The FRB Senior Credit Officer Opinion Survey on Dealer Financing Terms (a/k/a SCOOS) came out recently and we wanted to share the results.

The SCOOS reports have been on the boring side recently; things have been pretty much the same. The special questions are usually where we usually like to focus. This survey asked asked about “…changes since the middle of 2012 in the provision of warehouse funding for commercial real estate (CRE) loans and syndicated bank loans on an interim basis prior to securitization…” and “…queried dealers about changes in client risk appetite since the beginning of 2013…”. Not barn burners, but there were some interesting trends (within the special questions as well as the standard set) which emerged.

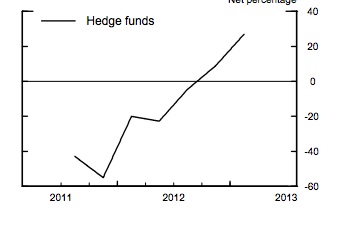

- “…more than one-fourth of dealers, on net, reported an increase in the use of leverage by hedge funds…”

- “…Almost two-thirds of respondents reported increased demand for funding of non-agency residential mortgage-backed securities (RMBS), whereas about two-fifths noted increased demand for funding of agency RMBS and commercial mortgage-backed securities (CMBS)…”

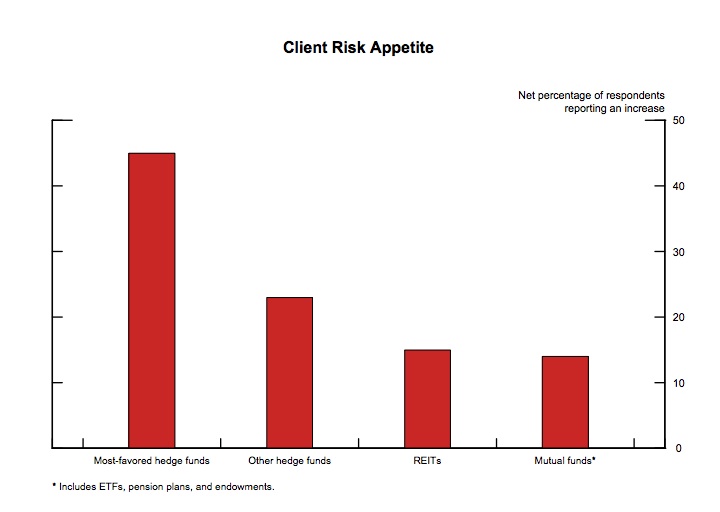

- “…Dealers reported that the appetite of most client types to bear investment risk had increased since the beginning of 2013..”

- In addressing Central Counterparties and other financial utilities: “…About one-fifth of survey respondents noted that the credit terms their institutions applied to clients on bilateral transactions that are not cleared had been influenced to a more than minimal extent by changes in the practices of central counterparties, including changes in margin requirements and haircuts…” We would expect that number to go a lot higher once the BCBS/IOSCO non-cleared derivatives are finalized. We wrote about this on February 19, 2013 “BCBS and IOSCO clarify non-cleared derivatives margin rules and allow broader collateral eligibility – the cake is almost baked” and on March 14, 2013 in “ISDA publishes a paper on Non-Cleared Swaps: rumors of its demise are greatly exaggerated”

- In looking at collateral for derivatives and margin terms, “…in a departure from prior survey responses, one-fourth of dealers reported a tightening in acceptable collateral, and one-fifth of respondents also indicated that requirements, timelines, and thresholds for posting additional margin had tightened somewhat over the past three months…” This was a little surprising to us.

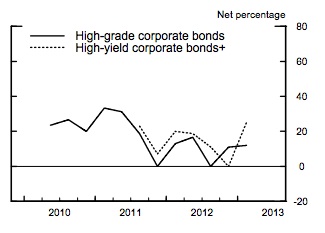

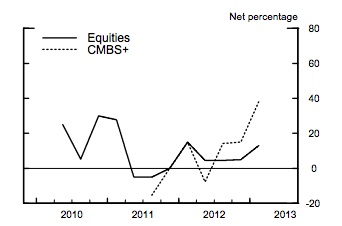

- On types of paper being financed, “…dealers reported that demand for funding had increased for a number of collateral types…In particular…an increase in demand for funding of securitized products. Almost two-thirds of dealers reported increased demand for funding of non-agency RMBS, while about two-fifths of respondents pointed to increased demand for funding of agency RMBS and CMBS. In addition, smaller net fractions of dealers reported increased demand for funding of high-yield and high-grade corporate bonds as well as equities…”

- Looking at term, “…Finally, respondents noted an increase in demand for term funding—that is, funding with a maturity of 30 days or more—for several types of collateral. Almost two-fifths of respondents reported such an increase with respect to high-yield corporate bonds, and about one-fourth with respect to agency and non-agency RMBS as well as CMBS…” We would have expected the dealers to be pushing lengthening of financing term, driven by LCR.

Some of the responses over time in graphical form:

Respondents reporting increased use of leverage

Respondents reporting increased demand for funding of:

Respondents reporting increased demand for funding of:

A link to the report is here.