It’s been a very active Q1 2020 at Finadium, both in our product development and the complex changes in market dynamics that the coronavirus and Brexit have introduced. Here’s a product update, along with a review of some predictions we’ve made in the last couple of years.

Borrowers of securities from US mutual funds and ETFs

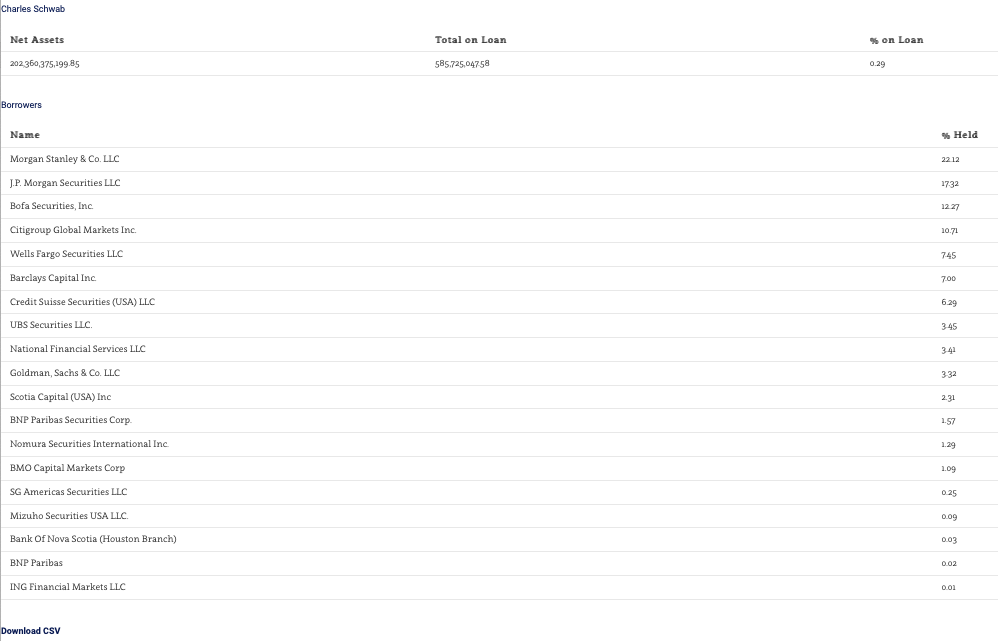

We’ve added a new data set to our US mutual funds and ETFs in securities lending analysis tool. The GUI now allows users to search fund complexes and their respective borrowers by total securities on loan and percentage held by each borrower. We’re also supporting a reverse lookup, which lets a user search a borrower and get a list of all funds they borrow from with amounts on loan. The data set is collected from Form N-PORT-P filings with the SEC – we are collecting and parsing every available filing. We’re presenting the most recently collected data by calendar year on our website (so far from 2019, 2020 coming soon). The data are available at https://finadium.com/sec-fund-data/ with your Finadium client login.

Here’s a snapshot of the data search for Charles Schwab’s latest filings. As with all Finadium data sets, the information can be downloaded with one click to a CSV file.

SOFR Averages and better repo search

On our US repo analytics GUI, we’ve added the Federal Reserve’s new SOFR Averages. Users can capture the index, 30 day, 60 day and 90 day moving averages in a time series that can be quickly exported to CSV. The new SOFR figures were launched by the Fed earlier this week. The data can be found at https://finadium.com/repo-analytics/ with your Finadium client login.

We’ve also added more flexible search features on the left sidebar. Given the volume of the data points, we’ve adjusted the search so that when a new data element is selected it appears on the left hand side, and can be unselected from there as well. We are using this feature to quickly compare several repo variables at once, for example daily SOFR, GCF and BNY Mellon Tri-party Index data side by side, and keep track of what we’ve selected.

We are working on two new updates for the repo analytics page: more precise reporting on primary dealer positions and financing, and better charting including a one click save of the image.

Amsterdam ESG event postponed

The COVID-19 coronavirus has negatively impacted our event planning. We’ve had to postpone our Building Out Capital Markets for ESG event in Amsterdam, originally scheduled for March 31. The decision was driven by both the need to protect the well-being of our guests and the fast spread of travel restrictions at our guest and sponsor institutions. We expect to reschedule this event for later in 2020, and have received a strong show of support from industry participants that they look forward to attending. We’ll have more news on this as soon as we have a new date.

For our big Finadium Investors in Securities Lending conference May 13-14 in New York, we have no plans to postpone as yet, but are watching developments closely and are speaking regularly with guests and sponsors. We’ll send out updates as we have them.

A few things we’ve gotten right lately

While our official crystal ball broke many years ago, we still find that careful analysis can reveal patterns in market and regulatory behavior. Some of our earlier forecasts have now come to fruition:

- In May 2018 we said that Frankfurt would be an important new hub for collateral and liquidity trading. We said that “While the timing of staffing moves is uncertain, it is probable that they will happen at some point in the next two to three years.” On February 27 2020, the FT reported that “Citigroup is further consolidating its European investment bank and trading leadership in Frankfurt as the post-Brexit financial services divergence between the UK and EU becomes clearer…. ‘It is a clear endorsement of Germany as a market and Frankfurt as centre for our post-Brexit EU operations,’ said David Livingstone, Citi’s Emea head. ‘As the EU faces decisions on the formation and structure of its capital markets, we are moving our leading people there to help their development for the next generation.'”

- In December 2019 we presented the important question of whether the Fed would simply take over the US repo markets, or whether banks might gain some relief in balance sheet treatment to provide liquidity. There is moral hazard and potential systemic risk all around, but we were pretty sure that the Fed had no easy outs. We said that “The opinion that Fed asset purchases should reduce the need for repo intervention seems optimistic in the short and medium term. With bank balance sheet at capacity, the number and frequency of technical events that can cause disruption in the face of prolonged US Treasury issuance appears greater than $60 billion/month. We expect that the need for Fed repo intervention will continue alongside this not-QE program for some time to come.” We’ve already seen the Fed continue its repo liquidity programs with hints that they will continue well through April, their previously-planned end date. Calls to make use of the discount window more common are another version of liquidity provision with potentially larger impacts. The Fed is in the liquidity provision game for the long haul.

- In August 2018 we explored the just-emerging technology of quantum computing (QC). At the time, we said “QC involves preparation not just for the computers but also what to do with them. This is not just a new computing platform but also a new way of doing business, once business figures out what to do with the new technology.” This is now starting to play out in practice. Two weeks ago, Oracle reported via Forbes that “Goldman Sachs is working with a California quantum computing startup on reducing the time it takes to value portfolios of options. Volkswagen last fall demonstrated using a quantum computer to instantly calculate routes for nine buses through Lisbon for the WebSummit conference. In Germany, chemical company BASF invested in a startup spun out of Harvard that’s developing software for quantum computers.” The big question next is what happens to cybersecurity in the age of quantum computing?

Thanks for all your continued support. We appreciate it greatly.