A paper published by BNY Mellon and Rule Financial earlier this month caught our eye. It is called “To Clear or not to Clear….Collateral is the question”. We want to highlight a couple things that we thought were interesting and our take.

1.) The market is heading toward standardization.

“…Considerable product uniformity is required for clearing to be practical. As a consequence, the pace at which OTC derivatives are being migrated to the cleared market model depends to a substantial degree on how readily OTC derivatives can be standardised. Today, interest rate swaps and credit default swaps are already widely cleared; the International Swaps and Derivatives Association (“ISDA”) reports that 51% of the global interest rate swap market (which itself makes up over 80% of the gross notional volume of the total OTC derivatives market) is now cleared (although so far this is mainly dealer-to-dealer business). (Response to 1st ESMA Discussion Paper on Draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories’, AFME/BBA/ISDA, 20 March 2012, p.1.)..”

There are two areas of long term impact that come to mind: the first is that you can wave good-bye to any bespoke swap solutions. The capital cost to the broker/dealers will be prohibitive and, if they are even willing to do the trade, that cost will be passed through plus some. Anything complicated, often a layering of various types of swaps and options, will have to be decomposed in order to be executed. This will impact margin required as well as increase operational complexity. Second, the broker/dealers, when they do these compound deals, make a lot of money. The opaqueness of these complicated deals allow for realizing not only bid/ask spreads, but being paid for structuring complexity. This isn’t necessarily a bad thing since the deals address very specific needs in the market. But when the deals are simplified, revenue may suffer (along with risk management).

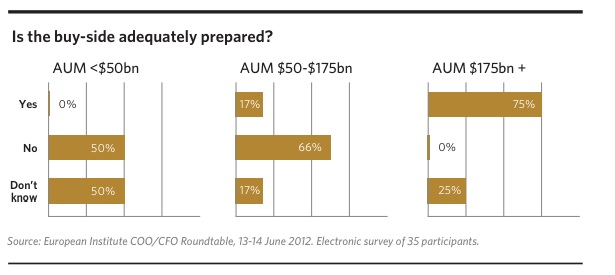

2.) The buy side isn’t ready, specifically medium and smaller managers. This is a re-occurring theme, but for good reason. It is the challenge of 2013.

“..The themes which emerged from the survey responses centred on uncertainty over the timetable for implementing regulatory changes and the challenges in preparing for the transition. While survey respondents recognised the potential material impact of new collateral requirements on investment and operational processes, only 20% of buy-side respondents had finalised their target processes. This means that projects have been, or will be, as the case may be, compressed into the latter half of 2012 in order to meet regulatory deadlines..”.

“…The operational and risk management challenges associated with the transition to the cleared market model are substantial; these include the preparation of legal documentation, establishment of market access and connectivity, on-boarding and account opening at clearing brokers, and the implementation and management of complex margining and collateral processes…”

This isn’t just about education anymore. It is about connectivity, modeling, legal agreements and relationships.

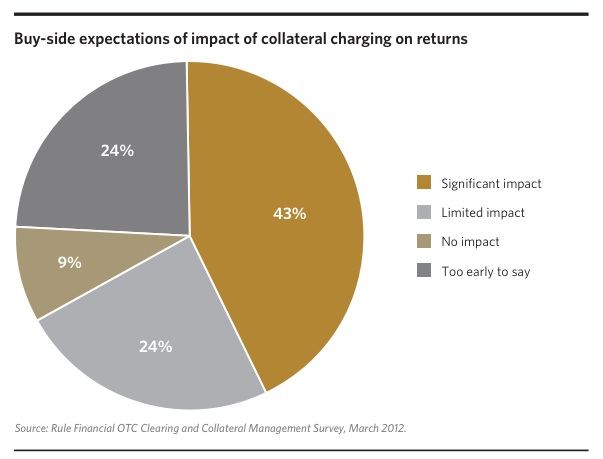

3.) Margin is going up, up, up and so will investment allocations on CCP eligible collateral. This will not necessarily be driven by management of portfolio risk (e.g. what the managers get paid to do) but on the need to have the paper to support the OTC derivatives trades.

“…The amount of initial margin that has to be sourced can be substantial. A typical initial margin obligation for a 5-year vanilla interest rate swap might be equivalent to 1-3% of the notional value of the contract. Long-dated or complex contracts, on the other hand, may require substantially more collateral because of the greater potential future exposure; perhaps 10% of notional for a 30-year and 15% of notional for 50-year tenors. Posting of initial margin can create acute problems for institutional investors since they generally establish directional positions. OTC derivative dealers are more likely to run matched books and therefore face much more modest initial margin commitments due to the benefits of netting…”

“…Research carried out by the Investment Management Association (“IMA”) identified as ‘not unusual’ the requirement for CCP-eligible collateral equivalent to 20% of the investment value of test portfolios in order to be able to meet initial and variation margin obligations on typical OTC derivatives strategies under mandatory clearing. (‘IMA response to European Commission public consultation on Derivatives and Market Infrastructures’, Investment Management Association, July 2010, p.14 and Annex A)…”

“…The impact of proposed EMIR requirements for collateralisation of OTC derivatives trades was calculated to result in an annualised yield drag of 2% for pension funds and 2.5% for insurance funds, due principally to the allocation of 10-20% of portfolio assets to cash or near-cash to meet potential variation margin calls. The compounded effect on portfolio assets over time is clearly very material…”

A lot of studies tell us about how collateral demands for margin will be on the rise. It’s the “great sucking sound” we all hear in the background. But “…the allocation of 20% of portfolio assets to cash or near-cash to meet potential variation margin calls…” is higher than most numbers bandied about. This is the true cost of the financial crisis.

4.) We thought the conclusion to the paper was worth reading twice.

“…The danger is that the perceived benefits of central clearing are overwhelmed by the unintended consequence of the costs of compliance being passed through to the policy holder and pension scheme member, for example, whether in the form of constrained, sub-optimal portfolio decisions or the direct costs of adapting to the new market structure…”

A link to the article is here.