Recurring debt ceiling standoffs cause political disruptions and economic costs. Researchers at the International Monetary Fund (IMF) quantify one type of cost which is receiving growing attention: the spillover to short-term funding markets.

Using high-frequency aggregate as well as granular money market fund specific data, researchers find that flows in and out of the Treasury General Account triggered by the debt ceiling mechanism can create large swings in the repo spread and distort the supply of repo funding for the Treasury market.

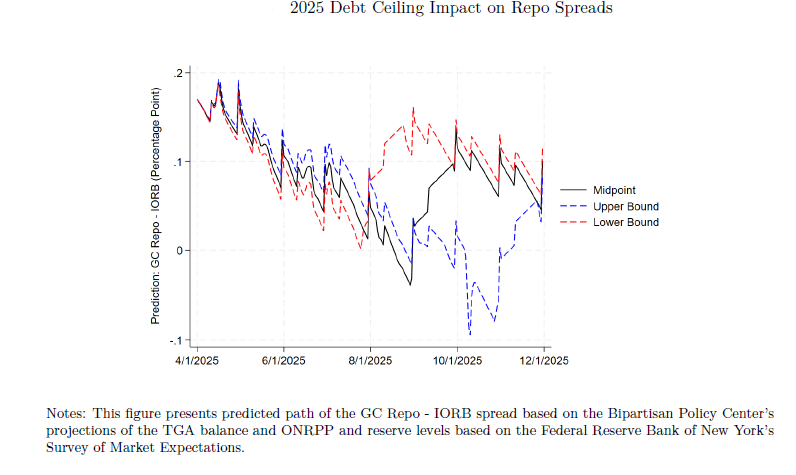

Applying estimates to the expected debt ceiling lift-off in summer 2025 implies that the repo spread could fluctuate by 20-30 basis points around the lift-off date. A higher level of aggregate bank reserves and overnight reverse repo balance at the Fed can dampen the impact on funding spreads appreciably.