The idea of starting to trade on a new platform, especially for repo, can seem daunting to the buy-side. In this article, I present the opportunities and challenges for onboarding and trading with non-traditional clients. This is especially relevant for credit departments concerned about new counterparties.

In two previous articles, I pointed out that the drivers behind the shift away from high volume, low margin businesses, like repo, at major money center banks is due in part to the restrictive supplemental leverage ratio. I went on to describe ways in which many buy-side clients have been relegated to lower status in the repo market: they don’t have platinum accounts; have no transactions that are nettable; and are not members of CCPs. These firms are ideally placed to access the market through better collateral and liquidity management, expanded credit appetite, and using All to All (A2A) electronic lending platforms to mitigate the lack of credit intermediation available to them.

The case for A2A lending and utilizing collateral exchanges to meet regulatory requirements (MiFID II and SFTR, to name just two) and to adhere to new margin requirements for derivatives has been made time and again. Some clients are asked by their regulator: what happens if your bank “goes away?” Having alternative access to the repo market, given the low barrier to entry, grants the non-traditional repo client and their counterpart the ability to mobilize their collateral and invest cash at market prices. Still, it has been problematic for firms to engage in alternatives. What’s causing the problem and how can it be resolved?

Onboarding from the client perspective

A prospective buy-side client conversation starts with understanding the current funding needs of the firm: whether they fund bilaterally, through triparty or using a cleared model, and how they clear swaps to gauge their need for cash to pay VM. The conversation then turns to money: what are they paying to access the market and what is the return on their cash? Their level of sophistication with regards to their collateral management and margin optimization usually follows along with understanding how they monitor their own positions, including collateral and cash movements. These questions are usually well understood by buy-side firms.

Where clients trade on the collateral or cash curve with regard to tenors is important. There is a subset of clients who prefer or are mandated to trade certain maturities to access or secure funding. Another client base looks for long term funding because it may be required or they may deem it prudent to lock up funding for a longer term; for example, pension funds in liability-driven investment (LDI) strategies. On the other hand, money funds and CCPs often need to stay inside of one week when investing cash. Many clients that are required to post cash against margin calls when trading swaps almost always satisfy that need with short term funding.

If there is a match between the needs of the client and the ability of the funding platform to provide best price, best execution, and transparency, then the onboarding process, such as that proffered by Elixium, begins. There is always a point person assigned to manage documentation, any technology issues that need sorting, the legal documentation process, and the coordination of user testing. Once clients have accepted each other as potential counterparties, and the concomitant Know Your Client (KYC) and Anti-Money Laundering (AML) processes have concluded, then the assigning of credit lines and risk parameters, and signing Master Repo Agreements (MRAs) are the next steps.

At Elixium, we have created an All to All MRA stripped of the one-sided language usually buried in a bank’s standard initial documentation, which saves time and money. Once signed, it gives the counterparty the right, but not the obligation, to trade with everyone who is a signatory to the document. Assigning credit lines, risk parameters and haircut schedules not only ensures counterparty acceptability when transacting on the platform, but streamlines the post trade flow.

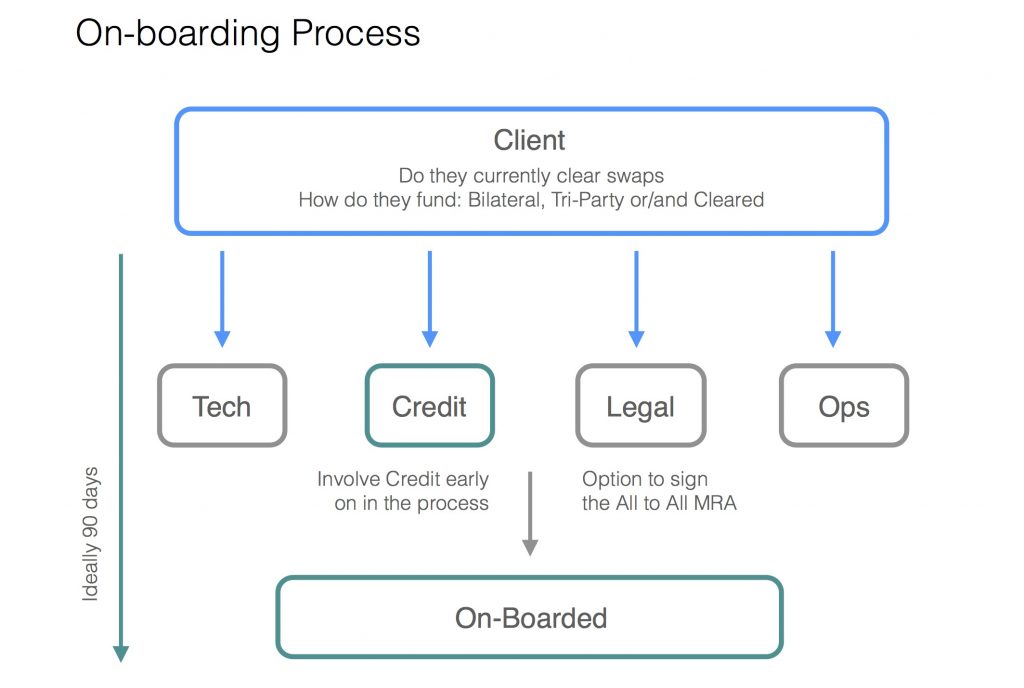

The success rate of onboarding is high if completed under 90 days (see Exhibit 1). If this process is longer than 90 days, then the odds of the firm becoming a participating member of the platform begin to go down. Getting commitment from a client on a senior level after having explained the value proposition of being a price maker instead of a price taker is paramount.

Exhibit 1:

The All to All onboarding process

Source: Elixium

The credit department challenge

In getting started on an All to All repo platform, technology and operations are easy to adapt but credit can be more challenging. Obtaining credit sign-off is typically the most difficult part of the onboarding process and one point at which the process can fail. In both our own feedback and comments at public conferences, business managers are asking, “how can I convince my credit department that All to All is a good choice?” Our experience shows several routes to success, and we recommend pursuing several of them at once:

- A senior credit officer (SRO) should be involved in the process as early as possible, even as early as the first meeting. The senior credit officer is responsible for setting credit lines and understanding where credit risks lie in the system.

- Establishing a meeting of the minds between the senior credit officer, the business, and the legal counsel reviewing the MRA is essential to spelling out what risks the buy-side firm could face.

- Credit officers may or may not have much exposure to repo, to MRAs, or to collateralized transactions outside of derivatives. We recommend an education session for credit departments to understand how the market works.

Ensuring credit department buy-in has been the biggest hurdle to date in creating successful buy-side All to All engagement. We emphasize the control aspect of the A2A market: counterparties can be switched on and off quickly, and credit lines can be added or reduced in real time. Credit departments will need to be engaged and interested in the opportunity, as well as cognizant of the requirements of the MRA, for the market to successfully supplement the declining supply of bank liquidity with a diverse set of counterparties able to provide best price and transparency.

Onboarding from the platform perspective

The fracturing of pricing in the repo market is fairly well known and cannot be solely attributed to banks widening spreads. Price discovery and the supply and demand imbalance driven by repo market participants, as well as the available supply of balance sheet, are major contributors to this fracturing. Banks have done a very good job of selling their need to meet return hurdles on repo transactions to their clients. Their explanations are justified in many respects: they do indeed face balance sheet hurdles that must be met.

Other contributors to repo dysfunctionality include definitions of operating versus non-operating deposits, money market reform, excess reserves, and rules around CCPs depositing cash in accounts at Central Banks. Liquidity ratios have also led to a major imbalance in the market: cash providers want to stay short term (one week or less) while banks are looking for longer term funding to meet LCR and NSFR rules. These factors have combined to cause massive, even tectonic, shifts in the deposit base of banks and their clients.

Even though the market clearly is not functioning well, there are a number of headwinds when trying to gain client approval to engage in A2A lending. These include: launching with critical mass; gathering both collateral and liquidity providers in equal measure with overlapping tenor points, trying to avoid a dearth of one and an oversupply of the other; and managing restrictive covenants inside an institution’s charter. There is also the inertia problem: if supply lines aren’t truly and fully broken, then some institutions are happy doing the same thing even when they know it isn’t entirely in their best interests.

Solving the onboarding challenge

Cracking the code of industrializing the onboarding process will be one of the characteristics of successful All to All repo platforms. There is a clear need in the market for fair pricing, liquidity, and transparency to both meet regulatory objectives and to provide best services for investor clients. This is not a problem for the future, but rather an immediate need that is reflected in asset manager investments today.

Efficient and rapid client onboarding is the number one priority once a client has expressed interest and a demo has been concluded. This one time only, 90-day time commitment pays enormous dividends once completed. By focusing on the credit department as the main group that requires education and support, and by engaging with them early, we at Elixium aim to speed this process along to build critical mass.

Stephen Malekian is Head of Business Development – US for Elixium.

He has over 35 years of experience in the global financing markets, having run Global Fixed Income Finance and Prime Services at Citi and European and Asian Fixed Income Finance at Barclays. Steve has been Chairman of SIFMA’s Executive Committee of their Funding Division, member of the New York Federal Reserve Task Force on Triparty Reform, as well as a member of the European Repo Council and the LCH Risk Committee.

Steven Griffiths contributed to this article.