The obstacle of regulatory balance sheet restrictions in physical securities finance is prohibiting the normal flow of business. While there is a natural alternative in synthetic financing markets, firms must support a robust identification of global inventory availability in order to grow a cost-efficient business.

Synthetic financing has been an important topic in global financial markets for the last five years as regulations have spurred the growth of this business over physical financing. Synthetic business is not new, and synthetic prime brokers have long made inroads with hedge funds based on swaps agreements that require only an ISDA agreement. But even swaps businesses have their balance sheet limitations, and advanced market participants are finding that inventory management is a key factor in the ability to grow business activity and hence revenues.

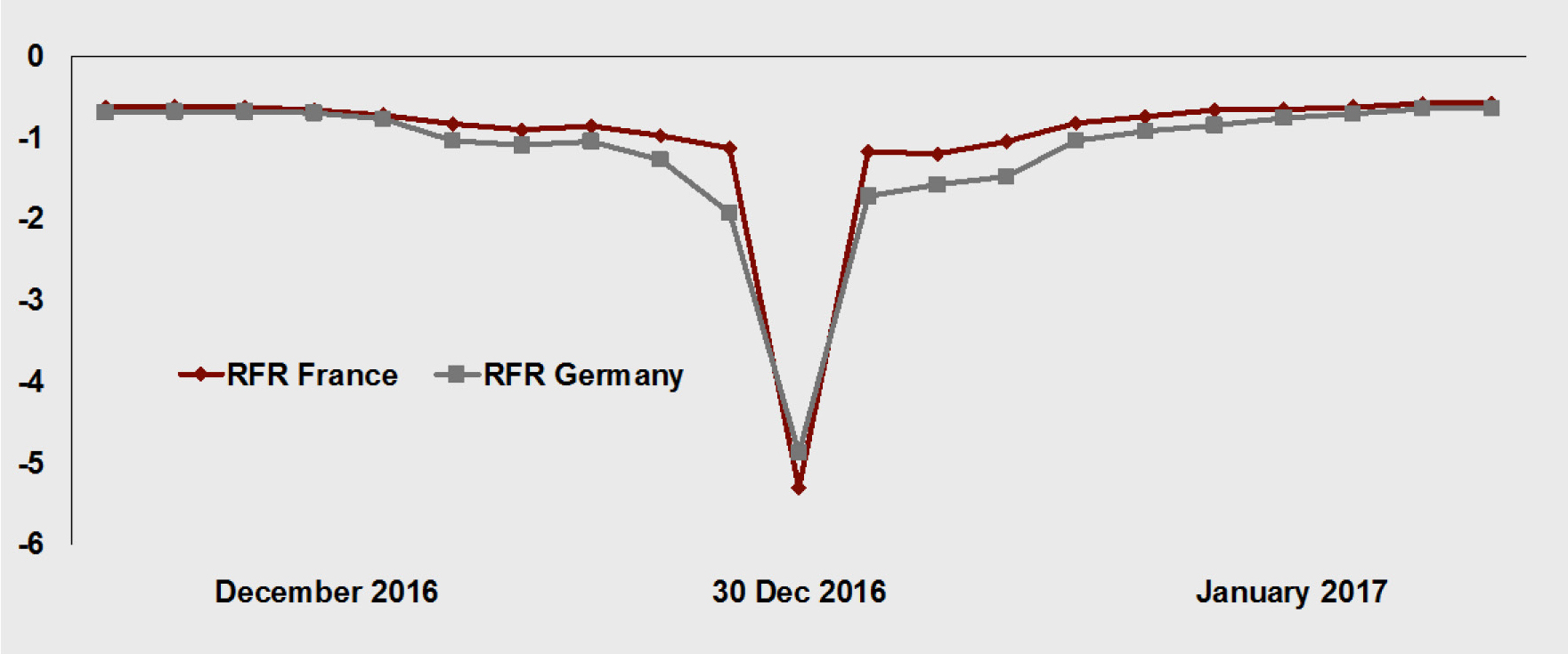

On the physical side, there has been little progress in global securities finance to relax regulatory constrictions and release liquidity into the markets. According to the latest ICMA European repo market survey, the European market has been trending sideways, with growth across the same group of banks at just 0.8% from December 2015 to December 2016. Meanwhile, European repo markets are unable to satisfy existing demand, especially at critical times like quarter and year ends; repo index data show the dramatic fall in General Collateral French and German bonds at the end of 2016 (Exhibit 1).

Exhibit 1:

France and Germany RepoFunds Rate

(Percent)

Source: RepoFunds Rate

Meanwhile, in the US, spreads between US Treasury overnight repo indices show widely fluctuating markets for dealers on the DTCC’s GCF market. At the end of Q3 2016, rates leapt from 50 bps on September 23 to 127 bps seven days later. Dislocation at year end was subdued, but the pattern began to reemerge again at the end of Q1 2017 with a 23 bps rise during the last week of the quarter. The physical markets have shown the stress of regulatory-driven compression.

While Bank for International Settlements data show the swaps market shrinking over the last year, this figure hides the impact of trade compression and netting on dealer balance sheets. In fact, a loss of netting would gross up the balance sheet of most major banks by hundreds of percent, and this is not being taken lightly. Synthetic financing by any account remains big business.

An opportunity in derivatives, if done correctly

At Murex, we see the restriction in physical financing activities as opening a new door in the synthetic markets, but there are caveats. Dealers have turned to derivatives in order to meet client financing requirements, which come with lower regulatory cost and the opportunity to earn servicing fees unassociated with the physical financing markets. But there is much more to the business than simply installing a synthetic finance trading system.

The basis on which dealers can expand into derivatives relies on a robust knowledge of their global inventory: this is the critical step to managing any sort of broad derivatives portfolio, and swaps financing opportunities are no different. Under current regulations, listed, centrally cleared derivatives trades are inexpensive relative to bilateral trades, and OTC derivatives are often less expensive than a securities financing trade depending on the dealer’s regulatory structure and capital requirements. We are now seeing specific cases where buy-side firms are getting better pricing from total return swaps, especially for General Collateral loans in exchange for cash or government bond collateral, than from conducting the same trade as a securities loan.

While not beneficial for the underlying market, the reality is that the swaps business, as any synthetic prime broker will tell you, is cost-efficient. It carries a low operational burden for custody and settlement, wide access to markets and jurisdictions, and can be set up under an ISDA umbrella. General collateral swaps contracts can typically be centrally cleared, which lower the cost further, and portfolio swaps allow for substitutions during the contract without having to create a new contract altogether.

The more that inventory is understood and can be hedged against in a derivatives trade, the more that trade will net for the purpose of dealer capital ratio calculations. Nettable trades are the best option as dealers have a specific and direct incentive to net off eligible sets of transactions to lower capital impacts. While netting a derivatives trade against a physical position is good, netting off two derivatives trades, particularly within the same Exposure at Default group, is an ideal scenario.

The infrastructure requirement: inventory + optimisation

The next step for dealers in building out their derivatives businesses is to create the infrastructure necessary to identify global inventory holdings. The challenge in inventory is to optimise balance sheet utilisation for a full range of assets. For example, knowing that a long position in Hong Kong can be offset by a total return swap on the same asset in London is not just a luxury, it can make a significant difference in the balance sheet cost of the transaction. As another example for the Standardised Approach to measuring counterparty credit risk, netting Exposure at Default for eligible netting sets works best if a dealer has a full view of all transactions that fall into the netting set.

Inventory management is not just helpful for synthetics, but also facilitates collateral optimisation for all collateralised trading activities. As Initial and Variation Margin requirements are now live, firms that have done the hard work of centralising their inventory management have a substantial advantage over firms that have yet to engage in this effort.

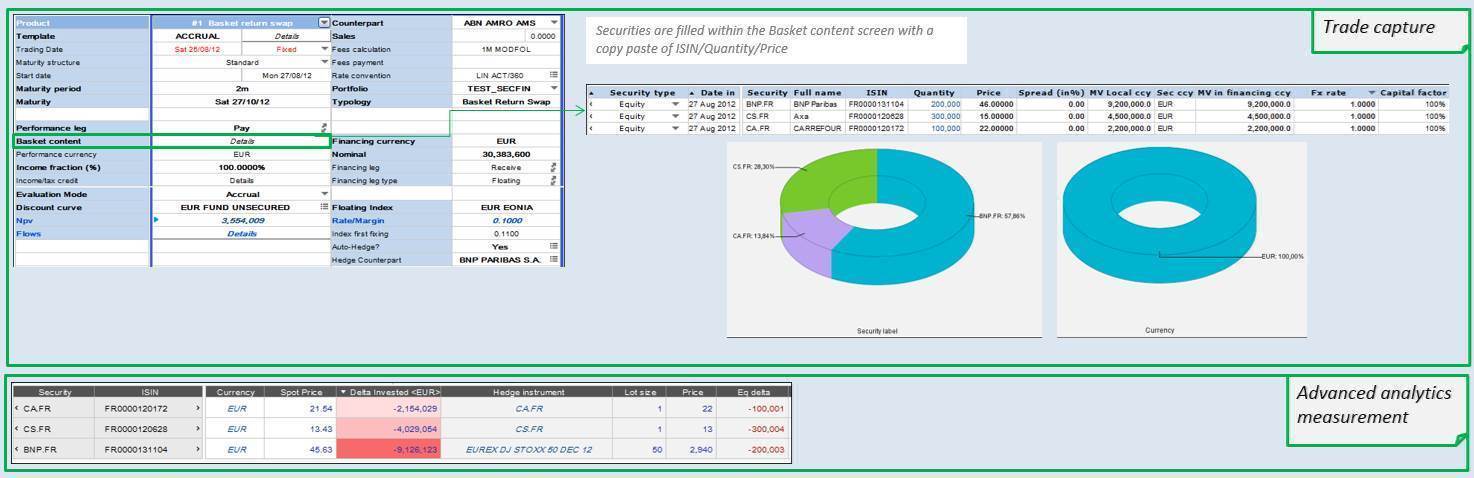

Robust analytics are also part of the requirement for building a better derivatives business. Murex has released a new version of its portfolio swap module to encompass a wider range of basket and index business activities: the Murex solution provides advanced analytics measurement and dynamic hedging capabilities for a wide range of risk factors. Credit risk capabilities, to measure capital costs involved, are also a key element, and offered as standard with Murex’s MX.3 solution (see Exhibit 2).

Exhibit 2

MX.3 for Synthetic Finance – Portfolio Swaps Analytics

Source: Murex

Blockchain + inventory + derivatives?

Blockchain represents an interesting possibility when assessing inventory management and the growth of derivatives businesses. A global internal (closed) blockchain at a firm can be the repository for all inventory holdings and feed downstream systems around the world. Along with blockchain comes the golden copy of inventory holdings, which means that each downstream system can verify its ability to net off positions for lower capital costs and then feed back when positions have been tagged for this purpose. The single internal blockchain can then inform all other downstream systems that the asset is no longer available for hedging purposes, which in turn impacts the cost of the next trade.

While optimistic, this situation is not futuristic: it is achievable based on existing technology. The biggest challenge is ensuring the right inputs and outputs are connected to the blockchain itself. But with robust data coming in, the blockchain can distribute accurate data outwards. This is the transition point that makes inventory management not just ideal but fundamentally cost effective.

Inventory management is the key factor for enabling the growth of derivatives businesses that supplant physical financing. Synthetic business is on the rise, but must be supported by an inventory management system coupled with derivatives functionality to be truly effective. Blockchain represents one model to executive inventory management so long as there is robust connectivity to upstream and downstream systems.

Etienne Ravex is Head of Product Management for Operations at Murex. Beginning his career in banking operations, he has since focused on developing risk and collateral management technology solutions at Murex. Etienne recently oversaw the overhaul of Murex’s collateral management solution. This important change was a response to new regulatory requirements and operational challenges facing the industry. Working with a diverse, global client base, covering both buy-and sell-side firms, Etienne has gained in-depth experience and knowledge of regulatory change, and collateral transformation and optimisation challenges. This experience equipped Etienne for his newly acquired position. He now oversees product decisions in the operations domain. The core components of operations at Murex include transaction life cycle, position management, margining, and settlement life cycle.

Etienne Ravex is Head of Product Management for Operations at Murex. Beginning his career in banking operations, he has since focused on developing risk and collateral management technology solutions at Murex. Etienne recently oversaw the overhaul of Murex’s collateral management solution. This important change was a response to new regulatory requirements and operational challenges facing the industry. Working with a diverse, global client base, covering both buy-and sell-side firms, Etienne has gained in-depth experience and knowledge of regulatory change, and collateral transformation and optimisation challenges. This experience equipped Etienne for his newly acquired position. He now oversees product decisions in the operations domain. The core components of operations at Murex include transaction life cycle, position management, margining, and settlement life cycle.