Maintaining disparate front and back office systems connected to the collateral ecosystem is not just costly, it is also a source of lost profits. As firms speed up their collateral systems rationalization projects, the best outcomes will be supported by understanding how trading P&L will benefit from integrating cash and securities inventory with the full trading, risk and settlements environment.

The idea that collateral management systems in the front and back office should be an integral part of a technology stack is now considered industry standard: in an era where Straight-through Processing and data flexibility are the norm, systems interactions should be taken for granted. The ability to generate real revenue from systems that connect directly with each other, or better yet, one system that delivers full front to back functionality, has moved from wishful thinking to practical reality. This includes not only collateral management but also trading, risk and settlements.

Systems are not always well integrated in practice however, as generations of collateral trading and back office technology have been left installed at user firms. These legacy systems are appreciated for their lack of effort to rethink but were not built for the modern age of data interoperability. Every change in one part of the organization requires a workplan to re-engineer a data format or data model in the old platform. However, the preference to keep adding tape and band-aids to legacy systems rather than reimagine what the ecosystem could do is coming to a rapid close.

The post-COVID-19 era is requiring firms to optimize their processes and associated cost structures with a cross-organizational mandate. In the highly regulated capital markets industry, where pandemic-driven market volatility has led to large collateral swings, this includes mobilizing firm assets for collateral management in real-time across the organization.

As individual firms move towards systems rationalization, this has ripple effects for the entire collateral industry. Individual firms that can move data faster between front and back office have an easier time optimizing collateral across Treasury, repo, securities lending, OTC derivatives and centrally cleared products. Optimization at individual firms means that counterparties’ trades can be priced more effectively, driving down costs for all market participants. Individual corporate efforts also mean that firms that fail to rationalize systems see both higher costs and lower revenues from collateral-related activity. The drive towards efficiency from systems rationalization is a competitive differentiator.

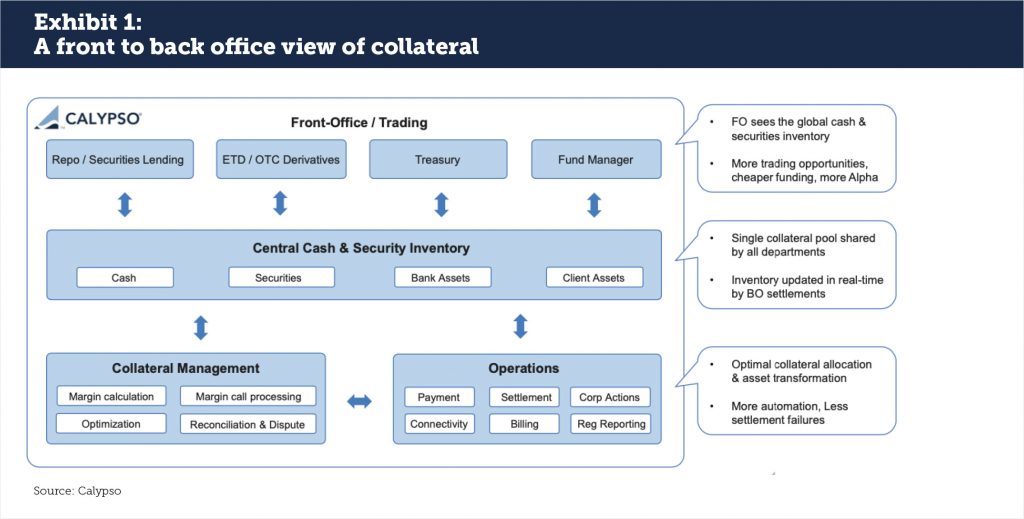

Collateral inventory integration across all cash and securities activities

Efficient collateral optimization brings a range of benefits to both the front and back office but achieving it in practice requires a front to back office view of inventory holdings. This includes not only what collateral is available but also what is coming in and going out in real time. This puts the front office in real-time communication with the back office, allowing both parties to communicate instructions on what collateral should be used for which purposes (see Exhibit 1). This simple data enrichment allows traders to know which securities are high value and should be used for purposes other than collateral deliveries, and to include collateral funding costs in their trading decisions. Likewise, operations users can know what securities are available to deliver for margin calls. Too often however, the legacy model of front to back technology means that this information is never delivered, or could be a day or two late in the process, leading to increased costs and lost opportunities.

As a practical example of increased costs, the collateral management process is part of calculating the standardised approach to measuring counterparty credit risk exposures (SA-CCR). When collateral is posted correctly and in a timely fashion, Exposure at Default (EAD) calculations can be reduced and an appropriate Margin Period of Risk (MPOR) can be assessed based on transparent liquidity metrics. The real-time impact of collateral holdings and settlement failures is reflected in these computations, and can also prevent trading with troubled counterparties in the event of a crisis. These same factors impact the calculation of derivatives XVA, leading to immediate P&L charges.

Systems rationalizations projects have an opportunity to directly include descriptive data, or metadata, as part of the collateral process. In a settlement-aware model, the back office receives the same information about available collateral including not just the position but also the metadata describing the position. When the front office and back office are looking at the same information at the same time, that allows all parties to agree on what inventory is really available and what has other, more valuable purposes for the organization. This is a big change from legacy systems that may never be able to communicate this content, much less in real-time.

Modeling the Trading P&L

Front to back systems rationalization that includes the collateral management process solves three problems at once. First, traders have access to their full range of tradable inventory. Second, sub-optimal trades and allocations disappear as settlements becomes an integral part of the trading activity. And third, the cost of integrating multiple systems for regulatory reporting disappears as one system manages the entire workflow, leading to more efficient reporting, lower regulatory maintenance and reduced exposure to supervisory fines. These benefits make a meaningful difference in implementation that can be demonstrated in a revenue statement.

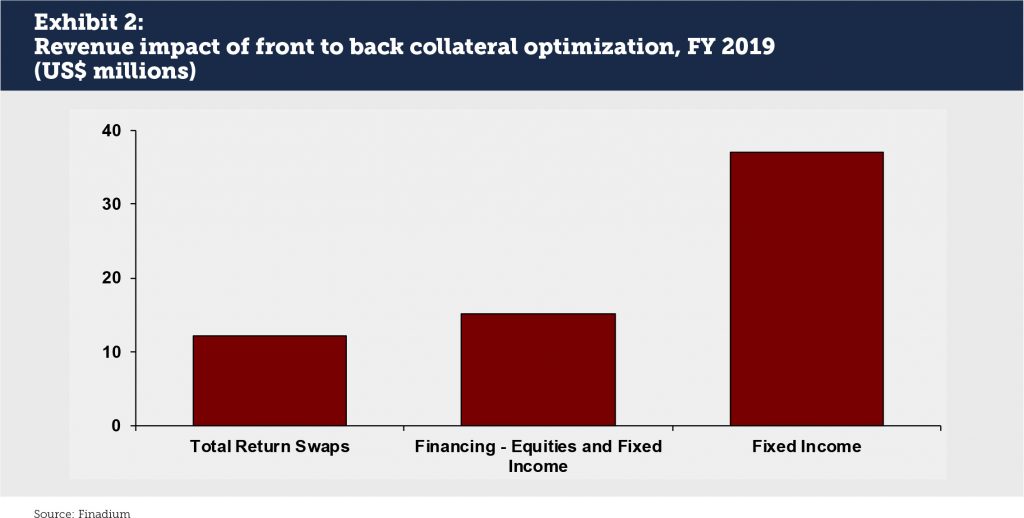

A conservative estimate is that collateral optimization can improve firm revenues by 6 basis points (see Exhibit 2). We can apply this figure to a range of collateral-related revenue activities to gauge the impact:

- Across 14 bank equity prime brokerage franchises that earned a collective $20.3 billion in FY 2019, an additional 6 basis points would have generated an incremental $12.2 million in revenue.

- For financing activities in both fixed income and equities in FY 2019, collateral optimization would have added $9.1 million on $15.2 billion in revenue.

- For nine large bank Fixed Income desks that generated a collective $61.9 billion in revenues in FY 2019 alone, effective collateral optimization would have added $37.1 million to the bottom line.[1]

These calculations look at the positive P&L, but there is also the negative P&L. Firms avoid additional costs for systems maintenance and integration and potential fines for under or over reporting of positions. This is the unknown risk of the cost of taking no action in systems rationalization.

External drivers for rationalization

While the immediate cost and revenue opportunity of systems rationalization may be the biggest reason to move forward with a project, a range of industry developments suggest other factors as well. We have compiled this short list based on our client work:

- Vendor risk from updating. The recent experience with LIBOR changeovers shows that out of date systems may not always successfully communicate new data elements with newer platforms, or may be unsupported for newly emerging products. Firms that have seen this happen in practice know the dangers and manual workarounds that may arise. Reducing the number of systems reduces the need to transfer data and reduces the number of times a firm must reconcile the data. One well-supported system that speaks to the front and back office at the same time solves this problem.

- Low interest rates. A low rate environment means challenges for financial institutions to earn net interest or other revenues linked to spreads that may be wider in higher interest rate environments. Clients will never be interested in paying more to make up a firm’s revenue loss due to low rates. As a result, firms know that they must be more efficient in their technology use to reduce costs and create new revenue opportunities, especially in the monetization of idle or poorly utilized assets.

- IM documentation. The next generation of ISDA Initial Margin documentation is expected to move large sums of cash into securities. The most recent ISDA Margin Survey from year-end 2019 showed $32.6 billion held as cash by major banks in Independent Amounts (IA) for non-cleared derivatives, on top of the $173.2 billion held in securities for counterparties both in-scope and out of scope of UMR rules.[2] If this IA cash all moves to securities, that is an additional 19% of OTC derivatives margin that must be delivered and segregated. The cost of holding securities collateral that can utilized elsewhere can mean lower costs for clients, but only firms that have that information readily available will price their services competitively.

- Repo electronification. A greater focus on electronic trading in repo, along with the need for data to feed into trading systems and internal Treasury and Risk departments, means that more intelligence on repo positions and collateral usage translates into a more efficient enterprise. More electronification also means more demand for automated collateral movements and Straight-through Processing that impacts multiple parts of the organization.

- COVID-19 lessons. The experience of COVID-19 has shown that employees can successfully work from home so long as they have the right technology platforms supporting their efforts. COVID-19 led to a sudden increase in margin calls owing to market volatility, not to mention settlement failures in the delivery of collateral. In some cases this led to funds having to liquidate their positions. Firms that minimize the steps and potential breakages between front and back office systems can permanently ease the communication burden between trading and settlements wherever employees happen to be working that day, helping to avoid trading problems. As firms consider projects that had previously been set aside for lack of time, collateral management is taking priority.

- Fines for under or over reporting. Multiple systems contribute to the possibility of reporting errors; one front to back office platform means more accuracy in regulatory reporting. We saw in 2020 that over or under reporting in MiFID II resulted in fines from supervisors: ESMA said that fines totaled €88 million in 2019, up from €10 million in 2018.[3] The UK Financial Conduct Authority has a history of fining banks for a failure to submit complete and accurate transaction reports, and market expectations are that fines related to Securities Financing Transactions Regulation (SFTR) could be forthcoming.[4] This is an issue that is not going away.

The new collateral optimization

The definition of collateral optimization has changed in recent years from being a smart ordering of lists for cheapest to deliver to a firm-wide view of collateral as an asset, for true balance sheet optimization. Technology has not always kept up however, leading some firms to exceed expectations of data flexibility and operational efficiency while others lag behind, tied in large part to legacy systems.

The ability to capture the promise of collateral optimization starts with technology. Stand-alone systems that were installed a decade or two ago are often all but inoperable with current demands. These platforms were once integral to the core workings of trading but are now systems that plug in on the side to a firm-wide framework. The ability to move past legacy systems and create a robust front to back office, single point of transparency in collateral across the organization helps the new meaning of collateral optimization deliver on its promise. This front to back systems rationalization, with transparent collateral data as part of a technology stack that can communicate across trading, risk and settlements, lies at the heart of the new collateral optimization framework.

About the Author

Alan Sheehan is the Director of Product Management for Calypso’s Collateral Management and Securities Finance solution. Since 2006, he has been responsible for building Calypso’s Collateral Management and Securities Finance solutions from their inception.

Alan Sheehan is the Director of Product Management for Calypso’s Collateral Management and Securities Finance solution. Since 2006, he has been responsible for building Calypso’s Collateral Management and Securities Finance solutions from their inception.

Prior to joining Calypso, Alan worked for Dresdner Bank in a number of senior operational roles including Global Head of Corporate Actions. His last role at Dresdner Bank was project managing the implementation of Calypso for Securities Financing.

[1] Revenue data based on “Total Return Swaps and Bank Resource Optimization,” Finadium, October 2020

[2] “ISDA Margin Survey Year-End 2019,” ISDA, April 14, 2020, available at https://www.isda.org/2020/04/14/isda-margin-survey-year-end-2019/

[3] “ESMA sees significant increase in EU market abuse sanctions in €88 million in 2019,” ESMA, December 21, 2020, available at https://www.esma.europa.eu/press-news/esma-news/esma-sees-significant-increase-in-eu-market-abuse-sanctions-€88-million-in-2019

[4] Transaction reporting fines, Financial Conduct Authority, available at https://www.fca.org.uk/markets/transaction-reporting/transaction-reporting-fines