Increased competition in securities lending means that to maintain a leading program, US mutual fund managers should assess their policy choices, use of technology and routes to market. A combination of partnering with an agent lender and developing capabilities in-house can help managers meet their key objectives.

US mutual fund managers and their investors face complex challenges, including regulatory pressures, market volatility and price competition. Managers have rightly seen securities lending as a way to increase investor returns and defray operational costs. More supply in the securities lending market however does not always come with more demand for loans, especially considering that regulated mutual funds carry Risk Weighted Asset costs that may make their assets less attractive to borrowers than other types of lenders.

US fund managers may not control the external environment, but they have multiple decision levers to control their participation in securities lending. To generate their desired returns with strong risk management, US fund managers should revisit their policy decisions and agent lender relationships to produce ideal outcomes. Justin Aldridge, Head of Fidelity Agency Lending, notes that “In general, registered investment vehicles require more customized and tailored programs, and firms want the ability to control the lending parameters to protect their information while maximizing returns.” Partnering with an agent lender to create a customized program using sophisticated technology is a logical next step in securities lending program development.

Market acceptance and inventory growth

Investors worldwide have been increasing their engagement in securities lending programs in recent years. Globally, the amount of available securities lending inventory, or securities that a lender is willing to lend on any given day, has increased from US$22 trillion in June 2019 to over US$40 trillion in May 2022, an 82% rise, according to S&P Global Markets (see Exhibit 1). Meanwhile, the total pool of securities lending revenue has stayed between $10 and $11 billion, suggesting that the same amount of income is being divided between more asset owners.

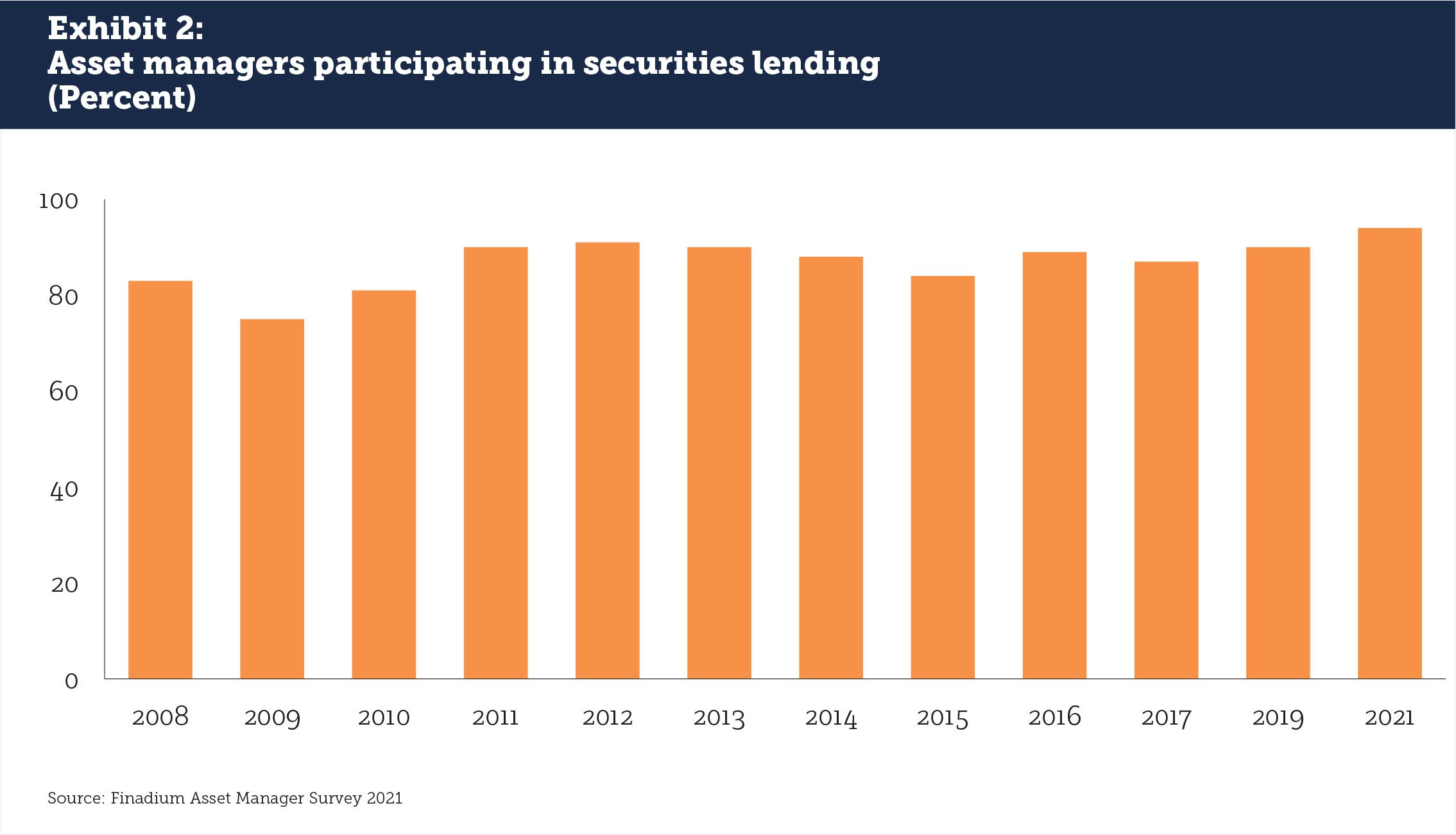

Large asset managers in North America and Europe have been part of this growth trend. A November 2021 survey from Finadium found that engagement in securities lending at large asset managers was 94%, an all-time high since data collection began in 2008 (see Exhibit 2). US mutual fund filings show that the average US fund earned 2.2 basis points from securities lending in 2021, although there is a wide variation between funds that earn under one basis point and those that earn five or more (see Exhibit 3). Broadly speaking, securities lending is widely accepted by large asset managers as a means of producing positive risk-adjusted income.

Cash and non-cash collateral, and the pricing of securities loans

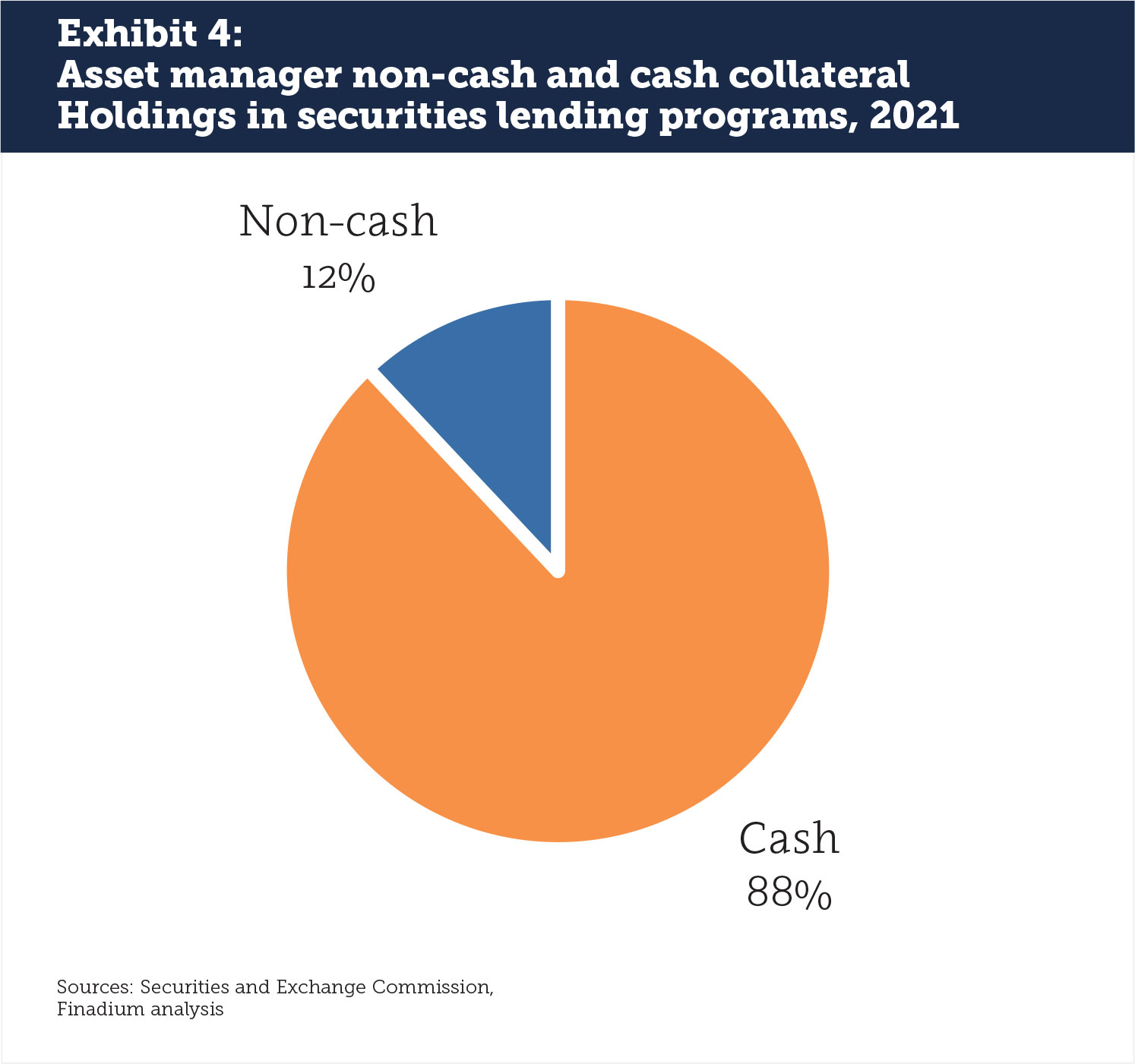

The US fund market has found some limited value in accepting non-cash collateral in the form of US Treasuries, which are currently permitted under SEC Rule 15c3-3 regulations. According to SEC filings, 25% of nearly 3,800 individual funds analyzed held some non-cash collateral in 2021. The total amount of non-cash held was 12%, compared to 88% in cash at the end of each fund’s reporting period (see Exhibit 4). SEC Rule 15c3-3 is directed at broker-dealers, who must provide securities lending collateral that is either cash, US Treasuries or a letter of credit. Discussions have been ongoing about including equities in the 15c3-3 definition, but this is not yet a collateral type that brokers can offer or US funds can consider for acceptance.

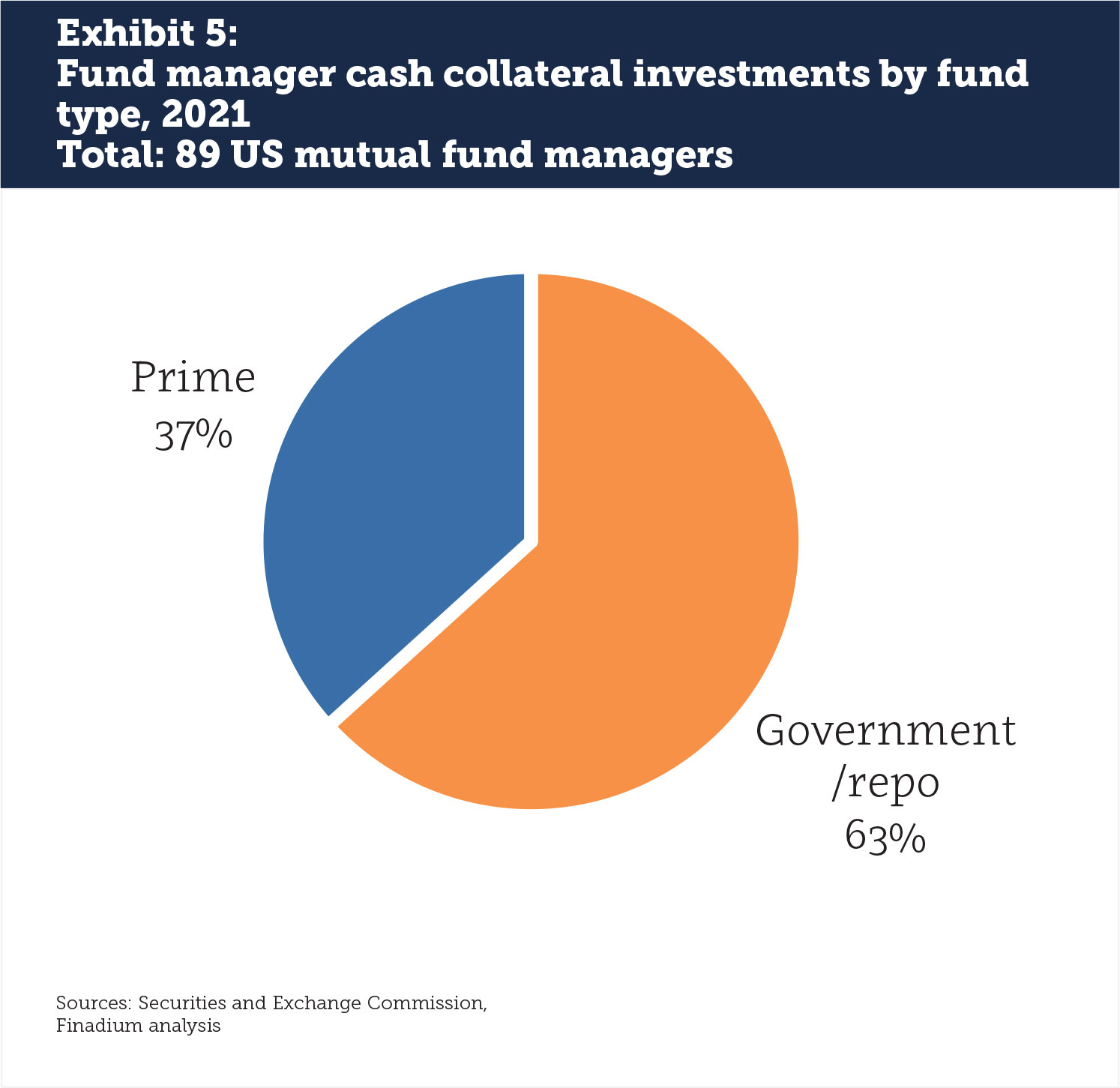

SEC data show that 63% of US fund managers have selected repo or a government money market fund as their cash collateral vehicle while 37% have chosen a prime or similar fund (see Exhibit 5). In practice, even these prime funds are very similar to repo or government funds; the main difference is often a small percentage of commercial paper or longer tenor of investment in the mix.

SEC data show that 63% of US fund managers have selected repo or a government money market fund as their cash collateral vehicle while 37% have chosen a prime or similar fund (see Exhibit 5). In practice, even these prime funds are very similar to repo or government funds; the main difference is often a small percentage of commercial paper or longer tenor of investment in the mix.

Fund decisions on the acceptance of non-cash and cash collateral may influence borrower decisions in an indirect manner. While US Treasury acceptance is not resulting in significantly higher returns for lenders than cash collateral today, maintaining flexibility for the future is important. Funds that choose overnight repo or government cash collateral reinvestment portfolios keep their risk to a minimum but this may also limit their ability to participate in some lending activity.

Differentiation through minimum spreads, proxy voting and QDI

Educated decisions on program parameters including minimum spreads, proxy voting and Qualified Dividend Income (QDI) can assist in delivering high quality outcomes to lending clients, but overly specific restrictions may have negative consequences. Fund managers should be able to rely on their agents to help them optimize the policies and objective of their funds while maintaining a competitive position in the lending market.

US funds can decide what a minimum spread should be and whether a fund should strive to lend all assets to generate cash returns or focus on intrinsic-only programs that generate income regardless of cash collateral reinvestments. Finadium’s experience as consultants is that minimum spread policies work best when set high or not at all. A program that lends only when a spread is 100 basis points or more knows that it is focused on hard to borrows. On the other hand, programs with a minimum spread of 10 basis points may have less clear distinctions on attractive versus unattractive loans one day to the next. In this case, no minimum or a prevention of negative spreads as a baseline could be the better policy choice.

The ability to make proactive decisions on proxy voting recalls versus lost income is a fiduciary management obligation, both to be a responsible investor and also to generate the greatest amount of income for investors. Many funds are now reevaluating their proxy voting activities in light of Environmental, Social and Governance (ESG) strategies, which may include recalling shares over proxy dates in order to vote. Doug Brown, Head of Business Development for Agency Lending at Fidelity says that “We get many inquiries about meeting the requirements of ESG and sustainable investing. It is important for funds to evaluate how much potential income could be generated if they continue to lend the securities or assess the revenue they would forgo if they decide to participate in an important shareholder vote. It is also necessary to determine the difficulty to get shares returned off loan, and the time frames required to recall securities from different borrowers before lending a security. All of this is a technology-driven process.” The pressure on US funds to be proactive around voting is only set to increase with the introduction of the SEC’s Form NP-X, which proposes to mandate that US funds report when they vote securities and if shares were on loan over proxy voting dates.

While a few fund managers have made a practice of frequent QDI analysis, Finadium’s experience is that most complexes have not thought much about this matter and that not many agent lenders have formal tools for evaluation. Funds with modest securities lending activities will likely never run into QDI limits, while firms with more active programs that lend over dividend dates often check their revenue opportunities relative to QDI. Funds that can evaluate QDI in an active lending program stand to deliver the most value to their clients in both the short and long term. Similar to recalls over proxy voting dates, a decision to recall for QDI may make the most financial sense for investors but may also make a fund less attractive for borrowers, which may impact future revenues.

Finding the right balance in minimum spreads, proxy votes and QDI is an important lever in securities lending for US funds. Borrowers that see more conservative policies may over time elect not to borrow from lenders that recall on a regular basis, or overly narrow parameters may impact a fund’s position in the lending queue, resulting in fewer overall opportunities for revenue generation. Finding the right balance, starting with internal policy making and extending to partnering with an agent lender, is a necessary step.

Optimizing operations and technology

US funds have not historically gotten involved in the operations or technology of securities lending, but as the windows for settlements, regulatory requirements, and other client needs shorten, this is an area where clients should spend more time with their agent lender or when evaluating a new provider. Better technology from agents is helping clients see the value of their portfolios in real time and the impact their decisions have on returns. Market data delivered on screen can translate into immediate messaging to agents to customize program parameters. This reduces the need for extensive coordination and speeds up response times.

Agent lenders that can capture inventory details on an automated basis from custodial systems can deliver better results for clients, and agents that can support Straight-through Processing with borrower systems are less likely to have fails. In a market moving to T+1 settlement, these types of operational efficiencies can help increase the attractiveness of different fund assets for borrowers. Borrowers have options to choose from different lenders, and their ability to engage with the least friction can make a difference to the bottom line.

US funds will soon need to consider the potential impact of the SEC’s proposed securities lending transparency rule, Rule 10c-1. The rule allows agent lenders that are either broker-dealers or not to report on behalf of their clients, but requirements for inventory reporting may come as an unwelcome surprise. Actively managed funds may not be comfortable in reporting all their available assets for lending and may want to make adjustments to lending parameters in order to both keep their inventory open and to limit what the public may see on a daily basis. This creates the need for flexible, two-way agent lender communications where available inventory on a security basis may be set dynamically, or program parameters changed on short notice, to meet both the spirit and the letter of the law.

Matching fund objectives with agent lender capabilities

The US mutual fund market is well served by agent lenders with both generalist and specialist capabilities. As fund managers evaluate these service providers, a primary objective should be identifying a firm that can help differentiate fund assets to borrowers in a crowded environment. Fidelity’s Aldridge says that “a good time to assess the market is when there are significant changes to your firm’s assets, major changes to the agency lending provider landscape, and underperforming assets in relation to benchmarks or a steady decline in revenue and balances.”

While some managers continue to look at fee splits as a primary decision factor, we hold that this should be a secondary consideration. Rather, managers should look for agency lending teams that share similar goals and have the ability to deliver on the most important priorities, with technology and operations playing a central role in the process. A strong partnership combined with a review of internal policies creates the most likely opportunities for revenue gains for the benefit of fund investors.

This article was commissioned by Fidelity Agency Lending®, a division of Fidelity Capital Markets. For more information about Fidelity Agency Lending, please visit https://capitalmarkets.fidelity.com/fidelity-agency-lending.

Fidelity Capital Markets is a division of National Financial Services LLC, a member of NYSE, SIPC.

Finadium is an independent entity and is not affiliated with Fidelity Investments.