So what are CCPs charging to hold collateral? For ICE Clear U.S., the answer on cash is 6bp plus a cut to ICE and 5bp on US Treasury balances.

Late last year ICE announced (Note 13-115):

“…to comply with new CFTC regulations and international regulatory standards regarding liquidity arrangements…ICUS will impose a charge of 5 basis points (bp) fee on clearing member US treasury securities balances (based on par value). This fee will be calculated daily, accrued monthly, and included on clearing member summary of fees as part of the monthly clearing member billing. This fee will replace the existing transaction-based charges for collateral activity…”

And

“…in early 2014, ICUS will begin to utilize external investment advisors to manage clearing member cash on deposit to meet original margin and guaranty fund requirements…ICUS will retain a portion of interest earned on cash balances with the remaining return going to clearing members after expenses. ICUS expects such cash management expenses to be 6 bps…”

On February 11, 2014, ICE announced a delay in the 5bp charge on US Treasury collateral. Notice 14-012 said that the fee won’t come into effect until March 1, 2014.

Our readers will recall that CCPs will need to have liquidity facilities in place covering the non-cash collateral they hold. Those facilities are, in effect, a cash put to the liquidity provider of the underlying collateral. For US Treasuries the cost of providing same day liquidity should not be big, but 5bp does seem pretty cheap to us. Market participants, and CCPs in particular, were predicting that clearing costs would go up to compensate for the cost of the liquidity program. We wrote about this on October 16, 2013 in “The CFTC and liquidity rules for DCOs: do they need committed repo facilities for their US Treasuries?” and again on November 19, 2013 in our post “CFTC rules on CCP liquidity facilities: Treasuries need to be covered”. In the October post we noted that the CME estimated the liquidity facility cost to be 30bp.

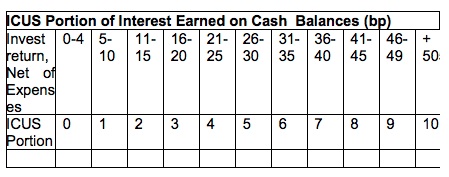

So the expenses to manage the cash are estimated to be 6bp. On top of that will be ICE’s cut. The chart below illustrates ICUS’ floating fee, based on the investment return, net of expenses. In the current interest rate environment, according to the ICUS Notice, those cash returns could easily go negative.

We also want to mention another SFM post, “Could US CCPs pay 25bps on cash collateral at today’s interest rates? The plot thickens” (December 9, 2013). In that article we wrote about new Fed rules on Financial Market Utilities (FMU) could allow their cash to be deposited at the Fed, earning (currently) 25bp. We quoted from the Fed press release “Federal Reserve Board announces final rule regarding Federal Reserve Bank accounts and services for financial market utilities designated as systemically important” released on December 5, 2013:

“proposed § 234.7(b) provides that interest paid by a Reserve Bank on balances maintained by a designated FMU in its Reserve Bank account shall be at the rate paid on balances maintained by depository institutions or another rate determined by the Board from time to time, not to exceed the general level of short-term interest rates.”

We also wrote:

“…And who are the Financial Market Utilities in question? The list of eight includes the CME, DTC, FICC, ICE Clear Credit, NSCC and the OCC…”

So if cash held as margin or guarantee funds could earn 25bp from the Fed, less 6bp in investment management expenses, less 4bp to ICE, that still beats overnight UST repo by a long shot. 6bp seems a lot to pay an investment manager to simply put the cash at the Fed, but whatever. Now we need to find out what others are charging.