In the last two posts on Single Treasury Futures (STFs), we reviewed the structure of the instrument as well as who might use them. In this post we will look at how STFs might differ from cash and repo positions from a balance sheet, capital, and margin perspective, and what that means for client demand. This is really the hook for any central counterparty (CCP) cleared secured funding alternative; let’s see what STFs have to offer.

Because futures contracts don’t involve booking an asset or a liability, their impact on the balance sheet is limited to their fair market value. As a result, the amount of capital allocated to a futures contract can be small. As an added benefit, US regulators recently clarified an important part of the Leverage Ratio: clearing activity must be single counted as a liability, not double counted (once for the client, second time for the clearing firm). In contrast, the full notional values of repos and cash positions are on the balance sheet, absorbing capital. Making an apples to apples comparison based on abstract data is difficult, but the consensus opinion is that a CCP-based transaction should beat a bilateral transaction in terms of balance sheet impact, especially once other factors like Dodd-Frank 165 are taken into account.

The Bank for International Settlements has announced that netting will be allowed for repo books when calculating balance sheet usage (and hence capital). Without that relief, the case for STF as a tool to help manage the balance sheet would have been overwhelming. With it, the case is still pretty good, since FIN 41 netting cannot always be achieved (and some observers believe that the netting rules will still drive repos to CCPs as the only, or best, safe solution). For Globally Significant Financial Institutions (G-SIFIs), subject to Supplemental Leverage Ratio rules, the sensitivity to reflecting risk on the balance sheet is even greater. STF can be an important optimization tool.

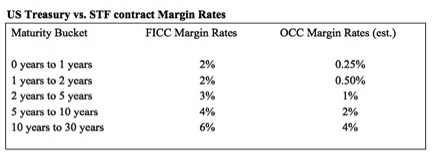

On paper, margin rules favor STFs over the main CCP repo alternative, the DTCC’s FICC. Repos that clear through FICC margin rates are about 2% for shorter dated Treasury securities and rise to 6% for long dated Treasury securities, although market participants believe that in practice, FICC margin rates may be lower than they appear in the rules. While actual haircuts and margin will vary, OCC CUSIP by CUSIP margin should provide capital efficiencies. The chart below shows compares FICC published margin rates to OCC margin rates.

Source: NASDAQ OMX

Turning to the client side, we expect that the demand for financing will always be part of market activity, at least for the foreseeable future. Clients tend to seek out the lowest cost financing among their various options and will likely be agnostic as to how their positions get financed. Dealers strive to make as many individual trades profitable as possible and not rely on commissions elsewhere to make up losses in repo. We think that this combination of factors leads the market toward Single Treasury Futures. Lower margin costs on a CCP plus lower margin charges on OCC than FICC mean lower costs for clients. Are Single Treasury Futures inevitable? No, they may not be for everyone, and dealers are still working out their options. On paper however they look to strike a good balance between dealer capital charge needs and what clients will want to pay for their transactions going forward.

This article was sponsored by NASDAQ OMX.

3 Comments. Leave new

Any ETA on when this product will be listed? And where will it be listed?

The current expectation is H1 2015.

This is definitely one for the ‘sooner rather than later’ file. Banks are not going to waste scarce capital on Treasury repos.