Securities Finance Monitor spoke with DTCC’s senior SFTR Trade Repository leadership about the importance of the client side of the Securities Financing Transactions Regulation (SFTR) and why DTCC dedicates so many resources to this aspect of the business.

To be a leading trade repository (TR) requires more than increasing the efficiency of regulatory reporting. It also demands assiduous maintenance of a global infrastructure, sustainment of a comprehensive onboarding and client service programme, and development of a value-added ecosystem for client benefit.

Building a Global Infrastructure

SFM: What does it mean to have a global infrastructure?

Val Wotton, Managing Director, Product Development and Strategy, Derivatives and Collateral Management for DTCC: DTCC’s global infrastructure, which reflects our experience operating trade repositories across all major geographies, uniquely positions us to support our clients in meeting their regulatory requirements globallyand strengthen our relationships with regulators around the world. Our global footprint also enables our clients to reduce their overall reporting costs by leveraging common infrastructure and connectivity and gives them a consistent user experience across jurisdictions.

SFM: What did it take to build out a global platform?

Wotton:Our initial design for trade reporting was a platform whereby a single trade reporting message could be directed to the required regulatory jurisdiction. Unfortunately, a couple of things happened to change the approach: first, the industry initially looked to build out by asset class. Second, as reporting went global and began to expand beyond derivatives, regulations were not harmonized across jurisdictions and traded products.To address this fragmentation DTCC had to support multiple TRs around the world. We decided to simplify this structure by creating a TR platform and infrastructure that can function across jurisdictions and products to serve each of DTCC’s TRs and their clients.

We now have one configurable, global TR code base that can efficiently support new products and jurisdictions. There are three recent examples of this capability: Swiss reporting under FinfraG; separate trade reporting in the UK post-Brexit and the European Commission’s adoption of SFTR in response to the FSB’s [Financial Stability Board’s] 2013 recommendations to address the risks of securities finance transactions [SFTs] through trade reporting. The fact that our platform will accommodate FinfraG, SFTR and Brexit is concrete evidence that the significant work we have done to create a global platform, including product development and technology infrastructure, is benefiting our clients. And, by the way, while EU [European Union] SFTR is the first, we’ll be able to handle additional SFT reporting mandates as they are enacted in other jurisdictions in coming years.

Equally important as our platform work is our ongoing collaboration with the industry on new product development and service delivery. We’ve learned a tremendous amount through these collaborations.

SFM: What is your relationship like with the regulatory community?

Wotton: Because each authorized TR needs to be approved in each jurisdiction and there are differences by country and product and stringent rules that all TRs must follow, we’ve learned the value of spending time on advocacy with the regulatory community at all stages of the process – from pre-regulation to implementation and production.While you can see our public comments on proposed rules or rule changes, our vigilance in educating regulators about the market is not publicly visible. We strive to help regulators understand the challenges facing clients and TRs in carrying out new mandates. Through these efforts, we have become part of the connective tissue between regulators and the industry, working to assist regulators in understanding what result they will obtain from their rules and help the industry know what to expect. In the end, we are seeking to make requirements across jurisdictions more consistent to better reflect a global market.

Mark Steadman, executive director, European head of Product Development for DTCC’s Repository and Derivatives Services:We have invested heavily in government relations to support our TR service. Our regulatory relations and compliance teams include former regulators in the US and Canada who were involved in the international regulatory response to the financial crisis – giving us added insights into the regulatory perspective.

In some cases, we began meeting with policymakers three years before the introduction of regulations. Regulators are a key constituency for our services as the ultimate consumers of the trades reported to TRs. Now that data reporting has matured, there is recognition of the value the data can provide, including by informing policy decisions. The more we can provide useful input on policy, from consultation all the way to final regulation, the better the outcome can be for all parties. We see ourselves as a fundamental partner in the trade reporting ecosystem.

SFM: Why should clients care about a global infrastructure if SFTR covers only Europe?

Wotton: A global infrastructure matters for SFTR because of the breadth of clients affected and who is in scope. Because SFTR effectively has global reach, clients around the world are forced to pay attention to these obligations.When SFTR is implemented in 2020, EU-based firms, including their non-EU-based branches, and non-EU-based firms whose transactions are executed by an EU-based branch will be required to report their SFTs to an authorized trade repository.

Since SFTR is part of the G20’s commitment to monitor risk and achieve transparency in financial markets, clients will also take notice when other jurisdictions follow with their own securities finance reporting rules. It is very possible that requirements in other jurisdictions will differ from SFTR in what and how to report. For example, the US initially plans to mandate the reporting of CCP-cleared repo transactions. By contrast, the Bank of Japan in coordination with the JFSA [Japan Financial Services Agency] requires reporting of Japan’s SFTs directly to JFSA rather than to a TR. Other regulators in the Asia-Pacific region may end up taking a different approach.

Fortunately, because our global platform is designed for flexibility by product and jurisdictional reporting obligations, it can easily support clients in managing these differences. As our clients look to us to help solve their reporting challenges, our global infrastructure will be critical to achieving that goal.

Another way our global platform benefits clients is by addressing the cost of global reporting. With more regulation in the pipeline – from the CFTC [US Commodity Futures Trading Commission] and amendments to EMIR [European Market Infrastructure Regulation] via Refit – the rising cost of regulatory compliance is a huge challenge for the financial services industry globally. Helping to reduce industry reporting costs is one of our long-term objectives.

SFM: DTCC promotes its “comprehensive onboarding support and client service” approach. What does comprehensive mean in this context?

Simon Farrington, Regional Administrative Manager, EMEA, and Managing Director, Client Service New Initiatives for DTCC: For us,comprehensive means serving clients throughout their trade reporting lifecycle –from project inception to testing, go-live and BAU support –to ensure they are operationally ready to meet their reporting obligations. There are four key elements in our approach that link together to form a coherent client service delivery programme:

- We have a flexible and proven TR platform, which has enabled us to quickly provide client solutions that allow our community to accommodate FinfraG, the demands related to planning for Brexit as well as SFTR.

- We offer a robust set of testing tools and training programs and a level of support that focuses on minimizing the client build-out effort.

- We provide 24/6 production support and 24/5 UAT support.

- We provide these tools and services at no additional cost to clients.

DTCC Comprehensive Global Client Service and Support

Source: DTCC

SFM: Please describe your consultative approach to product and service delivery.

Farrington: It starts with advisory groups and with regulators: we share ideas and consult with clients and stakeholders all the way through to go-live. We have built and continue to enhance some of our tools, such as our testing simulator, with client input.

SFM: Speaking of the simulator, what happens when firms fail this test?

Wotton: The simulator is a pre-UAT tool, so it doesn’t yield fails so much as works-in-progress to give a client visibility as to whether a message will receive an ‘acknowledged’ (ACK) or ‘negative acknowledged’ (NACK) as part of the TR ingestion process that validates the trade message against the mandated message schema. The simulator helps firms build out their messaging specifications and test in real time. When test messages are unsuccessful, clients can see what didn’t work, fix the issue, then move forward into UAT with confidence.

Steadman: The simulator allows early testing ahead of full industry UAT, to give clients confidence that their messages will be accepted by the TR. The industry UAT period can then be maximized by focusing on the quality of client reporting, reporting best practices and pairing and matching testing.

Farrington: We are constantly listening to and working with our clients to develop and deliver tooling that simplifies and increases the effectiveness of their testing and UAT cycles. Early delivery of the simulator, which we make available at no extra cost, illustrates our commitment to support our clients wherever we can.

SFM: How would you describe your model for production support?

Farrington:Our support model is informed by industry insights and best practice through our partnership with the Consortium for Service Innovation. It is further moulded by an ongoing, multi-channel feedback loop with our clients involving Relationship and Client Service Managers. This approach allows us to continuously evolve our support practices to meet the changing demands in the industry. Recently we began offering knowledge-centred support, which gives us a platform to resolve issues more consistently and respond to clients in a timely fashion. We’re also exploring the adoption of Agile practices across the support organization to streamline client entry points as well as push knowledge and skills closer to the initial client interaction.

SFM: How does industry engagement support client service?

Adem Sabah, Director of Product Development for DTCC’s Repository and Derivatives Services:As an industry-owned utility, our role is to help the industry through this major reporting challenge. Our client channels are established but SFTR is bringing in a new group of stakeholders, including firms not familiar with trade reporting and the regulatory expectations around it. We are active in industry forums –for example, ICMA [International Capital Market Association], ISLA [International Securities Lending Association] and AFME [Association for Financial Markets in Europe] –and have been at the forefront of industry outreach. By bringing user, regulatory and vendor stakeholders together in our own group and industry working groups, we are leading the effort to make SFTR implementation as straightforward as possible.

Creating a Value-Added Ecosystem

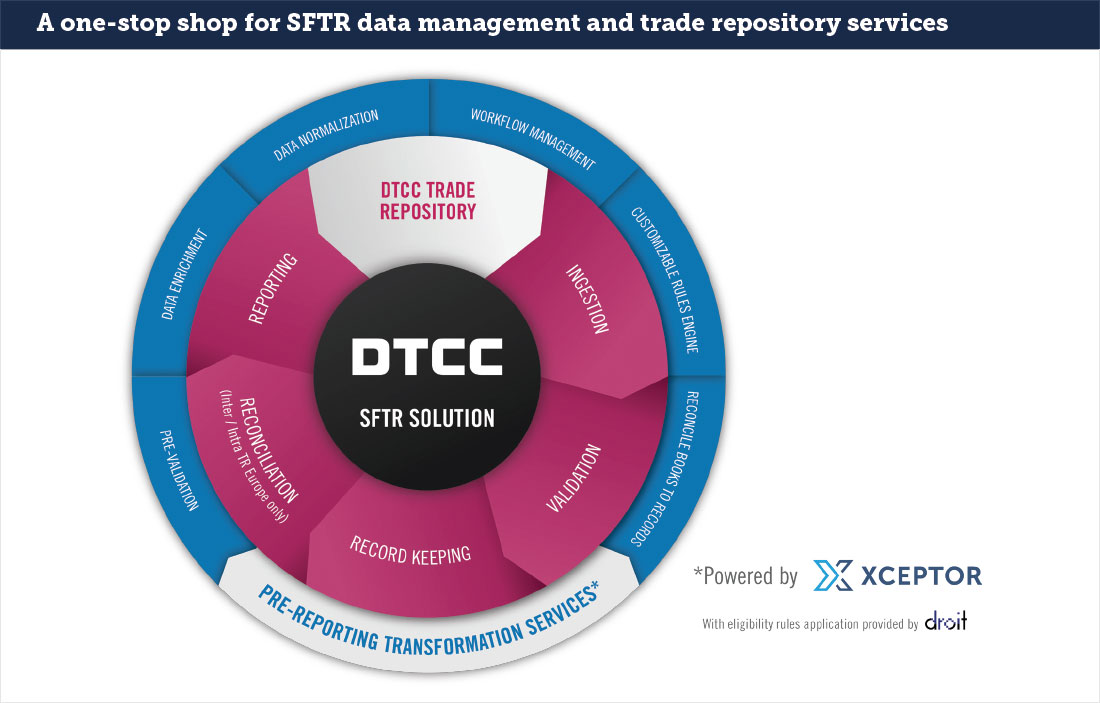

SFM: In the context of SFTR, what is a value-added ecosystem and how does your recent partnership with Xceptor for data transformation contribute to this ecosystem?

Wotton: At DTCC, our Pre-Reporting Transformation Services are central to our creation of a value-added ecosystem because firms are seeking support to ease the end-to-end process of trade reporting. We have now packaged up a number of services for data transformation and enrichment, including conversion to ISO 20022 format, the industry standard for messaging, and checks like Legal Entity Identifiers (LEIs). Once we have transformed the data, enriched it, and applied firm-specific elements, we can conduct a pre-validation check. Clients can view the results on a dashboard, identify approved messages, then investigate why the remainder are failing by leveraging the detailed reason codes.

Xceptor is our first partnership to help clients transform data. Xceptor’s entire business is data-centric intelligent automation, capturing data in whatever format it may lie in the organization, across any channel, and preparing it for one format like an SFTR submission. This pre-reporting transformation process is a recurring challenge for clients and one where DTCC, as a central utility, is positioned to help deliver an industry-wide solution.

Our transformation services play an important role in data enrichment as well. Giving firms the ability to enrich, normalize and validate data before submitting it to a TR will significantly streamline their operational processes and simplify SFTR compliance. With our new transformation services, firms will be able to enrich reporting with internal and external reference data, manage exceptions leveraging native workflows, and benefit from real-time gap analysis and testing in our simulator.

This process not only assists our clients in submitting to a TR, it also helps DTCC fulfil our regulatory obligations. Once a trade report is submitted, we must match transactions internally and across other TRs in Europe. We can then complete the cycle by helping clients reconcile with their own books and records, ensuring finality in the process and enhancing the client reporting experience.

Through innovations like our pre-reporting data transformation service we’ll continue to help the industry prepare for SFTR in 2020.

Learn more at dtcc.com/SFTR and SFTR@dtcc.com.