Recently Bank of New York Mellon (BNYM) published a review of a panel discussion “Securities Finance: Fixed Income & Repo Market Update”. We pick out a handful of interesting tidbits.

Under “Current Observations and Potential Impacts to Markets”, the panel noted 4 issues:

- Money market fund reform will have an impact on the short end of the market. It is likely that several hundred billion dollars will shift into government funds. A couple of large money fund complexes have announced plans to convert some of their prime funds to government funds. This will enable them to continue to operate with stable Net Asset Values (NAVs) and avoid gates and fees that are problematic for most investors.

- The short end of the yield curve remains relatively flat, without much of a pickup expected for six months or more. One-month to three-month investments are yielding from the low teens to the mid-20s. Fed funds have traded in a tight range – 12 to 13 basis points for the past six months. Treasury repos have been trading in the 7 to 9 basis points range, and agency mortgage repos are about 2 basis points higher.

- The Federal Reserve’s $300 billion reverse repo facility is supplying much needed treasury collateral to the market. The facility is open to about 160 participants; each has the ability to request up to $30 billion in collateral at the current rate of five basis points. Usage is low, running between $90 billion and $100 billion daily. Usage tends to spike at quarter ends, so the Federal Reserve added several hundred billion in additional collateral in December 2014 and March 2015.

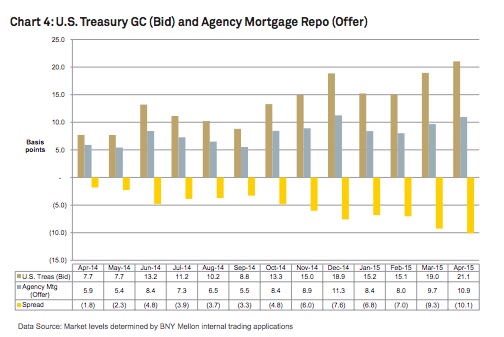

- The cost of raising cash in the repo markets has become expensive recently. This is further exacerbated at month end, days when Government Sponsored Enterprises’ cash is withdrawn from the market for P&I payments and when there is heavy coupon settlement.

The first three points highlight the amount of cash focused on the short end of the curve. Money market fund reform will create more demand for demand of HQLA. Investors required to keep cash investments short have compressed yields to pretty close to zero. And the Fed’s RRPs have provided a much needed source of collateral.

The last point – that raising cash in repo had gotten more expensive – seems to contradict the first three. Why are repo rates rising when it appears there is a lot of cash looking for a home? The answer seems to be in the disappearing balance sheet capacity of the broker/dealers and the friction that creates. On July 21st in a SFM post “New York Fed’s Liberty Street Economics: “Have Dealers’ Strategies in the GCF Repo© Market Changed?”” we looked at a Fed study on GCF activity by dealers associated with large Bank Holding Companies (BHCs), banks associated with small BHCs, and non-bank dealers. There was a fall off in activity at the start of 2013 for large BHC dealers that was not strategy related. Something else was going on – and we suspect it was a shift in the amount of balance sheet allocated to repo businesses. From the Fed blog:

“…Since we do not observe a change in the propensity of dealers to receive cash or to deliver cash over the sample period, it seems that the downward trend in net activity is due to reduced activity rather than a change in dealers’ strategies…”

Another explanation is that the Fed’s RRPs are crowding out the repo dealers, forcing them to pay higher rates to raise cash. In our opinion, this is less convincing.

There was a chart that also told an interesting story.

Could the widening spread between UST Repo bids and Agency repo offers be indicative that repo dealers need to get paid more to use their balance sheet? We wonder what this chart looks like simply comparing bid and offer for the same type of collateral?

Finally, BNYM noted:

“…There is a significant need for non-cash, balance sheet neutral trades. The non-cash balances in the U.S. government book (and overall) has grown more than 13% over the last 12 months due to “non-cash upgrade trades”. We anticipate that the non-cash component of BNY Mellon’s book will continue to grow…”

Are these the elusive collateral transformation trades to source HQLA for CCP initial margin starting to kick in?