What we learned at our Clearing and Market Infrastructure for Repo, Funding and Liquidity event (Premium Content)

Will the OFR and NY Fed Repo tracking project capture financing outside of traditional repo products? Not likely.

BCBS, IOSCO and IAIS release joint report on risk management. They address collateral shortages and illiquid margin.

The Fed releases proposed rules on using Muni bonds for LCR requirements. But the devil is in the details.

Tri-Party Repo: Liberty Street Economics blog looks at the history and BNYM announces the end of secured credit exposure (aka “unwind”/”rewind”)

The Systemic Risk Council publishes an interactive tool for looking at bank stats. We especially like “Short Term Noncore Funding as a Percent of Total Assets”.

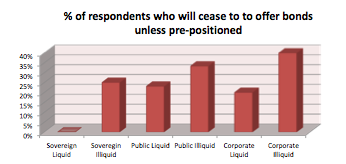

The Oliver Wyman/Morgan Stanley survey of wholesale markets: something new or just the same old stuff?

The Fed publishes “Overnight RRP Operations as a Monetary Policy Tool: Some Design Considerations”, a look at the RRP program objectives and risks, Part II

Highlights from comment letters: the FSB’s proposal on Trade Repositories in securities finance (Premium Content)

The Fed publishes “Overnight RRP Operations as a Monetary Policy Tool: Some Design Considerations”, a look at the RRP program objectives and risks, Part I

Should declining liquidity in the US Treasury markets push haircuts on UST repo up? We think there is a good case.

Highlights from comment letters on the “Regulatory Framework for Haircuts on Non-Centrally Cleared Securities Financing Transactions”