The Basel III leverage ratio is reported based on quarter-end figures in some jurisdictions, but is calculated based on daily averages during the quarter in others. It’s an example of what the Bank for International Settlements calls “Window-dressing” in its annual report, referring to the practice of adjusting balance sheets around regular reporting dates, such as year- or quarter-ends. Window-dressing can reflect attempts to optimize a firm’s profit and loss for taxation purposes. For banks, however, it may also reflect responses to regulatory requirements, especially if combined with end-period reporting.

Banks reporting based on quarter-end figures are incentivized to compress exposures around regulatory reporting dates – particularly at year-ends, when incentives are reinforced by other factors (eg taxation). Banks can most easily unwind positions around key reporting dates if markets are both short-term and liquid. Repo markets generally meet these criteria. As a form of collateralized borrowing, repos allow banks to obtain short-term funding against some of their assets – a balance sheet-expanding operation. The cash received can then be lent on via reverse repos, and the corresponding collateral may be used for further borrowing.

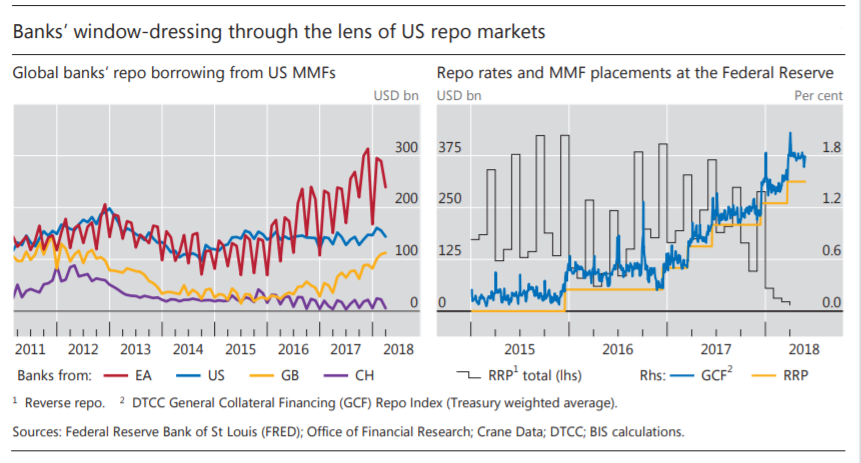

At quarter-ends, banks can reverse the increase in their balance sheet by closing part of their reverse repo contracts and using the cash thus obtained to repay repos. This compression raises their reported leverage ratio. The data indicate that window-dressing in repo markets is material. Data from US money market mutual funds (MMMFs) point to pronounced cyclical patterns in banks’ US dollar repo borrowing, especially for jurisdictions with leverage ratio reporting based on quarter-end figures. Since early 2015, with the beginning of Basel III leverage ratio disclosure, the amplitude of swings in euro area banks’ repo volumes has been rising – with total contractions by major banks up from about $35 billion to more than $145 billion at year-ends.

While similar patterns are apparent for Swiss banks (which rely on quarter-end figures), they are less pronounced for UK and US banks (which use averages). Banks’ temporary withdrawal from repo markets is also apparent from MMMFs’ increased quarter-end presence in the Federal Reserve’s reverse repo (RRP) operations, which allows them to place excess cash (right-hand panel, black line). Despite the implicit floor provided by the rates on the RRP (yellow line), there are signs of volatility spikes in key repo rates around quarter-ends (blue line). Such spikes may complicate monetary policy implementation and affect repo market functioning in ways that can generate spillovers to other major funding markets, especially if stress events coincide with regulatory reporting dates.