Last week in the York Fed’s Liberty Street Economics blog they published an article “FRN Follow-Up: Who Are the Market Participants?” We thought it was interesting and take a look.

The FRNs “…pays a fixed spread over the floating thirteen-week bill rate rather than a fixed coupon…”.

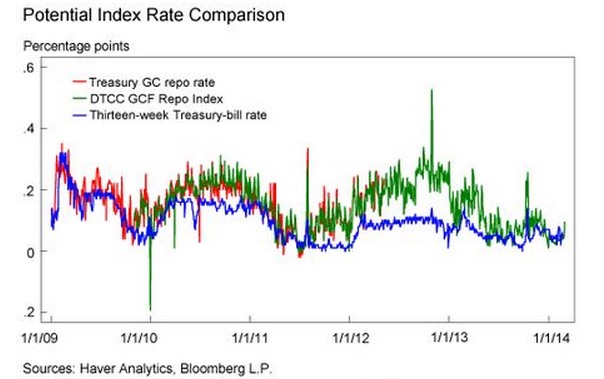

There had been some discussion when the security was first proposed what it would be indexed to. We liked the idea of a repo index linked instrument, but it was not to be. From an April 21, 2014 Liberty Street Economics blog post “Introduction to the Floating-Rate Note Treasury Security”, here is a comparison of Treasury GC repo rates, the DTCC GCF Repo Index, and Thirteen-week Treasury-bill rates:

Form the April 21, 2014 post:

“…Most commenters supported the use of the GC rate and, more specifically, the Depository Trust & Clearing Corporation general collateral finance repurchasing agreement rate index (DTCC GCF Repo Index). They cited the daily rate changes, the greater nominal value traded in GC agreements, and the potential to attract new investors as advantages, while noting the potential conflict of interest and minimal cost savings in benchmarking a Treasury note to a Treasury bill rate as detractors from using the thirteen-week bill. However, others favored the thirteen-week Treasury bill, citing disadvantages with using the GC rate, including higher daily rates and volatility than bill markets, the relative newness of the GCF indexes, and the possibility of exposing Treasury’s financing costs to private-sector rate shocks. In the end, Treasury decided to benchmark the FRNs to the thirteen-week bill in light of its long history and high liquidity. The final structure is detailed in the table below, and the interest rate on the first FRN can be tracked in the following chart…”

and on who would be the investors?

“…Money market funds may be attracted to even a modest yield pickup over Treasury bills, and although they are bound by their statutory weighted-average life of 120 days, most are currently well below this cap. Banks, on the other hand, are less likely users of FRNs, as they can currently leave excess reserves at the Federal Reserve and earn a return of 25 basis points, while FRN’s currently trade with a total return around 10 basis points (discount margin + current reference rate). However, Basel requirements may encourage banks to invest in short-duration, high-quality instruments such as FRNs when pricing conditions become more attractive…”

So who did end up buying the paper? From the January 14, 2015 post:

“…Investment funds and international investors consistently bought the bulk of the FRNs not taken down by primary dealers at auction. This is consistent with the prediction in our previous post, in which we suggested that foreign central banks and money market funds would be the most likely ultimate investors, while the yield would be too low to attract depository institutions that can earn interest on excess reserves (IOER) of 25 basis points…”

and

“…Money market funds (MMFs) are natural holders of FRNs because these securities provide a slight yield pickup over similar duration bills, and many MMFs are well below their weighted-average-life (WAL) caps…”

MMFs see the FRNs as an alternative to (rolling over) T-bills and, to a lesser degree, repo. It seems like a safe way for funds to minimize interest rate risk, reduce transaction expense, and still pick up a bit of yield for their trouble. Watching out how close the funds are getting to the weighted-average life caps will be a good indicator of their demand for the paper. But as the Fed noted, the MMFs are below their WAL caps at the moment.