Fintech, or technological innovation used to support or provide financial services, has developed markedly in recent years, transforming the financial landscape and creating a number of challenges for public authorities. These challenges are particularly material for central banks, as the “future of central banking is inextricably linked to innovation”. The transformation of financial markets is affecting the way they conduct their policies to ensure, among their policies to ensure, among other objectives, monetary and financial stability as well the smooth functioning of payment systems.

As regards central bank statisticians and their need for high-quality data to support policymaking, fintech gives rise to a number of issues. For example, what are the data sources available to measure fintech and how are they actually used? Which additional information is needed to support the conduct of central bank policies, and what are the data gaps? How should these gaps be addressed, considering costs/benefits trade-offs and the various stakeholders involved? And how should adequate statistical frameworks be developed for collecting comprehensive information given the global nature of the financial system?

To shed light on those various issues, the Irving Fisher Committee on Central Bank Statistics (IFC) conducted a survey among its members in 2019. The main results are the following:

- Fintech is developing in the majority of the jurisdictions, through different channels. First, a growing number of recently incorporated entities leveraging on technology have emerged to provide financial services; they are particularly engaged in the provision of payments, clearing, and settlement services, as well as in credit intermediation. Second, traditional financial institutions are also embracing technologically enabled financial innovation and adjusting their business models accordingly; this is particularly the case for well-established credit institutions and payment service providers.

- The survey reveals a significant need for fintech data among central bank users, with the strongest requests expressed by those units in charge of payment systems. Information demands are particularly high in jurisdictions where fintech is the most developed. Users are typically interested in lists of fintech entities and on statistics on fintech credit.

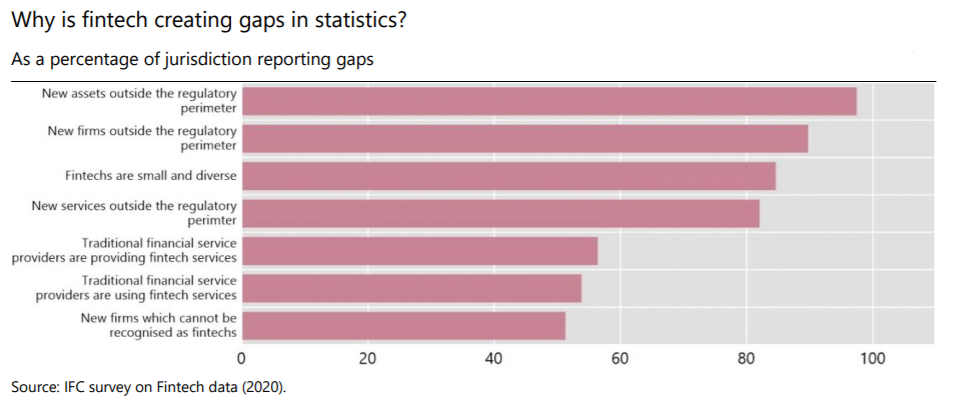

- Fintech creates important data gaps, reflecting three main developments. First, fintechs can be classified outside the financial sector if for instance they were initially set up as IT companies; such classification issues can be reinforced by the fact that these firms are often small, diverse, and not easy to identify. A second problem relates to the lack of granularity of the current statistical framework, since major data collection exercises group together non-bank financial institutions. For example, the financial accounts include a number of rapidly growing types of intermediaries providing financial services (eg crowdfunding, peer-to-peer lending) into the “other financial institutions” sector. Third, traditional financial institutions have been embracing innovation by sponsoring technological start-ups treated as directly controlled affiliates, implying that their fintech activities are blurred in consolidated groups’ reports.

- To close these data gaps, it is key that fintech entities be adequately covered in the statistical reporting perimeter. The guiding principle is that financial service providers shall be classified according to the main economic activities they perform, independently of the embedded technological intensity. Currently, central banks are applying this principle in an ad hoc manner, by assessing new fintech firms on a case by case basis in close cooperation with other domestic authorities – eg national statistical offices (NSOs).

- Official business classification systems should be revisited to ensure that firms engaged in financial intermediation are systematically classified in the financial sector. The ongoing revision of the International Standard Industrial Classification of All Economic Activities (ISIC) provides a key opportunity to enhance the classification of various fintech service providers such as neobanks, entities engaged in crowdfunding, robo-advisers or payment processing companies.

- Half of the central banks have launched initiatives to close data gaps, with the primary objective of updating the lists of financial entities and adjusting reporting requirements. In most instances, this work is done by collecting data from financial intermediaries (eg regulatory reports) and publicly available financial statements. Information provided by industry associations and business registries can also be helpful. In contrast, only a few central banks report initiatives to collect fintech data directly from the users of financial services (eg household financial surveys), despite their potential usefulness to assess the impact of fintech on financial inclusion.

- The majority of central banks report regular cooperation with other domestic authorities, which is essential to adequately cover fintech firms in official statistical frameworks. There is also a demand for stronger international coordination, not least to enhance classification standards and develop harmonized cross-country statistics, a precondition for any meaningful analysis of fintechs’ impact on the global financial system.