Fitch released a report on January 28, 2013 entitled “U.S. Money Fund Exposure and European Banks: Eurozone Declines, France Increases”. We dig behind the headlines and noticed some interesting trends.

There were a couple basic messages:

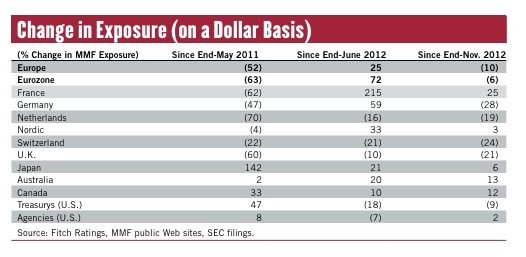

1.) MMF exposure to European banks fell slightly last month. However since June 2012 – the height of the Euro scare – allocations are up more than 70%.

2.) During the same period, allocations to French banks have more than tripled. And in the last month, when overall European exposure dipped, exposure to French banks continued to gain reaching 6.5% of the MMF Fitch sample.

3.) But versus the peak exposure in May 2011, MMF current holdings are significantly lower. The big gainers since May 2011 were Japanese bank liabilities and to a lesser extent Australian bank issuance and US Treasuries.

This is all pretty sensible. MMFs actively manage their risk, moving away from issuers they perceive as risky. As the crisis abated, largely a function of the ECB pumping money into the banks via the LTRO, MMFs started to come back in. Now that stronger banks have started paying down their LTRO obligations, will this increase their demand for external funding and eventually make their way onto the MMF’s balance sheets? In any event, the bifurcation of the market between the weak vs. the strong continues.

Why did the French banks go up in the past month when other European banks shrank? We have heard that several large money market funds extended their credit lines for European banks from 3 to 6 months. French banks were posting the highest rates on the longer maturities and the cash went to them. The French have backed off their rates now and we’d expect the next reporting period to show either a marked slowdown or reversal of the trend.

Another point worth looking at was the fall in repo exposure by the MMFs. Fitch reported that “…the proportion of European and eurozone exposure in the form of repos decreased markedly, a reduction in secured exposure that might to some extent indicate an easing in MMF risk aversion to the sector ….Aggregate repo exposure represented about 15% of total MMF assets at end-December, down from 20% of MMF assets at end-November…” The UST/Agency repo market had some strange technicals last year, with supply overhang forcing rates higher than one might expect. Bank balance sheets were clogged with paper as receding risk aversion encouraged investors elsewhere. As banks trimmed their balance sheets into year end, repo levels came back into line. This trend has continued into 2013 with repo rates in single digit territory. The expiry of TAG is one reason cited for the continued repo rate crunch.

A factor to consider may be the desire to term out repo funding to comply with Basel III and the LCR. Money market funds aren’t always interested in long dated repo and that could create a mismatch between what the MMFs wanted vs. what the banks were offering.

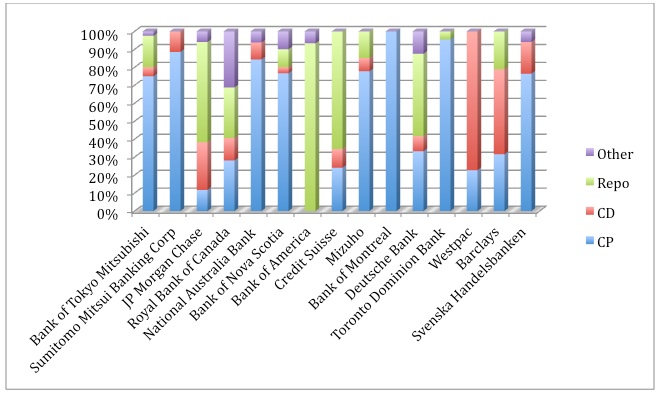

It is worth mentioning that the mix of funding between CDs, CP, and repo was a bit surprising to us. We took the Fitch sample data and looked at percentages by product for those banks. The graph is below.

What we thought was striking was that some banks, notably BofA, Credit Suisse, JP Morgan Chase and Deutsche did large percentages of their MMF business in the form of repo (93%, 66%, 56% and 46% respectively). Others like Sumitomo, Westpac, Bank of Montreal, and Svenska had zero repo. We are not sure if there is a reporting issue or the nature of the banks with zero repo reported push them toward unsecured liabilities. In a crisis, we wouldn’t want to be the guys who can only issue CDs and CP to fund themselves.

The article requires readers to register and log onto Fitch’s website (www.fitchratings.com) so we won’t link directly to it. But two good articles can be found here and here.