ISDA published on February 5th a research note “Interest Rates Derivatives: A Progress Report on Clearing and Compression”. It is an interesting analysis on the progress made in clearing interest rate derivatives.

The underlying message is that 90% of interest rate derivatives that can be cleared are, in fact, cleared.

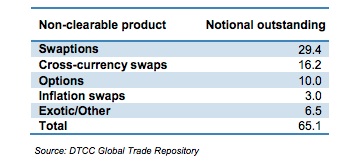

So what can’t be cleared?

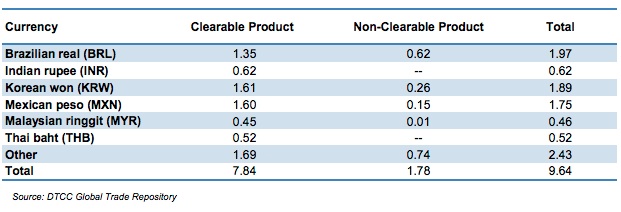

“…Approximately $73 trillion, or 13 percent of the IRD market at June 30, consisted of non-clearable transactions. This includes $65 trillion in products that cannot be cleared, and $8 trillion in products that can be cleared but are denominated in currencies that cannot…”

The chart below illustrates the types of trades that are outside of the central clearing mechanism.

The products that can be cleared but are denominated in currencies that don’t have central clearing include the Brazilian Real, Korean Won, and Mexican Peso.

It is impressive that so much of what can be cleared does pass though CCPs. Legacy trades with highly rated counterparties often had no IM – so to persuade those clients to novate to CCPs takes a lot. Not only is there the additional cost of collateral to be pledged, but also the complexity of managing that collateral. Neither should be underestimated. Anecdotally, we have heard that dealers are not aggressively pressing highly rated clients to novate deals, leaving lots of bilateral trades outstanding. The non-cleared trades will unwind over time, replaced by cleared deals — but this is lengthy process. The ISDA data suggests that the process has been largely accomplished. We would like to see data that differentiates inter-dealer trading (which is the lions share of the market) versus financial (e.g. non-clearing exempt) client trades. LCH data has suggested the ratio of total cleared trades to buy side cleared trades is something in the order of 8~10 : 1. This skew has the potential to obfuscate conclusions about how many buy side clients are actively moving their portfolios to CCPs. The dealer banks were motivated — better capital treatment alone would create a big push toward clearing. We wonder how many clients demanded (and received) compensation to make the switch? Or was facing a CCP seen as a better risk and enough incentive?

The piece also addresses trade compression. From the article:

“…Compression, also called trade tear-ups, reduces notional outstanding by eliminating matched trades or transactions that do not contribute risk to a dealer’s portfolio. Compression has helped to reduce the IRD notional outstanding by approximately 30 percent since 2009…”

and

“…While compression reduces notional outstanding, central clearing increases it. If, for example, two parties execute a $100 million swap on a bilateral basis, only one $100 million contract exists. If the same transaction is booked through a clearing house, it will be booked as two $100 million contracts, or $200 million in total…”

We have always been impressed by the ability to compress trades and the technology behind it. It is a key risk reduction tool and should be expanded whenever possible.

The point about double counting is important. Too often derivatives markets are judged by sound bites about the notional amounts. The numbers are huge by any metric. But as we have written before, notional is not a good way to measure the risk involved. Derivatives typically have a PV of zero when traded – and it is the PV relative to the collateral and market liquidity for that collateral that really drives risk.

1 Comment. Leave new

Unpicking the 90% the stat flatters progress. Of the 90%, 33% is cumulative compression to date which while helped by clearing consolidation but isn’t actually clearing. 28% is double counting elimination (clearing creates two trades for every one original trade – hardly a benefit of clearing). When you look at open single sided notional where the clearing is available for the product only 74% is cleared and 15% of the balance is between non-exempt financial parties.

Also if you look at the BIS half yearly OTC survey you can see that a surprisingly small fraction of the total open notional is C2D – implying the banks have not backloaded quite a bit of clearable product (which they are entitled to do but which becomes more and more of a burden as Basel III ratchets up).