Transactional data from late October 2014 show clearly the benefit of CCPs to dealers in the securities lending and repo markets. We have been saying for a while that we expected a two-tiered pricing market to develop as dealers preference the netting and risk-weight advantages of CCPs over their equivalent bilateral transactions. October spelled out the pricing difference in no uncertain terms for this end-of-month observation period.

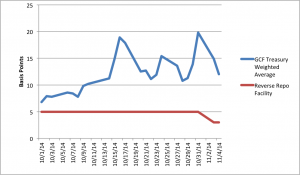

Data from DTCC’s FICC GCF repo transactions between dealers, and benefitting from netting, show that GCF Treasury repo went from 6.8 bps on Oct 1 2014 to 19.8 bps on Oct 31 2014 before falling again to 12 bps by Nov 4 2014 (see chart). The high point on Oct 31 2014 was reported at 22 bps.

Data from the Fed’s Reverse Repo Facility showed the Fed’s artificial floor at 3-5 bps. Volumes rose sharply at year end but did not approach the max in either dollar amounts or number of participants submitting bids.

Most importantly, data on GC repo in tri-party was priced below the Fed’s floor, at times negative or simply unavailable.

This answers the question, what’s the pricing benefit of a dealer-only CCP in a balance sheet sensitive environment? If Treasury or Agency overnight repo is going at 0 bps in tri-party repo, then the CCP benefit is 19.8 bps. If tri-party HQLA repo is simply unavailable otherwise then the CCP is priceless.

It will be important see how CCP-cleared repo equivalents behave when the number of market participants can increase substantially, and how repo CCPs price when the buy-side is allowed in as cash providers. We expect similar pricing dynamics to shape up on securities lending CCPs as agent lenders and beneficial owners become direct participants.