The IMF released a chapter of their April 2015 Global Financial Stability Report “The Asset Management Industry and Financial Stability”. We read this with interest and dismay. On the one hand, the authors make valid points about risk transmission in the plain vanilla asset management industry, a number of which we have heard before. On the other hand, we thought this was crazy: at what point is no asset safe enough in the eyes of regulators for a regular investor? The chapter does not answer this question, and that’s a missing link.

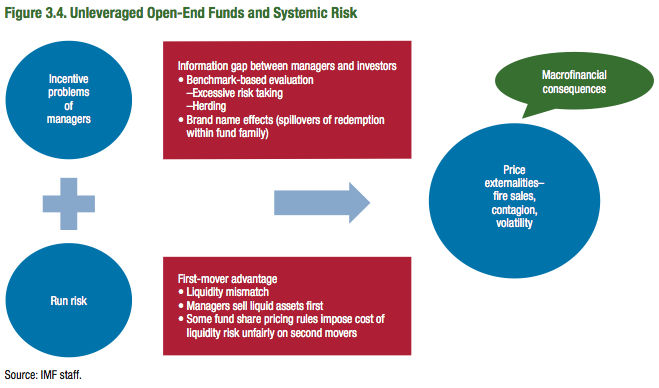

The basics of the chapter are that the IMF is worried about liquidity and systemic risk at plain vanilla asset management funds. There is lax regulation on liquidity (true) and herding by portfolio managers (also true). In other words, nobody really knows how much systemic risk there lies in plain vanilla funds when the fund managers themselves don’t know and portfolio managers all tend to run for the entrance or the exit at the same time. The concern is less about fund complexes than the behavior of types of funds, for example emerging market equity funds or corporate bonds funds. See figure 3.4 for more details on risk points.

As a result, the IMF would like regulators to substantially increase their attention on systemic risk management at plain vanilla investment funds. The IMF proposes three actions:

- Currently, most securities regulators focus on investor protection and do not intensively supervise risks of individual institutions with the help of risk indicators or stress tests. This practice needs to be changed, supported by global standards on microprudential supervision and more comprehensive data.

- Moreover, macroprudential oversight frameworks should be established to address financial stability risks stemming from the industry. These stability risks originate in price externalities that can be missed by microprudential regulators and asset managers.

- The roles and adequacy of existing risk management tools, including liquidity requirements, fees, and fund share pricing rules, should be reexamined, taking into account the industry’s role in systemic risk and the diversity of its products.

The IMF also notes that “the assets under management of top asset management companies (AMCs) are as large as those of the largest banks, and they show similar levels of concentration.” We found this trend in our December 2014 report but not to the degree that the IMF may think: “In 1995, the top five mutual fund complexes held 34% of assets; by 2013 that figure was 40%.” (Understanding the Modern Custodial Bank, Finadium December 2014).

We find nothing factually wrong in the IMF’s write-up besides some minor differences in interpretation and opinion. Yes, there are risks of fire sales in plain vanilla asset managers, and regulators have no real handle on what liquidity or systemic risks are out there. The ETF industry, discussed both in the IMF chapter and by us last week (“ETF liquidity: will it be illusory in volatile markets?,” April 7, 2015), is a good case study.

Here’s our big concern: we can agree on all these risks, and we can agree with the Financial Stability Board and IOSCO recommendations on defining some asset managers as SIFIs (“Assessment Methodologies for Identifying Non-Bank Non-Insurer Global Systemically Important Financial Institutions,” written up by us here), but where does this leave us? There appears to be no place that is now safe for investors due to their lack of time or expertise to manage their own portfolios. This does for both retail and institutional investors. This piece from the IMF sort of declares that nowhere is safe, but isn’t that what risk and return is about?

Regulators have sought a gold standard of risk for years, with the result being a tightening on financial innovation and opportunity. Some greater risks in liquidity and fire sales have arisen in large part due to regulatory tightening (US Treasury volatility as one example). Regulators should indeed have a handle on systemic risk due to fire sales but investors will be no smarter tomorrow. There has got to be some leeway somewhere. The IMF chapter offers no breathing room on what practical solutions are for investors or their asset managers for investing. We think this point of reality is where regulators ought to head next. In the end, investors have to put their money somewhere.

A link to the IMF Global Financial Stability Report April 2015 home page is here.

A quick link to the Chapter 3 PDF is here.