The road to US tri-party reform has been long and winding, and has succeeded in mitigating over 90% of daylight credit exposure formerly associated with that market. Yet, structural efficiencies can still be found. Tri-party repo is not integrated with the core US securities settlement systems of DTC & FedWire Securities Services.

The road to US tri-party reform has been long and winding, and has succeeded in mitigating over 90% of daylight credit exposure formerly associated with that market. Yet, structural efficiencies can still be found. Tri-party repo is not integrated with the core US securities settlement systems of DTC & FedWire Securities Services.

When tri-party repo was first conceived in the US, it was intended to remove risk from the then market practice of letter (or hold-in-custody) repo. Instead, this end of day process remained, and tri-party added a new role into the mix to verify the collateral posted. The settlement process was essentially unchanged.

In 2009, the US Tri-party Repo Infrastructure Reform Task Force was created by the Fed to fix dangers in the repo markets exposed by the failure of Lehman Brothers and the Global Financial Crisis.

Several important milestones were met during the Task Force’s tenure, including BNY Mellon (BNYM) and J.P. Morgan (JPM) moving the start of tri-party settlement (the “unwind”) from 8:30AM to 3:30PM. This reduced daylight credit exposure by several hours.

Additional progress followed: in 2013, both BNYM and JPM stopped providing intraday credit for certain settlement types and in 2014 the Fed announced that intraday credit provided by the two clearing banks to support tri-party repo was below 10% of each participant’s book.

In 2015, the Fixed Income Clearing Corporation announced it would suspend the interbank service of GCF Repo®, which allowed some level of credit transferability between BNYM and JPM.

As in any industry, there are still opportunities for improvement. Solutions that can complement existing industry activities are the most beneficial. They avoid unnecessary disruption and can even provide access to untapped opportunities.

For instance, better connectivity between the US tri-party repo and the core US securities settlement systems could result in real time movements of collateral settling in securities settlement systems.

Currently, there is no actual securities settlement, but rather a semi-continuous stream of substitutions with an unwind at 3:30PM and a rewind that can take an hour or more.

Gauging the current health of the repo markets

With conflicting data on the Leverage Ratio, the Liquidity Coverage Ratio and at times the Net Stable Funding Ratio, it is difficult to tell how much tri-party reform has affected the US repo markets, or what the impact of repo integrated with securities settlement systems would look like.

Regulations have arguably resulted in reduced liquidity for treasury transactions at a time when the US Treasury is flooding the market with new issuance. This appears to be a driver for the US Treasury to propose exempting Treasuries from the Leverage Ratio largely to reintroduce market liquidity:

The current interaction of the leverage ratio, particularly the enhanced supplementary leverage ratio, and other rules creates incentives that discourage critical banking functions, including taking low-risk deposits, providing access to centrally cleared derivatives for market participants, and providing secured repo financing, which supports market liquidity.

Significant adjustments should be made to the calculation of the SLR. In particular, deductions from the leverage exposure denominator should be made, including for:

- Cash on deposit with central banks;

- U.S. Treasury securities;

- Initial margin for centrally cleared derivatives.

Taking US Treasuries out of the Leverage Ratio would also take US Treasury repo out as well, which could release additional liquidity.

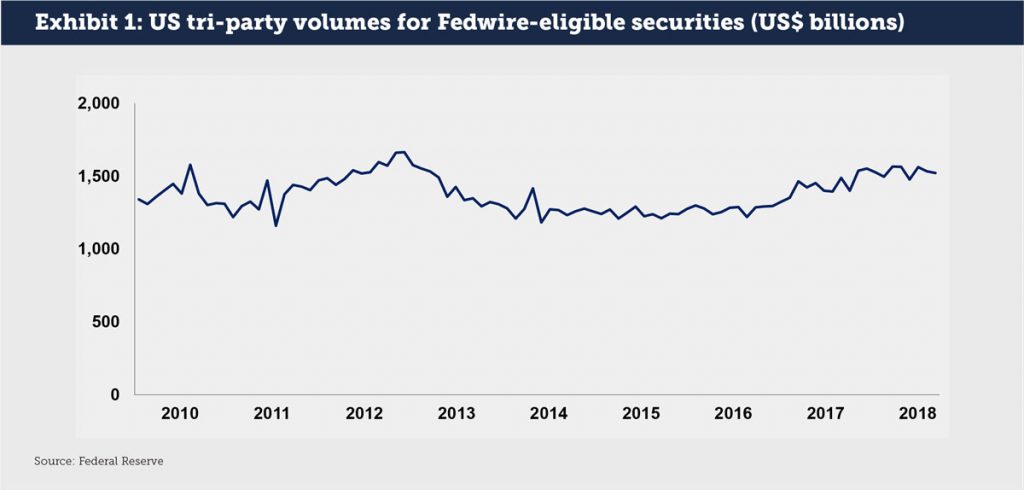

Data from the Federal Reserve show that repo market liquidity remains unsteady. Although the total Fedwire-eligible tri-party market has recovered from a low of $1.159 trillion in Q3 2011 to $1.8 trillion in Q1 2018, much of the increase had been due to the Fed’s own Reverse Repo Facility; only now are we seeing a growth in repo transactions between private sector market participants (see Exhibit 1).

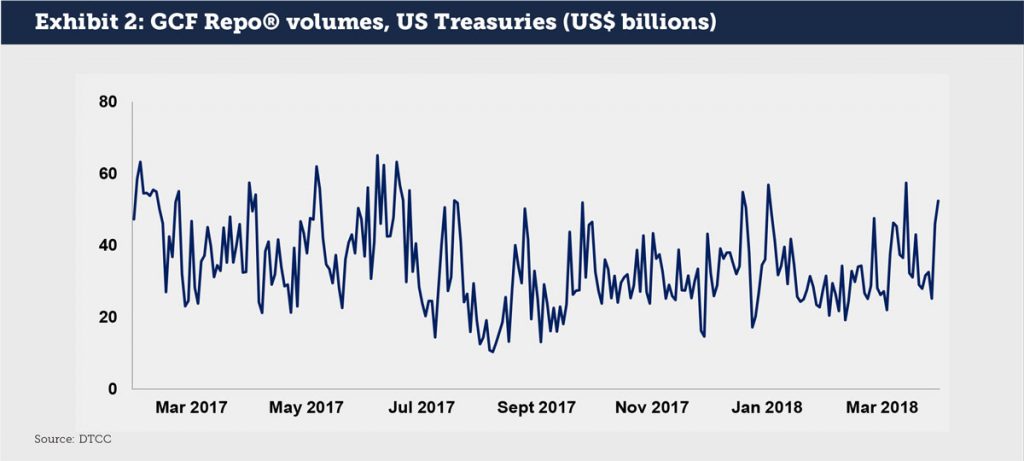

Meanwhile, GCF Repo® volumes have stayed close to US$50 billion in daily US Treasury volume for the last year (see Exhibit 2). This is much lower than the $150 billion that the market saw fairly regularly until the end of 2014.

What further tri-party evolution might look like

The industry continues to progress. Tri-party repo risk can be better managed with the new systems and controls in place. Repo and treasury desks have real time data which is enabling them to manage liquidity more effectively.

The more integrated tri-party financing becomes with the securities settlements systems, the more risk we can remove from the system. New opportunities may also emerge.

It’s a model that is already in use in Europe, and one which DTCC-Euroclear GlobalCollateral has adopted. The aim is to complement existing industry activities and connect US collateral users to new ecosystems of assets.

It could be a win for the entire industry.

Oscar Huettner is a New York based Product Sales Specialist for DTCC Euroclear GlobalCollateral – the Euroclear and DTCC joint venture – where he has worked to develop a global collateral management solution for secured financing and margin postings.

Prior to GlobalCollateral, Oscar spent almost 30 years in the international secured financing markets as a trader in New York and London. He established Barclays Capital’s European repo desk (1994), South African repo desk (1998) and RMBS repo desk (2004) and has held senior trading positions at IBJ International, Donaldson Lufkin and Jenrette and Salomon Brothers. Oscar has worked for BondLend, was a founding member of the European Repo Council and has served on numerous industry working groups.