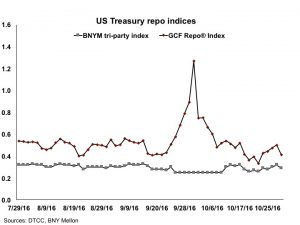

The Federal Reserve has asked for comments on their planned publication of three interest rates (along with the Office of Financial Research), including the Secured Overnight Financing Rate (SOFR) selected by the Alternative Reference Rates Committee as an ultimate replacement for LIBOR. The planned rates are based on General Collateral (GC) tri-party and GCF Repo(R) transactions. This raises some pointed questions for the future of bilateral non-cleared UST repo.

![]() This content requires a Finadium subscription. Articles with an unlocked symbol can be accessed with free registration. Log in or create a free account by signing up here..

This content requires a Finadium subscription. Articles with an unlocked symbol can be accessed with free registration. Log in or create a free account by signing up here..