The Association for Financial Markets in Europe (AFME) published a report highlighting the critical barriers still limiting EU banking consolidation, including over €475 billion in capital and liquidity trapped by regulatory ringfencing, as well as the fact EU banks face higher funding costs versus global peers with stringent Minimum Requirement for Own Funds and Eligible Liabilities (MREL) requirements, at 28% of risk weighted assets, exceeding levels in the US (22%) creating a competitive disadvantage.

Due to the lack of cross-border waivers, over €225 billion of capital and €250 billion of liquidity are trapped in subsidiaries of EU banking groups. This regulatory ring-fencing discourages banks to engage in cross-border operations as it prevents transfer of resources between parent and subsidiary in times of stress. It also visibly limits the scale and competitiveness of banks operating in the EU.

Furthermore, the report finds EU Banking M&A is the slowest in the world with acquisitions taking 285 days on average – far longer than the US (219 days) delaying consolidation and weakening the sector’s efficiency.

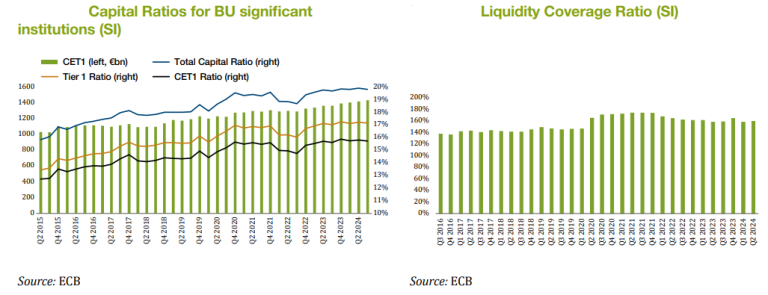

Bank-sovereign nexus: lower holdings while linkages continue to support liquidity management

Soon after the start of the great financial crisis, the first diagnosis of the link between national banking sectors and sovereigns began to emerge, where the sovereign credit quality deterioration eroded the asset quality of banking union (BU) banks as a significant portion of government debt was held by banks. Since 2020, BU bank’s exposure to their local sovereign has decreased from 8.44% of total BU banking assets to 6.86% in 2024, with some differences between member states with Portugal (18.7%) with the highest exposure and Ireland (1.3%) with the lowest portion.

While this trend suggests progress toward mitigating the sovereign-bank nexus, it does not fully capture the various linkages between the sovereign and banks. Banks and institutional investors rely on high-grade sovereign debt for collateral in central bank operations and market transactions, making minimal holdings of sovereign debt unrealistic. Half of the EU investment-grade fixed income assets (and thus eligible for central bank collateral) are issued by sovereigns, indicating the necessity for banks to hold a significant portion of these assets for liquidity operations.