Financial services both benefit from and fuel the DNA feedback loop. Offering financial services can complement and reinforce big techs’ commercial activities. The typical example is payment services, which facilitate secure transactions on e-commerce platforms, or make it possible to send money to other users on social media platforms. Payment transactions also generate data detailing the network of links between fund senders and recipients. These data can be used both to enhance existing (eg targeted advertising) and other financial services, such as credit scoring.

Data analytics, network externalities and interwoven activities (DNA) constitute the key features of big techs’ business models. These three elements reinforce each other. The “network externalities” of a big tech’s platform relate to the fact that a user’s benefit from participating on one side of a platform (eg as a seller on an e-commerce platform) increases with the number of users on the other side (eg buyers).

Network externalities beget more users and more value for users. They allow the big tech to generate more data, the key input into data analytics. The analysis of large troves of data enhances existing services and attracts further users. More users, in turn, provide the critical mass of customers to offer a wider range of activities, which yield even more data. Accordingly, network externalities are stronger on platforms that offer a broader range of services, and represent an essential element in big techs’ life cycle.

The source and type of data and the related DNA synergies vary across big tech platforms. Those with a dominant presence in e-commerce collect data from vendors, such as sales and profits, combining financial and consumer habit information. Big techs with a focus on social media have data on individuals and their preferences, as well as their network of connections. Big techs with search engines do not observe connections directly, but typically have a broad base of users and can infer their preferences from their online searches.

The type of synergies varies with the nature of the data collected. Data from e-commerce platforms can be a valuable input into credit scoring models, especially for SME and consumer loans. Big techs with a large user base in social media or internet search can use the information on users’ preferences to market, distribute and price third-party financial services (eg insurance).

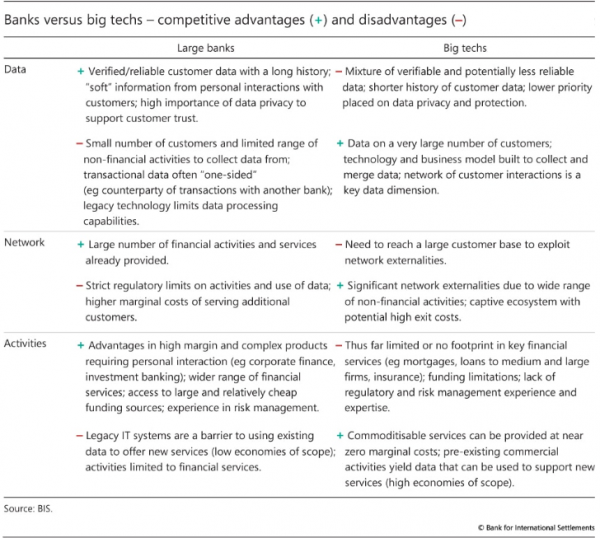

Although large banks have many customers and offer a wide range of services too (eg distribution of wealth management or insurance products, mortgages), so far they have not been as effective as big techs at harnessing the DNA feedback loop.

Payments aside, banks have not exploited activities with strong network externalities. One reason is the required separation of banking and commerce in most jurisdictions. As a result, banks have access mostly to account transaction data only. Moreover, legacy IT systems are not easily linked to various other services through, for instance, application programming interfaces (APIs).7 Combining their advanced technology with richer data and a stronger customer focus, big techs have been adept at developing and marketing new products and services. The main competitive advantages and disadvantages of large banks versus big techs are summarised in Table III.2.

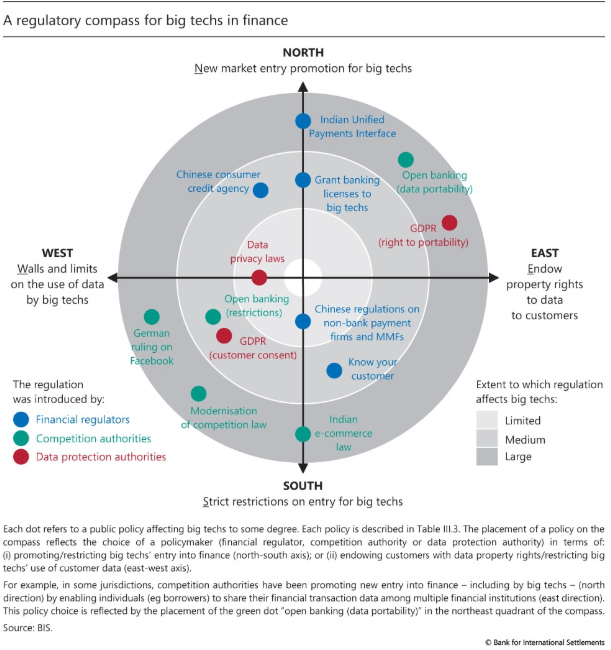

Big techs’ DNA can lower the barriers to provision of financial services by reducing information and transaction costs, and thereby enhance financial inclusion. However, these gains vary by financial service and could come with new risks and market failures. To navigate the new, uncharted waters, regulators need a compass that can orient the choice of potential policy tools. These tools can be organized along the two dimensions, or axes, of a “regulatory compass”.

The north-south axis of the compass spans the range of choices over how much new entry of big techs into finance is encouraged or permitted. North indicates encouragement of new entry, while south indicates strict restrictions on entry. The second dimension in the compass spans choices over how data are treated in the regulatory approach. It ranges from a decentralized approach that endows property rights over data to customers (east), to a restrictive approach that places walls and limits on big techs’ use of such data (west).