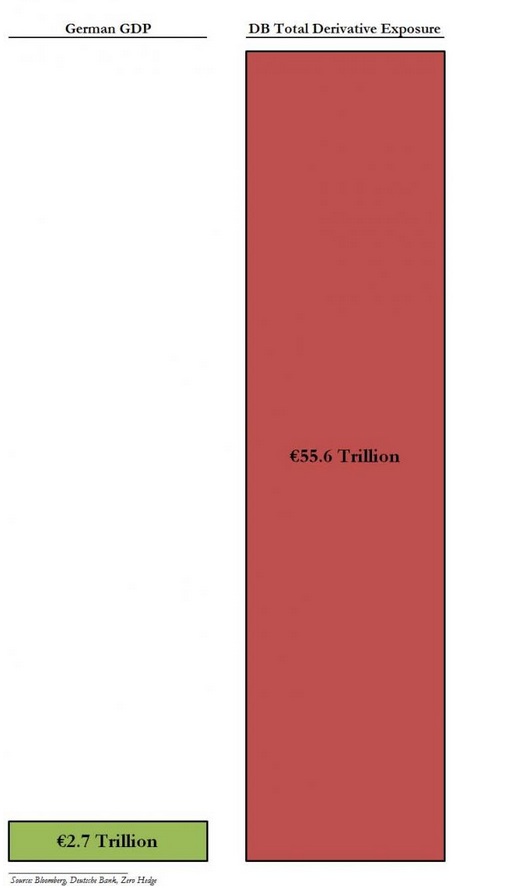

Back on March 20th we wrote a post about the problem of using gross notional when sizing the derivatives market. We said it made for great eye candy, but not much else. Well, it happened again when another zerohedge post “At $72.8 Trillion, Presenting The Bank With The Biggest Derivative Exposure In The World (Hint: Not JPMorgan)” came out on April 29, 2013. This time the eye candy was a graphic comparing Deutsche Bank’s total derivative exposure (€55.6 trillion) to the German GDP (€2.7 trillion).

Zerohedge did acknowledge the netted numbers, “…The good news for Deutsche Bank’s accountants and shareholders, and for Germany’s spinmasters, is that through the magic of netting, this number collapses into €776.7 billion in positive market value exposure (assets), and €756.4 billion in negative market value exposure (liabilities), both of which are the single largest asset and liability line item in the firm’s €2 trillion balance sheet mind you, and subsequently collapses even further into a “tidy little package” number of just €20.3…” We sense some sarcasm in there.

Sure, when it hits the fan, unwinding big complex derivatives portfolios can take years (although god-knows-how-many thousands of Lehman’s centrally cleared derivatives were unwound quickly and without loss) and exposure numbers can be vastly different in stressed markets versus orderly ones. But we are still not talking about gross notional as a reasonable basis for benchmarking exposure. Derivatives trades start out, by and large, with a Present Value of zero — meaning there is no exposure. As markets change, PVs change and exposure is created one way or another. Much of that exposure is collateralized — even more so with central clearing.

The proper way to think about this can be found at “How Big is OTC Really?” by Jon Skinner on the OTCSpace website. Our thanks to Bill Hodgson from www.OTCSpace.com for pointing us to this post on his website (gotta’ love LinkedIn). We like both Skinner’s and Hodgson’s writings on this topic as well as other derivatives related stuff. Skinner’s March 22, 2013 post takes us from the BIS reported $639 trillion open notional in derivatives to $1.1 trillion on net credit exposure. It is worth a read.

A link to the Finadium March 20, 2013 post is here.

A link to the April 29, 2013 zerohedge post is here.

A link to the “How Big is OC Really?” post is here.