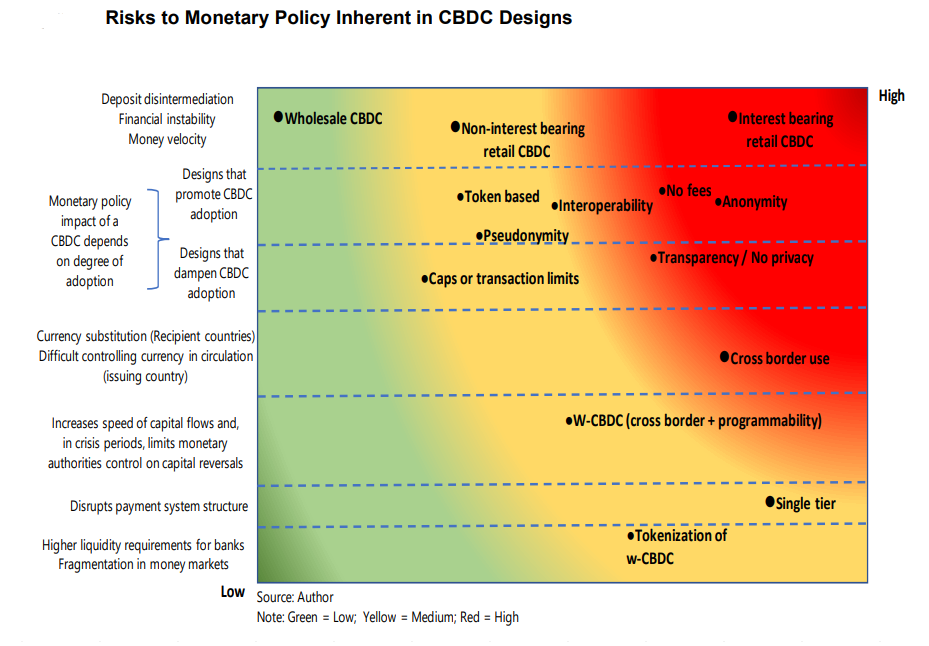

A report from the International Monetary Fund (IMF) details how central bank digital currencies (CBDCs) promise many benefits but, if not well designed, they could have undesired consequences, including for monetary policy. Issuing an unremunerated CBDC or a wholesale CBDC does not change the objectives of monetary policy or the operational framework for monetary policy.

CBDCs can, however, induce changes in the retail, wholesale and cross border payments that have negative spillover effects on monetary policy, through their effects on money velocity, bank deposit disintermediation, volatility of bank reserves, currency substitution, and capital flows.

Countries most vulnerable are those with banking systems dominated by small retail deposits and demand deposits, low levels of digital payments and weak macro fundamentals. Proposed CBDC design features, such as caps on CBDC holdings and unremunerating the CBDC can moderate disintermediation risks, but they are not sufficient. Central banks will need to ensure that unintended macroeconomic risks are comprehensively identified and mitigated.

The liquidity conditions in the banking system and the response of banks to the sudden withdrawal of deposits could mitigate or amplify the risks. The impact on monetary policy will be more pronounced if bank reserves are generally low or if there is uneven distribution of the reserves across the banks. The impact could also vary depending on whether commercial banks make up for the decline in deposits by borrowing from the interbank market or seek recourse to central bank financing.

The risks are highest in crisis times when the precautionary motive surpasses the transaction motive but could also be high at the inception of CBDCs when there is “en-masse” opening of CBDC wallets by the public. The impact will also depend on the speed of CBDC adoption.

In both the transition and crisis scenarios, banks may have to scramble for alternative funding sources or central bank financing. If commercial banks exhaust their collateral, the central bank will need to expand acceptable collateral or lend uncollateralized, and depending on the quality of the collateral, the risk on the central bank balance sheet could increase. Increased demand for central bank financing could lead to a spike in the repo and policy rate and force the central bank to provide reserves to commercial banks. An expansion of the central bank balance sheet, if not accompanied by a corresponding increase in output could lead to higher inflation.

The availability of Sharia’h-compliant money market instruments for interbank transactions and liquidity management vary across countries but the market is mostly underdeveloped. A few countries (Malaysia, Bahrain, Indonesia) have made advances in developing Sharia’h compliant liquidity management tools and interbank markets, but many others do not have any Islamic repo facilities with central banks or have a very limited offering. The basic infrastructure necessary for a market-based Islamic monetary policy (Islamic money and Sukuk markets) are also lacking. Islamic banks, therefore, tend to hold more cash than necessary.