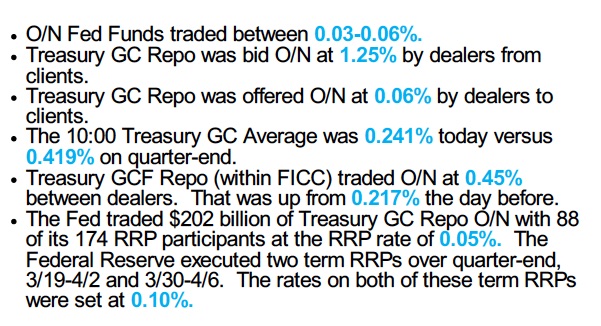

Quarter-end repo trading is always difficult, but this last quarter-end was especially hard. From Jeff Kidwell’s April 6th AVM Repo Commentary, here is what it looked like.

(Used with permission.)

But this post isn’t a rehash of quarter-end. Rather it is about what we can learn from the behavior of the repo market and apply it to how the market might behave when the Fed raises rates.

Why is there such a big spread between where dealers bid GC (1.25%) and where it was offered to clients (0.06%)? We needn’t look further than the scarcity of balance sheet and need to make bigger returns on capital. Of course the Fed taking cash out of the market with RRPs exacerbates the situation too.

The pressures brought to bear on the securities financing business rains down from regulators’ efforts to better capitalize the banking system. With more loss absorbing capital, systemic risk and inter-connectedness can be held in check. But by disconnecting the banks in the system, have the regulators also damaged the ability to transmit monetary policy?

When the Fed finally raises rates, they are going to hike IOER and RRP rates. In theory these higher levels will ripple through the system and increase the rates bank pay their clients (think savings rates) to say nothing of what they charge for loans. But with the need to increase returns on capital, we wonder if cash rich clients will be seeing much benefit? Will there be banks that can afford to increase their balance sheet by stepping in and arbitraging the flows? Lending rates will react, but will borrowing rates budge?

The traditional dynamic of system tightening relied on banks being in a reserve deficit position. They ended up paying more for Fed Funds as the Fed removed available reserves (remember the Fed doing matches sales?). These days the massive excess reserve position in the banking system all but makes Fed Funds an anemic tool to use for monetary policy. IOER and RRP will have to do the heavy lifting. The Fed has said they don’t want to rely on RRP too much. One argument is that in a stressed environment, allowing cash to flow to the RRP will starve the banks for cash and make a bad situation worse. Will raising IOER be able to shoulder to burden of tightening rates?

We wonder if the transmission of tightening doesn’t go as planned, what is next? The Fed can ratchet rates even higher, hoping wider spreads will entice banks to get involved. The other solution is to start selling some of the QE assets, sucking liquidity out of the system. This seems like a classic unintended consequence of the regulator’s work to face down systemic risk. But for monetary policy to work, will the system need to be better connected?