The New York Fed’s Liberty Street Economics blog did a post on July 20th: “Have Dealers’ Strategies in the GCF Repo© Market Changed?”, written by Nina Boyarchenko, Thomas Eisenbach, and Or Shachar. They want to know how regulatory changes have impacted repo markets. Has repo activity shrunk across the board or did specific strategies become too expensive to pursue and fell away? Or both?

The piece looks at the General Collateral Finance (GCF) market, and specifically US Treasury and agency collateral, as a proxy for the entire market. For those not familiar with GCF,

“…GCF Repo is a service provided by the Fixed Income Clearing Corporation (FICC). It was introduced in 1998 by FICC and the two clearing banks Bank of New York Mellon and JPMorgan Chase to reduce transaction costs and enhance liquidity in the interdealer repo market. FICC serves as the counterparty to all trades. The market is blind-brokered so the cash lender and borrower do not know each other’s identity. Netting members of FICC’s government securities division are eligible to participate in GCF Repo…”

FICC has the look and feel of a central counterparty clearing house (CCP). For example, FICC serves as the counterparty to all trades. There are some differences versus how derivatives CCPs work.

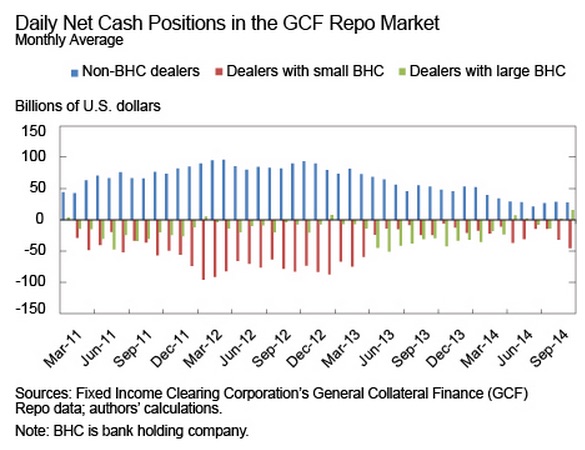

The article divided up the three major participants in FICC: Non-Bank Holding Company (BHC) dealers, Dealers that are part of small BHCs, and Dealers with large BHCs. Large BHCs are defined as having more than $500 billion in assets.

Each type of entity uses repo for slightly different purposes. Dealers seemed to have similar strategies based on what category they fell into. Looking at net cash positions, non-BHCs are net borrowers of cash pretty consistently. This should not come as a surprise given that repo is an efficiently way to fund and non-BHC dealers don’t have as many options to source cash as bank-related dealers.

Dealers that are part of small BHCs looked to be the mirror image of non-BHC participants, typically being a lender of cash versus receiving collateral. Again, this should not be such a big surprise. Small-BHC dealers are probably not trading repo around so much, opting to use it as a cash management tool to put their liquidity to work.

Dealers that are part of large BHCs were also net lenders of cash, although not 100% of the time and had net cash lending that was lower than dealers associated with small BHCs.

It is worth noting that around May 2013 dealers affiliated with small BHCs, who had been the primary source of cash in repo, fell away and dealers with large BHCs stepped up their cash lending. However this was also at the time when the scale of GCF repo markets started to shrink. The authors wonder if this was due to SLR or other regulatory constraints?

It is worth noting that around May 2013 dealers affiliated with small BHCs, who had been the primary source of cash in repo, fell away and dealers with large BHCs stepped up their cash lending. However this was also at the time when the scale of GCF repo markets started to shrink. The authors wonder if this was due to SLR or other regulatory constraints?

“…As a group, affiliated dealers typically lend cash to unaffiliated dealers. The funding raised by non-BHC dealers peaked at $93 billion per day in December 2012, but since the beginning of 2013, there is a general decline in activity, which reached its lowest level in our sample period in August 2014…”

So was the decline in repo activity the result of changes in strategy or just an overall scaling down of the market? The analysis looked at the activity divided by collateral type: UST versus Fixed Rate Agencies. Dealers with large BHCs typically lent UST and borrowed Agencies, doing a “collateral downgrade trade”. This sounds like dealers using balance sheet, earning the spread. But this changed in the beginning of 2013 when dealers with large BHCs started, on a net basis, to borrow both UST and Agencies. Does this change in the market implies a shift in strategy? The Fed doesn’t think so. We wonder if this isn’t when internal balance sheet charges started to make these kinds of trades uneconomic?

“…Since we do not observe a change in the propensity of dealers to receive cash or to deliver cash over the sample period, it seems that the downward trend in net activity is due to reduced activity rather than a change in dealers’ strategies…”

Non-BHC dealers continued to use repo to raise cash against both UST and Agencies, consistent with a strategy of using repo primarily to fund themselves and not engage in activity that would consume balance sheet unnecessarily. But even so, right around the start of 2013 non-BHC dealer activity shrank, especially in Agencies.

So with the typical flow of dealers with small BHCs funding non-BHC dealers shrinking in overall size, and dealers with large BHCs using balance sheet less to arb markets, has the repo market found an uneasy equilibrium or is it still in shrink mode?