The European Securities and Markets Authority (ESMA), the EU securities markets regulator, published its second Trends, Risks and Vulnerabilities (TRV) Report of 2020. The Report analyses the impact of COVID-19 on financial markets during the first half of 2020 and highlights the risk of a potential decoupling of financial market performance and underlying economic activity, which raises the question of the sustainability of the current market rebound.

The TRV also highlights specific risks for financial stability and investors in relation to Collateralised Loan Obligations (CLOs) model risk, EU fund industry interconnectedness and spill overs, research unbundling and closet index funds costs and performance.

Continued very high risks across ESMA’s remit

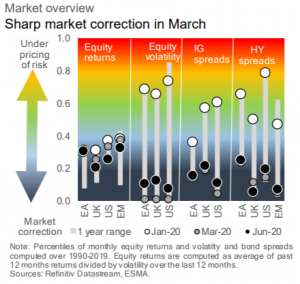

The COVID-19 pandemic, in combination with the valuation risks highlighted in ESMA’s previous risk assessments, led to massive equity market corrections in Q1 while in Q2 markets witnessed a remarkable rebound, helped by public policy interventions in the EU and elsewhere.

The market environment however remains fragile, and ESMA maintains its risk assessment. It sees a prolonged period of risk to institutional and retail investors of further – possibly significant – market corrections and very high risks across the whole of ESMA’s remit. The extent to which these risks will materialise will depend on two drivers: the economic impact of the pandemic, and additional external events in an already fragile global environment. The impact on EU corporates and their credit quality, and on credit institutions, are of particular concern, as are growing corporate and public indebtedness and the sustainability of the recent market rebound.

Decoupling between market performance and economic activity

The sustainability of the recent market rebound remains a concern. Equity markets have surged by 40% in the euro area since the trough reached in mid-March, almost back to pre-crisis levels, while the IMF expects GDP to drop by more than 10% in 2020, followed by a mild recovery of 6% in 2021.

Initial impact of COVID-19 on financial markets

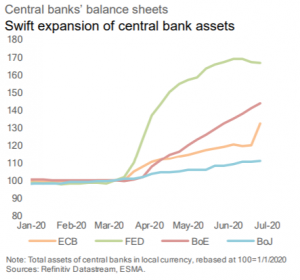

During the reporting period for this TRV, ESMA saw the financial market go through three stages, each described in detail in this report: i) a liquidity and volatility period (mid-February – end-March) where markets, investment funds and infrastructures faced high levels of stress, ii) a rebound period (early to end-April) where markets grew swiftly on the back of policy actions and iii) a differentiation stage (starting early May), where credit and solvency risk came to the fore, as investors started to differentiate between issuers and asset classes amid ongoing deterioration of economic fundamentals.

Against the background of these events, regulators have monitored closely any threats to financial stability and taken measures to promote stability, investor protection and market integrity.

This TRV also takes an in-depth look at specific risk issues in four articles:

Model risk in Collateralised Loan Obligations (CLOs): The benefits of securitization depend on its ability to effectively engineer and limit credit risk. Following up on ESMA’s recent thematic report of rating methodologies used for CLOs, this article explores the approaches to modeling CLO credit risk adopted by the three main Credit Rating Agencies.

Interconnectedness and spillovers in the EU fund industry: The COVID-19 turmoil has highlighted the risks of market-wide stress, not least for investment funds. This article assesses the connectedness among EU fixed-income funds. Our empirical results suggest high spillover effects, indicating that funds exposed to less liquid asset classes are more likely to be affected by shocks originating in other markets than funds invested in more liquid assets.

MiFID II Research Unbundling – first evidence: This article analyses the impact on EU sell-side research of the MiFID II Research Unbundling provisions that require portfolio managers to pay for the research they obtain. In the past, concerns have been raised, based primarily on survey data, that the new rules could have detrimental effects on the availability and quality of company research in the EU. In order to provide a more detailed, data-based contribution to inform this discussion, ESMA has analyzed a sample of 8 000 EU companies between 2006 and 2019, and does not find material evidence of harmful effects from the unbundling rules.

Costs and performance of closet index funds: ‘Closet indexing’ refers to the situation in which asset managers claim to manage their funds in an active manner while in fact tracking or staying close to a benchmark index. In this article ESMA looks at annual fund-level data for the period 2010-2018 and finds that investors see lower net performance of potential closet indexers than the net performance of genuinely active funds, as the marginally lower fees of potential closet indexers are outweighed by reduced performance.