The Q1 Fed’s Senior Credit Officer Opinion Survey (SCOOS) just came out. We take a look.

Looking at the standard questions is like watching “Groundhog Day” – the same thing over and over again. Everyone pretty much says the same thing in a remarkable version of groupthink. We are hoping that this uniformity does not mean complacency.

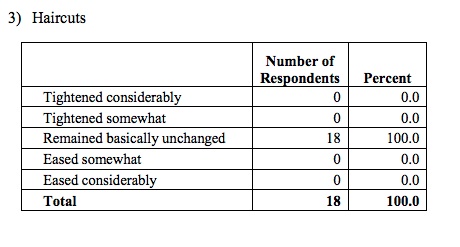

For example, when asked about changes in haircuts on high grade corporate bonds for their best clients the poll answer was:

However, there are some longer term charts that are worth paying attention to.

However, there are some longer term charts that are worth paying attention to.

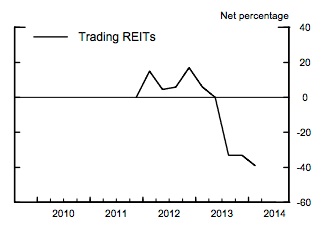

Looking at the number of respondents who reported greater use of leverage by Trading REITs, the numbers have been showing a clear downward trend.

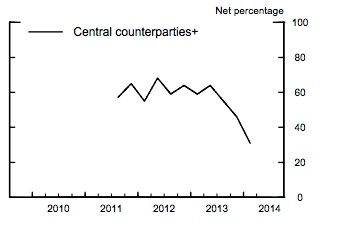

Or “Respondents increasing resources and attention to management of concentrated exposures to central counterparties” we see:

The interesting material are the special questions. This report focused on synthetic prime brokerage:

“…Over the past year, so-called synthetic prime brokerage arrangements have reportedly emerged as an increasingly important source of leverage for hedge funds. Under such arrangements, levered exposure is created through TRS and other OTC derivatives rather than through more traditional secured financings—for example, through margin lending or repurchase agreements…”

Questions were asked about the following hedge fund types:

- Equity long-short hedge funds (fundamentally oriented)

- Equity long-short hedge funds (quantitatively oriented)

- Event-driven equity funds

- Other equity funds

- Macro-oriented hedge funds

- Credit-oriented hedge funds

- Emerging market–oriented hedge funds

Where synthetic prime brokerage has not done well is with credit-oriented and emerging markets hedge funds. One advantage of synthetic prime brokerage is the ability to internalize trading (e.g. finding one client who is short to offset against another who is long) while using derivatives accounting. Those offsetting positions are less common in credit and EM markets. Without the offsetting trades, the PB has to hedge the risk in the cash & repo markets (for example, going long the physical security to generate the total return and financing the underlying). We touched upon this in our April 3rd post “Matching Collateral Supply and Financing Demands in Dealer Banks” in the NY Fed’s Economic Policy Review. They really don’t like repo netting.”

Below is a chart showing how many of the SCOOS survey participants answered either “widely employed by a large number” or “employed by some clients or in some situations” to the question: “How would you characterize the current use of synthetic financing making use of TRS and other OTC derivatives (as an alternative to traditional secured financings) by hedge fund clients of each of the following types”

When asked how many hedge fund clients had changed their use of synthetic PB over the past year, the results did show some shifts, albeit hardly tectonic. At least 50% of the respondents said that use among hedge funds had remained the same, with a range of 57% for Equity long-short hedge funds (quantitatively oriented) to 78.5% for Credit-oriented hedge funds (although credit-oriented funds aren’t big users in the first place). Ex credit and EM funds, just under 30% of the respondents said use had “increased somewhat”. There were very few “increased significantly” answers.

The final question was about how important certain factors were in motivating clients to use synthetic PB. One question stood out: “Access to foreign markets”, where 71% of respondents rated it “very important”. Using derivatives to gain exposure to foreign markets takes the local regulatory issues out of the hands of the hedge fund, which is probably most welcome.