We are staring it down year end and the Fed is gearing for a long-awaited rate hike. Typically, Fed interest rate moves are an Event with a capital “E”. Securities finance had always been tremendously plugged in and sensitive to Fed moves as arguably the most rate conscious and rate sensitive of businesses – after all, no other industry refers to interest rates as “prices”. Not this time though. What is happening here?

The securities finance markets appear pretty disinterested in the impending Fed rate hike. A quick search on the subject across the internet yields a surprisingly low number of hits – even in the professional press. Indeed, the fact that we are so uninterested simply reinforces and confirms just how the factors that drive our business have completely shifted in the last 10 years.

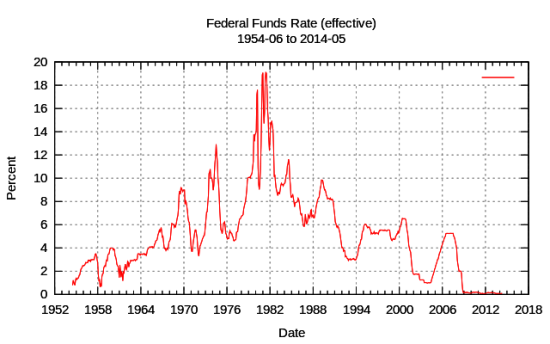

Everyone is very familiar with charts that look like this –

The most obvious and notable anomaly in this chart is the incredible duration of the flatline since 2009. There has been no period of even 1 year (much less 6) in the past 60 years when rates – high, low or in-between – were fixed and basically constant. Stated another way, for 10 percent of the period, rates have been so near to zero as to be essentially irrelevant – or, for 20 percent of the working lifetime of an old stock loan guy.

According to traditional economic theory, rates this low should mean that the economy is awash in gigantic inflationary piles of cash. We should see people backing up to the grocery store with dump trucks full of banknotes to buy their daily bread. We should see the US Dollar in free fall in currency markets, as governments and other foreign investors dump our devalued currency. Investors should be fleeing all dollar based investments for things like gold and silver in preparation for the collapse of the American economy.

Of course, none of this is happening. Dollar-based investments have increased in the period, and – apart from the initial panic spikes at the beginning of the Great Recession – safety net investments in “hard assets” have turned out to be big losers. If anything, the perception of the dollar as the currency of security has increased as has the attractiveness of foreign corporate investment in the US economy.

The reason we haven’t seen spiraling inflation and currency devaluation is that, while there is an extraordinary amount of incredibly cheap cash out there, much of it is out of play; its flow and movement are no longer controlled or regulated naturally by its market “price” in rate terms. Instead, the flow of cash is throttled by more stringent regulation on market risk, credit exposure and increased capital reserve requirements – all of which favor hoarding cash rather than using it. So while there is a theoretical surfeit of cash, there is an actual extreme lack of cash flow. The reserves are full, but it’s only coming out one reluctant and one regulatorily expensive drip at a time.

These factors have become far and away more important in capital markets, and particularly securities finance, than are central bank rates. Because of credit and balance sheet restrictions, we have moved away from a Big-Balance-Cash-Investment driven business to an arguably more pure form of fee-for-service (intrinsic value) driven business… which makes the loan fee far more influential than the cash rate of return.

Securities Finance Monitor premium subscribers will have seen an article last week about returns in securities lending, “An interesting twist in returns from cash and non-cash collateral in securities lending (Premium Content)“. This article included a chart on the relative market value of non-cash versus cash securities loans, based on data from SunGard’s Astec Analytics. In 2015 for the first time, more than 50% of global securities finance balances by market value are now collateralized by something other than cash – up from about 25% a mere 9 years ago.

Who would have thought 15 years ago, given the relative heft of the US (always heavily cash collateral) market, that the majority of securities lending would have no recourse to cash? In a very meaningful way, as an industry securities finance has separated itself from Fed rate policy. Fed rates are now interesting, but that may be just a distant indicator with little meaning on the ground. We’ll continue to yawn as long as the price of capital, credit and risk outweighs the price of money.