This conversation keeps coming back around and we’re not yet satisfied with the conclusions that we are hearing. Most recently, Fed Governor Jeremy Stein brought it up again. The tricky issue is that, in the category of unintended consequences, the Leverage Ratio (and the Supplemental Leverage Ratio) may do more to stifle securities lending and repo than anyone initially intended. But its not supposed to work like that.

Although much of his talk is about fire-sales, Stein points out some important facts around capital ratios and securities financing transactions (SFTs):

1) Current risk-based capital requirements are of little relevance for many types of SFTs.

2) Low risk-based charges on repo (and other SFTs) are appropriate – these are low risk transactions.

3) The LCR hits low high quality liquid assets transactions under 30 days including repo.

4) (Here’s the kicker:) If a broker-dealer firm faces a binding leverage ratio, this constraint can act as a significant tax on two types of SFTs that are largely untouched either by risk-based capital requirements or by liquidity regulations.

The way this happens is that large transactional volumes inflate the denominator of the Leverage Ratio (the Exposure Method – written up here by the Basel Committee). Generally speaking, this isn’t supposed to happen – the LCR or other risk-based capital measures are supposed to be the gating factor. But SFTs appear caught in a trap not of their own making. We are now in a situation that Stein says was undesired, “a regime of completely un-risk-weighted capital requirements, where the effective capital charge for holding short-term Treasury securities would be the same as that for holding, say, risky corporate debt securities or loans.” That’s unwanted but possible to improve.

We also don’t like Stein’s conclusion of the current scenario, which we agree with, that the Leverage Ratio constraint would push repo out of big banks and towards smaller banks with more Leverage Ratio room to engage in repo trades. We generally support a more level playing field between banks, but an artificial movement due to an unintended consequence in the Leverage Ratio doesn’t seem right to us.

Stein does propose three solutions to removing the Leverage Ratio as a binding constraint on SFTs. Two of these we will discard for long-winded reasons, but the third one, increased margin on repo, seems pretty reasonable. Stein proposes taking the Financial Stability Board’s ideas on increased margin, which were limited to certain types of transactions, and applying them at the security level. He calls this a Universal Margin Requirement. By somehow taking SFTs out of the denominator of the Leverage Ratio, this sounds like a reasonable compromise. Now it just has to get done.

A link to Jeremy Stein’s speech is here.

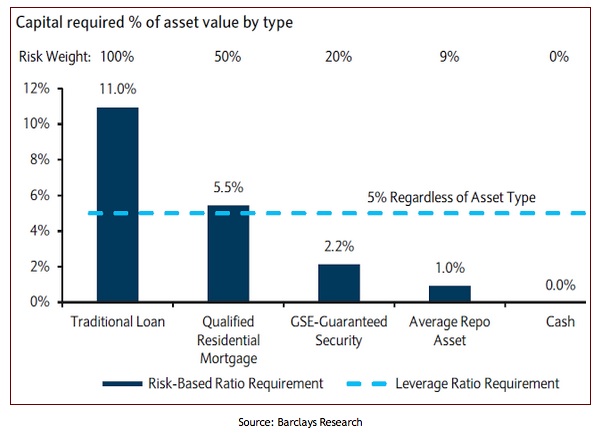

We covered a related version of this conversation last August when the blog SoberLook picked up a Barclays Research piece on Leverage Ratios and where banks might be inclined to put their capital in order to make returns relative to risk exposure. We’ve since referred to this chart on several occasions as it tells the story succinctly. In a nuthshell: the lower ROE with a hurdle of a 5% Leverage Ratio, the less interested banks will theoretically be to put their capital to work in products even if they have low capital weights. Here’s the chart: