Recently, TheStreet.com published its top ten list of Robo Advisors and some of the statistics quoted were pretty interesting (see Exhibit 1). Robo Advisor services are heavily targeted towards the retirement investor, marketing the exciting opportunity and power of algorithmic trading to the realm of retirement savings. There are direct impacts to watch out for in securities finance however, and the bigger Robo Advisors get, the more this matters.

“Robo Advisors” is a bit of a catch-all term, broadly representing algorithmically driven tools designed to manage investment portfolios with limited human intervention. Some of them are highly automated and almost entirely hands-off; others are push-of-the-button tools. The graphic below shows the odd melding of man and machine from the New York Times. All of these products focus on portfolio reallocation, and all are driven by proprietary algorithms based on… whatever they are based on. We don’t really know, since they are proprietary. Younger investors seem particularly interested in these services, with their presumably higher trust and immersion in technology, though a surprising number of investors nearing retirement age are also taking part. Many firms are actively touting the tools, implying better returns and punching up the technical sophistication and “advantage” they offer.

Exhibit 1

| Top Ten Robo Advisors by Assets Under Management through October 2014 | In Billions |

| Vanguard | 4.2 |

| Betterment | 2.5 |

| Wealthfront | 1.7 |

| Personal Capital | 1 |

| Asset Builder | 0.6 |

| Future Advisor | 0.2 |

| Rebalance IRA | 0.18 |

| Liftoff | 0.15 |

| SigFig | 0.06 |

| Others | 0.05 |

Source: TheStreet.com

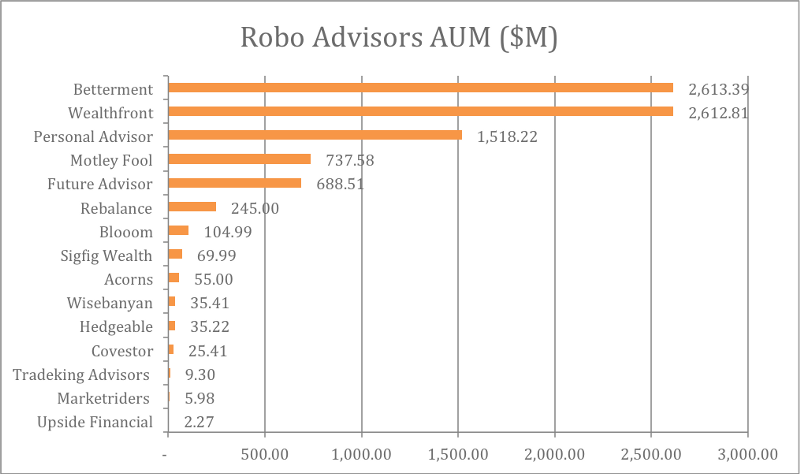

The view from Form ADV filings from October 2015, collected by Vimarsh Karbhari and Chandra Inguva and published on Medium.com, shows just a view of AUM from dedicated Robo Advisor firms (see Exhibit 2).

Exhibit 2

We can make some basic assumptions (which would need to be tested against real data that does not appear to be readily available as yet) about the behaviors and decisions of Robo Advisors.

- Individual investor portfolios under their control will be more actively rebalanced and reallocated – “traded” – than those managed by humans.

- Many of the algorithms consuming the same data points will make similar decisions about the “trades” they want to make.

- Some ETFs and mutual funds that incur presumed higher volatility (and therefore costs) will react in some way to protect themselves against these costs and/or the loss of stability.

We have already seen that market volatility can have impacts on the quality of ETF valuations (“Should we be worried about equity ETFs as the next big potential crisis?” January 4, 2016). But the flipside is also true: volatility in ETF investment driven by rapid, automated portfolio reallocations have a similar effect. This means that a nice stable supply of ETF equity suddenly dry up in the market, creating a collateral squeeze. We worked through these arguments in our February 2016 research report, “ETF Risk in the New Regulatory Environment.”

Similarly, could certain funds that are being actively traded pull back larger portions – if not all – of their securities lending portfolio to maintain a higher degree of ready liquidity? Could others now incurring higher costs due to the greater volatility start demanding better returns on the financed positions?

Algo trading was once part of the margin trading, professional investor marketplace. Now, we are seeing something conceptually similar emerging in the staid world the good old fashioned stabilizer of markets – the cash paying, long term buy-and hold retirement investor. This class of investor, and those managing and holding his investments, have been the backbone of reliable collateral supply in securities finance, largely financing the activities of the active trader.

Our prediction is that the growth of Robo Advisors engaging in algorithmic trading could have an impact on the overall stability of securities lending supply in ETFs and mutual funds. From taking assets out of the hands of big managers to frequent rebalancing, and many accounts trading on the same signals, this is an area to watch.