On December 16th, 2016 Euroclear received regulatory approval from the Securities and Exchange Commission (SEC) to expand its exemptive order to include US equities. This cleared the way for DTCC-Euroclear Global Collateral Ltd (GlobalCollateral) to launch its Inventory Management Service, or IMS, covering not only US Treasuries, but also equities, corporates and asset backed securities. This represents significant progress in the global drive for a more efficient collateral utilization environment, allowing globally active US dealers greater flexibility in their use of collateral across two of the largest global market infrastructures servicing a combined $78 trillion in assets.

What is GlobalCollateral’s IMS?

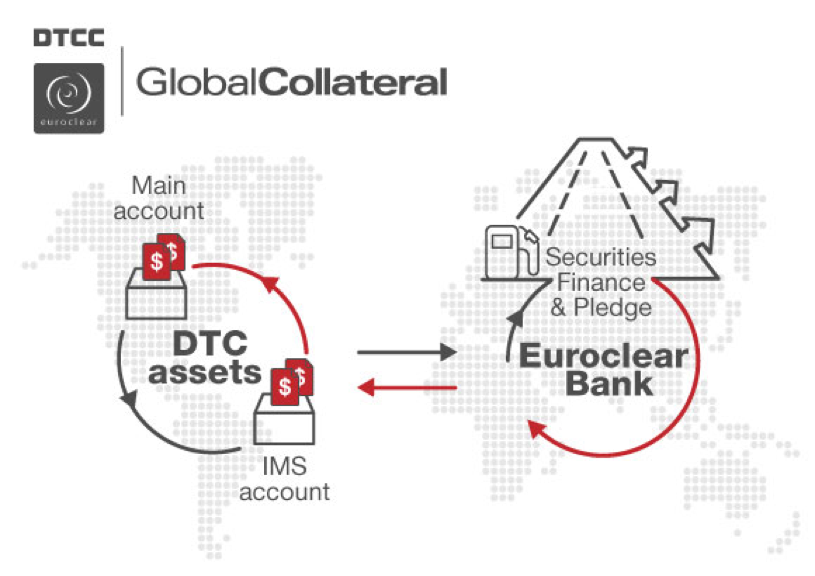

IMS is a solution that connects Depository Trust Company (DTC) and Euroclear assets to Euroclear’s Collateral Highway, where it can be used for triparty financing and pledge business (see Exhibit 1). It provides automated transfer, recall and substitution of assets. The idea is to ensure as broad a pool of collateral as possible is available for OTC derivatives margining in the US and Europe, and to expand the potential pool of trading partners in the securities finance markets.

Exhibit 1:

Connectivity of GlobalCollateral IMS

Source: DTCC-Euroclear Global Collateral Ltd.

The IMS value proposition: feedback from dealers

With IMS now live and providing a vital service in connecting collateral across US and European markets, Finadium spoke with dealers who could use the service. We sought to learn how the IMS functionality would be employed at their firm, what asset classes would be most important, how easy or difficult integration will be, and whether IMS is expected to create new business opportunities in global financing markets. Our conversations were confidential to encourage transparency in the responses.

Flexibility in the front office

Dealers were unanimous in saying that IMS will provide inherent flexibility in the front office financing process. Traders and collateral managers remain constrained in their deals by separate and inflexible inventories, and a lack of interoperability across geographies and asset classes. Silos still exist however and may be around for some time to come. While some dealers have or are moving to the central collateral funding desk model of aggregating collateral, this still does not solve the problem of moving assets easily between the US and Europe. The IMS, they say, eliminates an archaic way of viewing and mobilizing inventories. As one dealer noted, “With the technology that exists today, there is no excuse for silos. It should be easy to move collateral wherever it’s needed, wherever it can be most profitably used.” The IMS solution is “long overdue.”

Risk reduction

The ability to utilize US assets directly in the Euroclear environment provides a significant de-concentration of systemic risk by helping to spread the tri-party business across multiple venues. From a compliance and regulatory perspective, IMS allows dealers to better manage concentration risk and spread their business across a wider variety of counterparties.

Euroclear is a favored venue and highly respected for its capabilities in tri-party financing and collateral management. Prior to IMS, it has been an operational challenge – and a risk – for dealers to transact bilaterally in corporates and asset backed securities with counterparties who would much prefer to see this collateral run through the Euroclear infrastructure. The dealers we spoke with agreed that access to a broad universe of counterparties across the full asset mix was extremely important.

Centralizing inventory

Dealers noted that the traditional approach to trying to optimize collateral was always to centralize inventories. Firms have spent enormous amounts of time and energy tracking down dormant inventories across custodians and custodial locations, physically bringing it together into a central location, and then redistributing it back to where it is needed. IMS eliminates this complex process by providing virtual centralization without actual, physical centralization. “Overfunding and backfilling is expensive and risky,” one dealer stated. “IMS greatly reduces this problem.”

Utilization of non-Treasury assets

Dealers were interested in IMS for corporate bonds and asset-backed/mortgage-backed securities, with equites lower in importance, aligning with overall market conditions and practices.

“There’s no real change to the market model with IMS,” one dealer stated. “But that could change. Equities could become more important if they can be more efficiently utilized within more secure environments like Euroclear.” When operational risks level out across asset classes – meaning, where equity collateral is no more operationally challenging than higher rated assets – this could encourage greater utilization of equities in financing. Initially however, dealers expected IMS to simply make better use of their existing asset preferences.

Implementation: easy for IMS, a challenge for sophisticated collateral decision making

We asked how much effort dealers would require to incorporate IMS into their trading and operational environment. While implementation approaches varied, the consensus was that it was a relatively small effort. Most of the pipes and plumbing are in place operationally and technically, and additional work is largely centered on connecting existing systems. One dealer said: “On a scale of 1 to 10, it’s a 2. Pretty straightforward.”

Another reported a little more effort. “The issue for us is that our systems lack the sophistication today to look across the whole book in a multidimensional way. It’s going to take some effort for our systems to understand that collateral in multiple locations is really virtually in the same place.” Still, the dealer reported that will not prevent them from moving forward and getting the IMS in place, though they may not be able to utilize it to its fullest capacity without some “better decision making” in their existing systems.

The challenge of utilizing IMS to its fullest potential is reflective of a larger issue: collateral and securities finance systems need to be educated on a complex decision making hierarchy that goes beyond cheapest to deliver. Systems in many firms still have not fully come to grips with Liquidity Coverage Ratio (LCR) and other capital cost considerations. IMS will, they say, make the operational process of optimizing the collateral easier, but without more sophisticated internal tools to make complete decisions, dealers won’t be able to take full advantage of the opportunity. IMS may serve as a catalyst for firms to do the internal work that is required to make best use of the offering. Once the internal challenges are surmounted, implementing additional solutions becomes much easier.

Operationally, the consensus opinion is that IMS significantly reduces operational overhead. According to one dealer, “Operations today is constantly shoveling collateral around in a dozen different ways. IMS eliminates a lot of this work and risk. It takes a lot of pressure off.”

This fact alone has a substantial impact on dealers’ ability to efficiently mobilize their collateral. Having a single, integrated process for a large percentage of their business – and one that mitigates pressures on operations teams at the end points – will open them up to more counterparties. There are counterparties that do not want or cannot take on the current workload of a bilateral relationship. Getting the collateral into Euroclear’s existing operationally efficient infrastructure eliminates this problem.

Will IMS allow different financing structures in the future?

Dealers are focused on the immediate benefits of IMS within their existing structures, but that does not mean they aren’t thinking ahead. While the immediate benefits of greater collateral efficiency, access to a larger number of counterparties, and reduced operational overhead are their priorities for the short term, dealers offered some speculation on future possibilities.

A general theme is that the lower the operational burden of managing different collateral types, the easier it will be to utilize that collateral for OTC derivatives and securities finance transactions. There will always be concerns about liquidity risk, but if counterparties see asset classes like US equities as a check-the-box option in the Euroclear system, that may open up the market.

Alongside asset classes, product structures like collateralized FX swaps and Net Stable Funding Ratio (NSFR) term arbitrage trades for like collateral classes could become easier. “A globally integrated inventory just opens doors and possibilities. It will take some time for it to sink in.” The expectation is that once it does, dealers will be better positioned to think more creatively about DTC collateral and its relationship to the financing needs of the broader market.

This case study was commissioned by DTCC-Euroclear Global Collateral Ltd.