ISDA has just published their 2014 Margin Survey. There is plenty to look at and discuss. In this post, we focus on the use of cash as collateral and who is doing collateral optimization.

The ISDA Margin Survey always includes some interesting analysis on collateral use and practices. There is a nice balance between cleared and non-cleared derivatives. Not surprising, the survey is dominated by banks & broker/dealers. They account for 87% of the respondents and probably a lot more if volume weighted. Given the tilt toward banks & broker/dealers and the high volumes they trade when compared to most of their clients, the results are skewed toward their practices.

Cash and government securities comprise 90% of collateral used for non-cleared OTC derivatives trades– not a big change from prior years. Cash alone is just a hair under 75% of the total collateral received, 78% of collateral delivered. We would expect that cash would dominate the equation. Variation margin is heavily cash weighted and could easily overwhelm the numbers. But independent amounts (for our SFT oriented readers, think about it as like a haircut) are way up there too. 63.5% of IA received was in cash, 61.9% of IA delivered.

What does all this use of cash tell us? The opportunity cost of cash is so low that bothering to use securities doesn’t make much sense. Systems to track cash are the bread and butter of banking. Securities are a lot more complicated, involving analyzing rule sets to insure eligibility, making sure the securities haven’t been sold (and recalling them if they have), watching out for corporate actions like coupons, etc., etc. Until the cost to post cash heads upward (driven by increasing rates or some regulatory issue), posting securities (primarily for IA) will be a while coming. When analysts write about collateral shortages, they need to keep the predisposition for cash in mind.

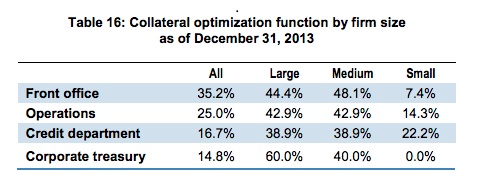

The survey asked about collateral optimization.

“…Collateral optimization appears to be best aligned as a front-office activity, particularly for large- and medium-sized firms. However, one-quarter of participants indicated their operations departments manages this process….One reason for the front-office focus could be that the optimization strategy is based on liquidity risk, funding costs, capital costs and other economic factors that are part of everyday life on the trading desk. Meanwhile, rules-based methods for optimization may fall within the sphere of the operations group…”

We agree with ISDA’s take on where optimization should happen – in the front office. However in our minds, front-office means the Repo trading desk. But its not really surprising that one-quarter of optimization is handled by Operations groups. In the past, settlements & substitutions drove a lot of this activity and the legacy lives on. What is harder to explain is why 17%% of optimization is done by Credit and 15% by Corporate Treasury. We imagine Corporate Treasury’s traditional job of keeper of the unsecured cash serves to reinforce the frequent use of cash as collateral (and visa-versa). Truth be told, Corporate Treasury groups don’t always get along with Repo Desks — something about strict rationing of unsecured cash and charging high spreads leaves a bad taste. But unless those groups work very closely with the derivatives front office (and by that we mean sit next to and talk most of the day) we are skeptical about the business model if cash becomes less common, securities more. As for Credit pulling the strings, setting limits and monitoring exposure is one thing, moving cash and securities around in a way that could easily have an impact on trade economics, that is another.