It seems that the era of mergers between physical and synthetic finance businesses is finally upon us. While client preferences may lean towards one type of trade vs. another, there is no question that regulation is the major driver of change. When faced with a request for a securities loan vs. a total return swap, the swap may be both easier and less capital intensive. In the long-term this will create broad-based new dynamics in financial markets. But in the short-term, our clients are working to manage complex implementation and technology changes.

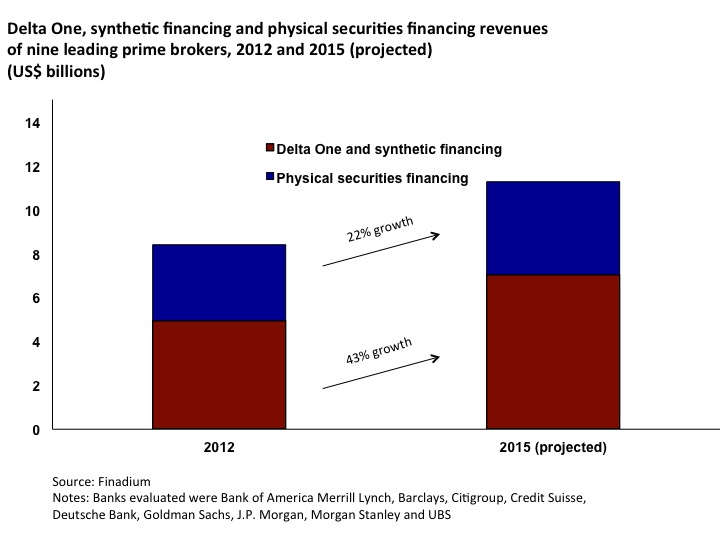

Data has suggested for some years that synthetic finance and Delta One desks were building momentum. Analysis by Finadium shows synthetic financing revenues at an estimated US$7 billion for 2015 across nine leading prime brokers, a growth of 43% over 2012 figures (see exhibit below). Physical financing revenues are estimated at $3.9 billion, just 61% of synthetic revenues. Physical revenues have also grown more slowly than synthetic, just 22% since 2012.

What is Driving Swap Growth Over Physical Transactions?

The reason for the growth of synthetic financing over physical has logical explanations, and the differences are only getting bigger. The primary driver being that capital regulations dictate that swaps are more easily accounted for than physical securities financing loans.

In just one example, in order to net down the balance sheet exposure on a physical loan, there needs to be an opposing loan with the same counterparty at the same clearing facility and for the same end date. This rarely happens in a bilateral transaction outside of high quality liquid sovereign debt markets; the opportunities are greater in the CCP environment. In an era of counterparty credit exposure limits, these things matter.

Whereas for derivative transactions, the balance sheet treatment is moving to the standardized approach for measuring counterparty credit risk (SA-CCR), a much more friendly capital treatment than what securities loans and repo receive. A swap transaction will carry XVA charges that are unavoidable but could potentially be netted, while synthetic financing desks then have opportunities to net down exposures on their own balance sheets across multiple counterparties. The outcome of these netting opportunities is that a synthetic financing book could, in theory, require less balance sheet for a bank or broker while leaving open credit lines between banks. Numerous other examples abound for why synthetics have gained momentum and more wild cards are still yet to be played, but capital treatment is at the heart of every discussion.

Why Merge Trading Desks?

As both financial markets and securities finance evolve, multiple pressures and opportunities are combining to make synthetic and physical desk mergers a potentially attractive opportunity for financial intermediaries. We hear the following points discussed when talking with clients:

- The ability to offer a suite of multi-product technology products is critical. Each individual client has their own financial goals but potential limitations or preferences in their trading styles.

- As business units and prime brokers seek to diversify or exploit their stronger revenue streams, they need to have ‘multiple products in the arsenal’, whether this be flow through CCPs, synthetics, optimization, etc. One desk managing swaps and physicals can provide a range of trades, up to and including offering one trade to the client then transforming that trade into something more attractive to other market participants.

- Cost reductions are an obvious reason to merge desks but this can only happen with changes to business priorities. Banks and brokers expect financing to become more costly, which means more sophisticated business and technology solutions.

- Banks and brokers may benefit from better risk management by consolidating like economic outcomes across their products.

Pros and Cons of Mergers

Like a train driven by regulatory fuel, synthetics are growing increasingly popular in the securities financing market. Benefits to synthetics may include happier regulators but do not extend to easier processing or more transparency, where physical transactions win on a consistent basis.

Market participants have recently commented that mergers of physical and synthetic desks would mean fewer people in the business. A consolidation of people could result in one trader for equities securities loans and Total Return Swaps, and so on. Reducing headcount could mean a loss of specialized expertise on trading desks as traders are forced to focus on easily replicated, vanilla transactions instead of custom trades that could improve market efficiency and benefit both sides. This would be a net loss to the industry.

At SunGard, this lack of trader specialization and blurred responsibilities at our clients could result in more technology products that provide broader general functions, as opposed to products with deep functional needs that are focused on specific silos or trading strategies. A growth in mergers would mean a reduction in the focused technology services that we expect to offer our clients; and a move towards newer technology solutions.

We suspect that mergers of physical and synthetic financing businesses may not serve the best interest of all market participants but will instead be unique to each organization specific needs and objectives. So long as capital treatments benefits synthetics so clearly, this evolution is inevitable.

Moving Towards New Technology Solutions

The task for any technology firm is to foresee market trends and ultimately react to the needs of our clients, whether that be new markets, regulatory requirements or evolving business strategies. In this vain, the growth of the synthetic securities finance market provides both challenges but ultimately opportunities.

At SunGard, we have many market leading comprehensive products which are silo based on legacy market structures. Our task is to provide our clients with more holistic solutions (not products) that match the evolving needs of users. Following on from the previous ‘on trend’ amalgamation of securities finance and collateral for the Apex solution suite, new opportunities now exist with synthetics and more vanilla physical securities finance.

As a result, SunGard are focused on delivering a Synthetic Securities Finance solution, incorporating synthetic prime (ETD and OTC), Delta One and securities finance leading functionality in a single solution suite. The offering can be delivered as a fully hosted solution and tied to the full range of services provided by SunGard that deliver key value and efficiencies.

Tom Dibble is head of product management for securities finance at SunGard.