Bloomberg ran a story last week on derivatives for peer to peer loans. In “Wall Street’s Thinking About Creating Derivatives on Peer-to-Peer Loans,” Tracy Alloway and Matt Scully discuss recent trends by startups to create derivatives based on P2P loans (the title is a bit misleading). On the one hand this is a really interesting idea. On the other, who is going to buy them and how will the collateral quality be tracked?

The basics of the story are that “peer-to-peer lending and its Internet enablers like LendingClub Corp., the industry leader, are being pulled into the high-octane world of derivatives. While many hail Wall Street’s growing involvement, others warn investors could get carried away, as they did during the dot-com era and again during the mortgage mania. The new derivatives could help people hedge their risks, but they could also lure speculators into the market.”

Here are the pros and cons of what we see:

The story cites some small firms that are working to create new products out of P2P loans including SLMX, a start-up looking to make a total return swap type of product. This could work as a risk management tool if an investor is concerned about defaults. If an investor can’t buy a loan for legal reasons though, would they buy a TRS on the loan? Not so sure. This wouldn’t work for money market mutual funds in any size but may be fine for high net worth individuals.

We noted with interest a company called PeerIQ, that is collecting filings on P2P loans for stress testing, pricing, risk management and settlement. Any new market needs data to help it thrive. PeerIQ is taking a bet that P2P loans are enough of an asset class that sophisticated investors will need these types of analytics. But are there enough sophisticated investors buying P2P products en masse that need the data? There’s a lot of anecdotal evidence about hedge funds and institutions wanting to “snap up” P2P loans. We think about private funds like hedge funds and family offices as the principal buyers. The article cites, and we know also, that investment funds are active in this marketplace.

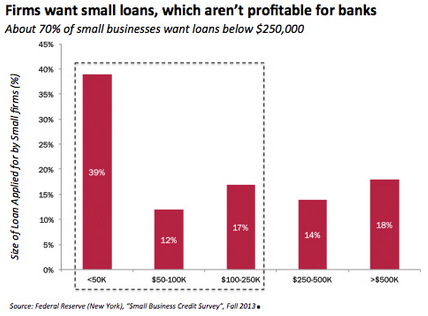

We haven’t seen any data on the size of demand for buying loans, but we have seen data that show that P2P markets seem better suited than banks for providing the types of loans that small business owners want. Karen Mills, former Administrator for the US Small Business Association, wrote in Fortune that “Many banks make loans today pretty much the way they did 50 years ago, relying on expensive personal underwriting and a mountain of paperwork. That makes small dollar loans not economical. Yet, loans under $250,000 are what most small businesses want. Add to that, the number of community banks – a critical source of small business loans – has been shrinking, from 14,000 in 1984 to less than 7,000 today.” The article cites Federal Reserve data showing the concentration of loans by small business owners at 68% under $250,000 (see Exhibit). In many ways this is a question about credit and income validation. If the P2P markets can do this faster and more efficiently than banks, their loans will be less expensive to produce and hence smaller loans can be more profitable.

The P2P loan space is very interesting but may now be crowded. Equally important is how much credit do small business owners really need? We’ve heard talk about P2P extending into emergency room operations and other very much non-business activity. At that point these just personal loans with no collateral besides a person’s income. Will derivatives and analytics help the market grow by increasing demand? Risk management and the right packaging will help, but bigger questions on what the P2P market really means and how credit, and hence collateral, is verified will need resolution before derivatives can expand the buyer pool to a mass audience or have enough liquidity to provide their goal of robust risk management.