The industry-wide topic of balance sheet optimisation has hung in the air like a fog for the last three years. We at Societe Generale are now seeing what this means in practice across our physical and synthetic prime financing business with important consequences not just for us but for prime brokerage as a whole. In this article I break down some of these changes and offer ideas about some of the outcomes for the prime brokerage industry.

The Regulatory Background

While often commented on, any analysis of changes to the prime brokerage financing marketplace must start with regulations; this is the major driver of our industry today and cannot be ignored. For prime brokers, the regulatory impact crosses between broad categories and small, specific changes that impact our business behavior. The primary considerations in my mind are:

- The Liquidity Coverage Ratio – we are especially aware of our expected liabilities in a 30 day period

- The cost of operational deposits from hedge fund clients. Now that there is an explicit outflow rate, no prime broker wants to hold client cash.

- Counterparty credit risk analytics. Across cleared and bilateral transactions, we assess even more carefully than before the cost of providing services against each counterparty.

- Additional costs for internalising securities loans. This encourages synthetic transactions over physical, which is an area of strength for Societe Generale and is driving other prime brokers to expand their synthetic offerings.

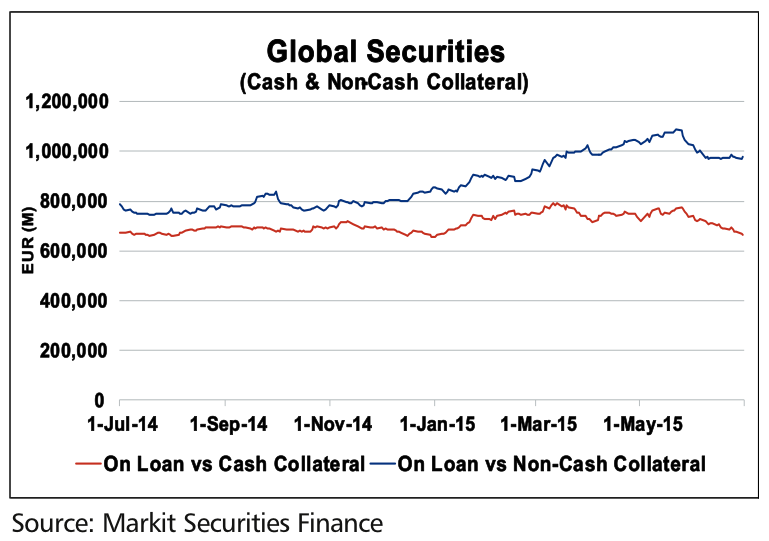

On the physical side, the growth of non-cash collateral usage is tangible. Data from the latest ISLA Market Survey, based on Markit Securities Finance, show that non-cash collateral is now 60% of the market, up from 50%-55% last year (see Exhibit 1). Non-cash provides our clients and counterparties with a risk-adjusted alternative to providing collateral, and ourselves as well.

Exhibit 1: Use of cash and non-cash securities as collateral in securities lending

Balance Sheet Management and Prime Brokerage at Societe Generale

The regulations that curb balance sheet have driven our prime financing business to reassess some of our most basic business arrangements. Business as usual can no longer be assumed as the only successful strategy going forward. We are constantly assessing business lines viability on a Balance sheet management standpoint both now and in the future.

The biggest impact of regulatory changes is how Investment Banks management are working with new balance sheet metrics in allocating scarce resources to businesses. Historically, a big part of our business, as well as the business of other large European Investment banks with excess balance sheet, has been to finance other banks’ illiquid assets. This has relied on our wealth of assets that made cash inexpensive; taking in emerging market bonds or ABS in a repo or structured note was, at that time a profitable trade. A key driver of this business was the fact that Treasury departments did not mind us using balance sheet. We also did not face any meaningful restrictions on transactions between banks. Clearly, those days are done. Instead of inexpensive cash, we are now in a position where our access to balance sheet is limited, defined and carefully monitored with enhanced tools. Hence, we are all very much aware of our balance sheet consumption and how to optimise and prioritise some business activities.

In response to the new regulatory environment, Societe Generale (and other prime brokers) has gradually elected to focus their efforts on client business, and this directly takes away from providing financing to other banks. As a matter of fact, scarce resources are allocated to businesses with the best client-facing use. This either no longer includes financing other banks’ assets or means a significant reduction; after all, we can no longer ask for additional balance sheet resources from the Bank’s Treasury simply because an opportunity is there; we must work within the dual requirements of the new regulatory framework and Societe Generale’s internal balance sheet requirements. Often this means, as a business line, we are more and more incentivised in being self-financing. That also means that clients who think about self-financing themselves get an increased priority.

An important part of our strategy is the full acquisition of Newedge. This clearing business offers us the ability to provide client access to futures exchanges (and CCPs) around the world that is capital efficient. A robust prime brokerage business must offer a range of services to clients, and clearing has emerged as by far the least capital intensive. The more business we can promote through clearing channels, the more business we can conduct. The counterparty risk weight alone leans towards clearing, not to mention the margin costs.

Societe Generale Corporate and Investment Bank, where prime brokerage (including Newedge) reside, now offers access to over 125 markets worldwide. We clear commodities, fixed income, FX and equity derivatives with an 11% market share in Listed Derivatives. This focus on clearing might sound like a lot, but if we can offer our clients two competing transactions, one cleared on a CCP with low capital costs to us and the other a bilateral transaction that is balance sheet expensive, then the cleared trade should be better for both parties.

A contraction of balance sheet at Societe Generale and other prime brokers has been a long-standing dilemma for hedge funds in particular. A constriction of balance sheet at prime brokers worldwide means that not just small prime brokerage clients, but large ones too, may see balance sheet restricted according to the needs of regulators, internal capital requirements, market volatility or other factors. As with clearing, the lower the capital cost, the better the chances that clients will not see any balance sheet reduction. More expensive transactions like securities loans or bilateral swaps will be impacted first, compared to cleared products.

Possible Outcomes for the Prime Brokerage Industry

The evolution of regulations means a better usage of the balance sheet for our counterparties and clients: Bank to bank business is aimed to shrink while bank to client business is emphasised for profitability. So where does this leave prime brokerage? I see several ideas for how the business may change, including:

- Hedge funds must shift their expectations towards self-financing and the utilisation of clearing services. This is no ultimatum, simply that the realities of prime brokerage are that balance sheet and relationships cannot be guaranteed. Hedge funds know this and are working to diversify their sources of balance sheet and market access. The door to creating new relationships will not stay open forever though. Post Lehman Brothers, a lot of Hedge funds started to spread their business among many prime brokers. In the future, the consolidation in number of prime brokers that Hedge Funds use may help them to get the best service from the brokers they selected.

- Prime brokerage constricts enough that regulations loosen. We are nearing a tipping point where prime brokerage shrinks enough to damage financial markets. Prime brokerage facilitates a substantial amount of trading and clearing business; it does not just provide leverage (although that happens as well). Penalising prime brokers through special breakouts in regulation targeting hedge funds puts a damper on our ability to provide market liquidity. Regulators may recognise this and adjust some of the more onerous restrictions on our business, much as the current conversation on the Leverage Ratio may result in revised standards. One example for prime brokerage could be adjustments to netting rules that allow more cross-correlation between assets or counterparties.

- Large bank prime brokers will focus on clients who can dedicate the most “wallet” across capital efficient activities. In the process, this leaves smaller and/or more capital intensive funds to do business with a new generation of prime brokers that offer primarily clearing services. Regulation makes winners and losers; smaller prime brokers may wind up the winners as large bank regulation constricts our ability to serve clients.

Regulatory change in prime brokerage has emerged from the fog and is part of our daily reality. We at Societe Generale recognise the change and have adjusted our business model to focus on client-facing activities. However, I expect that evolution is not over: Leaving the prime brokerage industry with more uncertainties than certainties as balance sheet requirements continue to force change to business models.

James Treseler is Global Head Cross Asset Secured Financing at Societe Generale.