As the funding profile of European banks continues to mature, MTS finds that a diversity of product types across secured and unsecured are still necessary and in use. There is a common theme however: the need for efficient trading and post-trade solutions that harmonize with broader bank objectives on automation and big data management. A guest post from MTS Markets.

While secured funding, notably repo, gets the most attention, the market continues to rely on deposits for much of its funding needs. This creates ongoing demands for a mix of manual operations and automated solutions to ensure delivery and settlement of multiple transaction types. Banks may also be using multiple trading platforms to interact with each other, as well as with buy-side clients.

There is a need for change in this space, as relying on both manual and automated activities is burdensome and may lead to operational error. Trading platform operator MTS offers both secured and unsecured transactions with full settlement connectivity across the product lineup, including to TARGET2 and T2S. This extends to offering access to a diversity of liquidity types and sources. Banks tell us that they are looking to bring the full range of funding activity onto technology systems and move away from manual processing. This creates alignment with the interests of banks to drive automation further through the organization.

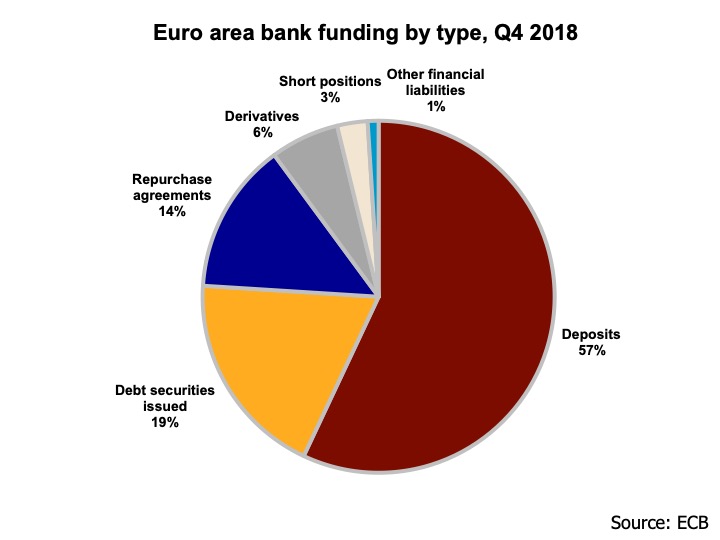

The funding mix across European banks

The funding profile of European banks remains diverse, with Treasury and repo desks utilizing both secured and unsecured vehicles to meet their funding needs. Most notably, unsecured deposits are the single largest type of funding product, according to 2018 supervisory data from the European Central Bank (ECB) (see Exhibit 1). This may be an unexpected result for market professionals looking at the steep growth of the repo markets, but the importance of unsecured cannot be minimized.

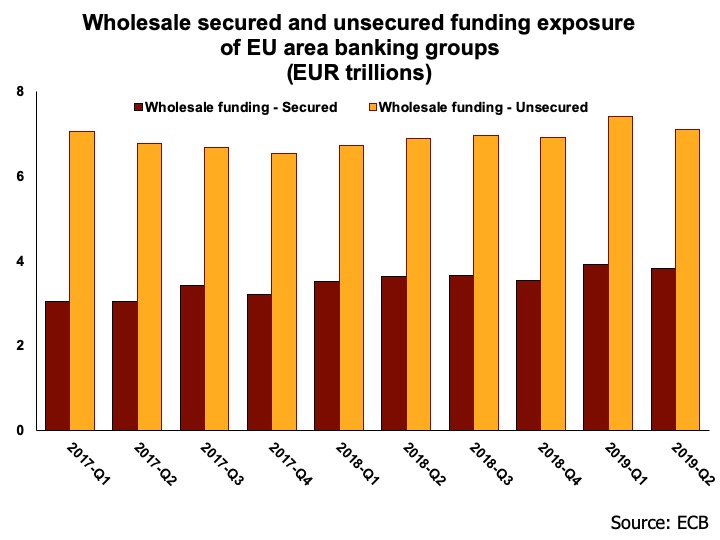

Most of the focus in recent years has been on the secured market, and indeed, from Q1 2017 to Q2 2019, secured funding exposure at Euro-area banks increased by 26% to €3.8 trillion. This is still 54% smaller than the unsecured Euro bank deposit market however, where volumes have remained about constant at €7 trillion for the last three years, including transactions with both other banks and central banks (see Exhibit 2). While the unsecured market may not be seen as enticing, it remains the main way that Euro area banks obtain funding.

The unsecured market may be poised to regain more of its lost luster for regulatory reasons. A recent Bundesbank article looked at the long-term decline of unsecured funding and noted that policy changes could encourage a revival with a market-based approach: “…it would be desirable in the medium term to strengthen market mechanisms in the refinancing of banks and to contain the role of monetary policy operations in the compliance by banks with regulatory standards.” This may not be immediately possible in the midst of a global slowdown, but it does appear to be the ultimate goal.

The use of unsecured deposits for calculation of the ECB’s Euro Short-Term Rate (€STR) may also encourage new interest. The ECB has noted that “Unsecured deposits are standardised and are the most frequent means of conducting arm’s length transactions on the basis of a competitive procedure, thereby limiting idiosyncratic factors potentially influencing the volatility of the rate.” The official adoption of €STR may give greater comfort to institutions that were previously uncertain about their preference of funding methods.

While this is the goal, a move towards unsecured solely because of €STR is not yet happening, at least in the distribution of unsecured loans between banks across jurisdictions. In a November 2019 speech, then-Member of the Executive Board Benoit Coeuré noted that Euro-area banks largely conducted unsecured transactions with entities that had no access to the ECB’s liquidity programs. The secured market on the other hand was more effective in mitigating borrowing costs between countries.

Further, unsecured deposit trading is not captured by Securities Financing Transactions Regulation (SFTR), whereas repo is an integral part of the reporting regime. For institutions that look to reduce or avoid their SFTR exposure, a greater reliance on unsecured is one way to achieve that goal. This may wind up mattering more to money market funds than banks, but time will tell.

Automation and settlement, cross-product on one platform

The fact that bank funding remains an exercise in trading across multiple products means that banks must also find trading and post-trade solutions that can consolidate both information flows and operational requirements. For the bank, these two processing streams potentially mean two separate operations teams, data integration efforts and opportunities for fails that must be reconciled with diverse organizations. In today’s environment of automation, this is not only impractical; it is also an obvious inefficiency across the bank’s target operating model.

At MTS, we are working to consolidate the two processing streams of secured and unsecured on to a single regulated multi-product trading platform. We already offer one repo trading platform for both interdealer and D2C business; including unsecured is another step towards the overall goal of better visibility, transparency and operational efficiency.

A key methodology for executing on this strategy is automated submission of messaging to TARGET2. The TARGET2 platform run by the Eurosystem provides real-time gross settlement (RTGS) with orders submitted in Euro and settled in central bank money. The system can handle both bank to bank and bank to central bank unsecured trades with over 1,000 counterparties. MTS automatically processes and sends unsecured deposit transaction settlement instructions to TARGET2, letting banks move on to other pressing matters including liquidity and risk management.

On MTS, different money market transaction types can be traded, settled automatically and then reported in the same trade blotter, now. For example, a repo trade could be forwarded to a CCP and a bilateral deposit to TARGET2. This enables the bank to execute all of its funding activity in one place.

Unsecured deposits are the final piece in the process of aggregating funding products for cross-product settlement. While repo growth is the shiny coin, unsecured deposits remain an important bedrock of how banks fund themselves. Integrating STP across both product types provides an important leap forward for the industry.

About the Author

Tim Martins is Head of Product for Repo and Money Markets, MTS. Tim has over 20 years’ experience in repo, including 11 years on the trading desk at Bank of America. During his five years at MTS, Tim has overseen the development and launch of BondVision Repo, a new dealer to client repo trading venue.

Tim Martins is Head of Product for Repo and Money Markets, MTS. Tim has over 20 years’ experience in repo, including 11 years on the trading desk at Bank of America. During his five years at MTS, Tim has overseen the development and launch of BondVision Repo, a new dealer to client repo trading venue.