Early this month the BIS released “Statistical Release, OTC derivatives statistics at end-December 2014” (April 2015). We take a look at some of the numbers.

The highlights from the report were:

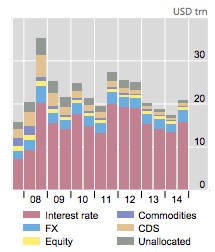

- “…OTC derivatives markets contracted in the second half of 2014. The notional amount of outstanding contracts fell by 9% between end-June 2014 and end-December 2014, from $692 trillion to $630 trillion. Exchange rate movements exaggerated the contraction of positions denominated in currencies other than the US dollar. Yet, even after adjusting for exchange rate movements, notional amounts were still down by about 3%…”

- “…The gross market value of outstanding derivatives contracts – which provide a more meaningful measure of amounts at risk than notional amounts – rose sharply in the second half of 2014. Market values increased from $17 trillion to $21 trillion between end-June 2014 and end-December 2014, to their highest level since 2012. The increase was likely driven by pronounced moves in long-term interest rates and exchange rates during the period…”

- “…Central clearing, a key element in global regulators’ agenda for reforming OTC derivatives markets to reduce systemic risks, made further inroads. In credit default swap markets, the share of outstanding contracts cleared through central counterparties rose from 27% to 29% in the second half of 2014. In interest rate derivatives markets too, central clearing is becoming increasingly important…”

We think that notional amounts are not terribly instructional (and have said so before). Notional numbers make good sound bites. A quick search of “$600 trillion” and “derivatives” came up with these dittys:

“…Derivatives: The $600 Trillion Time Bomb That’s Set to Explode…”

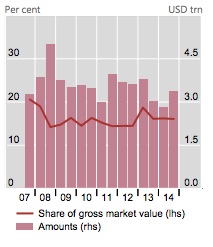

Gross market value, defined as “the cost to replace all outstanding contracts at current prices” is a better metric. It is interesting that it rose by 23% in the second half of 2014 to $21 trillion. The figures in this graph (and the next one) are in US$. Non-US$ trades were converted at the appropriate FX rate at the end of the observation period.

Gross Market Value (US$)

Source: http://www.bis.org/publ/otc_hy1504.pdf

Gross credit exposure is an better still. It takes Gross Market Value and subtracts the impact of netting (when there are legally enforceable agreements in place). The most recently figure reported was $3.4 trillion, up from $2.8 trillion at the end of June 2014. But Gross Market Value does not account for the value of collateral collected against that exposure. That is a number we’d like reported in detail by the BIS. How much collateral is cash? HQLA? Corporates?

Gross Credit Exposure (US$)

Source: http://www.bis.org/publ/otc_hy1504.pdf

One interesting statistic is a look at bilateral OTC interest rate derivatives trades between dealers. The numbers have fallen steadily over time. $70 trillion at the year-end 2014 versus $189 trillion at June 2008. This compares to trades with other financial institutions, including CCPs, of $421 trillion at year-end 2014 (equal to 83% of all outstanding contracts). However, one should keep in mind double counting. From the report:

“…The shift towards central clearing exaggerates the growth in notional amounts for other financial institutions because, when contracts are cleared through CCPs, one trade becomes two outstanding contracts…”

There is a wealth of data in the report, including numbers on credit default swaps, equity-linked, commodity, and foreign exchange derivatives. We recommend readers take a look.