The global repo markets continue to manually process the majority of business, opening the door to fails and errors that cost extra time and money to resolve. In addition, the new Central Securities Depositories Regulation (CSDR) will impose fines for fails and prompt systems changes worldwide. A ready solution to this problem is a greater move to electronification and Straight-through Processing (STP) that eliminates these inefficiencies. We call for the market to reach 75% transactional volume in STP by 2025 as a realistic goal. A guest post from MarketAxess.

Markets don’t fare well when manual intervention is required to manage a very large volume of transactional activity: financial history offers plenty of examples of what can happen when operational errors compound. On the other hand, electronic affirmation comes with a high degree of automation that has proven beneficial to operational efficiency. Automated contract matching can ensure that each side knows the same rate, issue, margin, term, nominal amount, start and end dates, cash settlement amount and direction. The global repo markets stand to benefit from this process as much as other products.

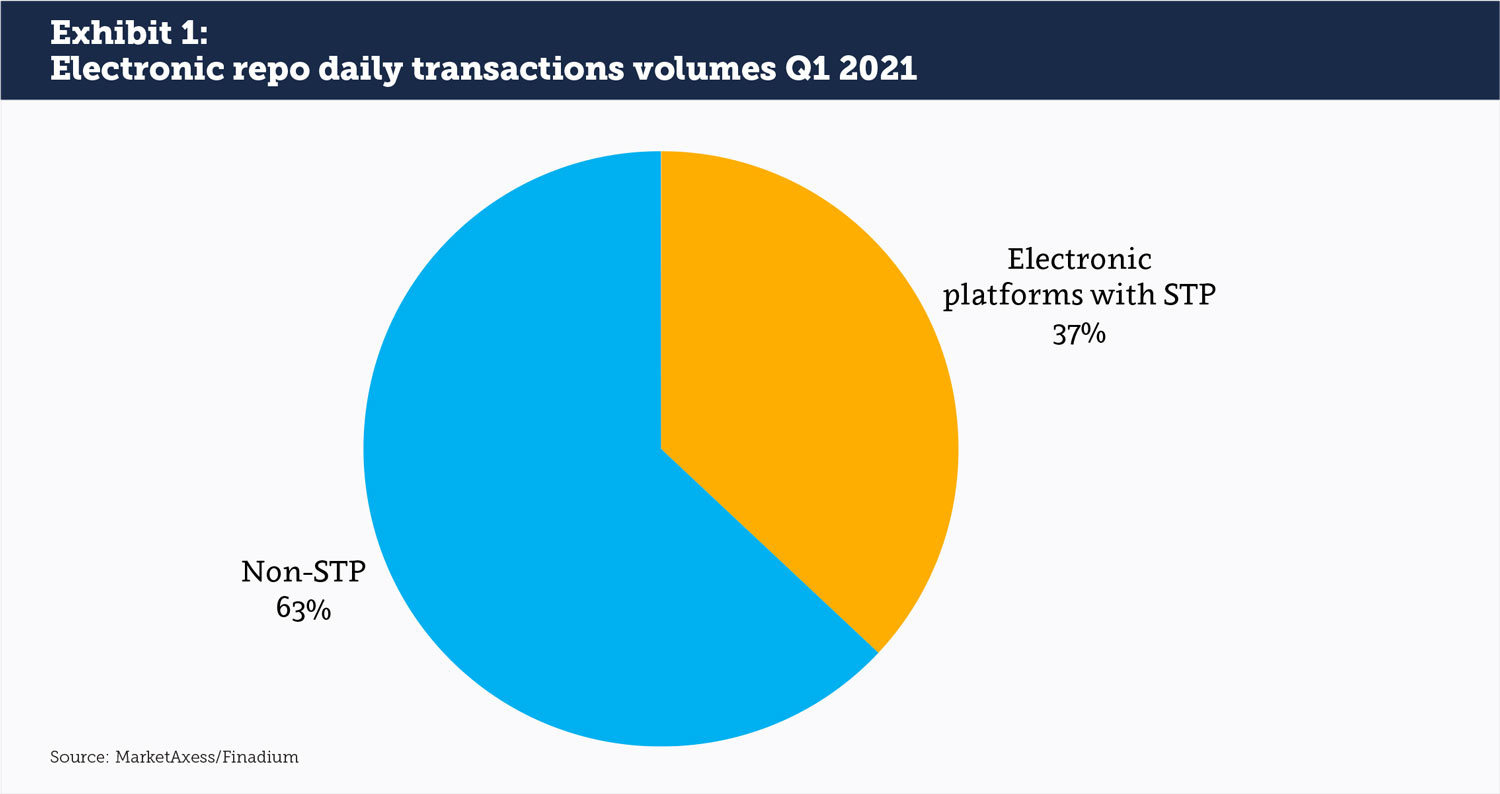

In a new analysis, we find that 37% of repo transactional volume is currently traded electronically with STP in North America and Europe; this includes volumes negotiated verbally and by email then inputted onto a platform as well as transactions that are traded on-platform to start (see Exhibit 1). This daily transactional business combines the electronic trading volumes of the many repo venues in the market as the numerator, with data from SFTR, DTCC and other official sources in North America as the denominator. While 37% is not bad, we believe that much more could be done. The remaining 63% of non-electronically traded daily business can still achieve greater levels of electronification than today with the right supports.

One reason why so much repo has stayed manual for so long is the relatively slower adoption of technology in repo compared to other parts of capital markets. The underlying bilateral trades look just like they did decades ago, utilizing credit lines, settlements, margining and other post-trade tasks that require a long tail of infrastructure; the underlying complexity of the market can make changes slow to adopt. By comparison, electronification requires the ability to shift capabilities onto platforms that may or may not yet exist internally.

The adoption of improved technology across firmwide infrastructures, and not just repo, combined with the greater STP on electronic platforms, creates an opportunity for quick advances. In something of a rarity in recent years, this shift is achievable by individual firms where first mover advantage is real; there are no industry working groups or regulations necessary to capture the lowest hanging benefits.

Why more STP makes sense for individual firms

The cost of not automating is found in fail expenses. Our client experience is that the percentage of market fails in repo is 2-4% of all trades resulting a daily market impact of €93 billion in misallocated funds. We have seen fails result in extra payments of €5,000 between counterparties, which can eliminate profit from the trade and force one side to correct a cash shortfall, with attendant operational costs.

The ability of a firm to self-correct is limited by their own amount of STP. As each firm adopts more electronic trading and automated matching, their fails will naturally decrease. MarketAxess’ Repo platform ensures that any potential errors are caught and resolved on T+0, leading to trades matched on trade date (see Exhibit 2). Both parties need to be on an automated platform to see the benefit: it only takes one side to book an erroneous trade to start the cycle. But the entire Industry does not have to go electronic in order for benefits to accrue. The more counterparties that a firm can electronically confirm with, the lower they can drive their exceptions.

A regionalized approach

A regionalized approach

The European rational driving in favor of the electronification of is well known: the Securities Financing Transactions Regulation (SFTR) has mandated reporting with time stamps, LEIs and other features. All of these are difficult to deliver without electronic platforms. ESMA has reported that the rejection rate of SFTR trade submissions declined rapidly from launch in July 2020 through January 2021, from 9% to under 2%, in part due to STP. However, matching rates are not ideal and more work needs to be done. Whether CSDR finally arrives with buy-ins or not remains to be seen, but when the cash penalties are enforced then the entire industry needs to ensure that fails are at an absolute minimum.

In the US, settlement of credit instruments through DTCC is efficient and few firms are deeply concerned about fails in the US Treasury market. Cost comparison remains problematic however and breaks are frequent. Sometimes failing can be a strategic move, for example if the rate of a Treasury hard to borrow is 4% but the fine for failing is 3%, but persistent fails are recognized as a cost drain when bilateral trade comparisons do not match. This remains a large piece of unfinished industry business. While the US does not expect new regulations that fine fails, businesses that operate globally may see a European mandate like CSDR as a reason for engaging in the global no-fails project. That could lower fail rates and the operational headaches they bring, even if the US is not considered a large problem on its own.

Asian markets on the other hand are at the beginning stages of what the electronification of repo could mean. There are potentially dramatic advances that could occur in the region, including business transformations resulting from a movement of manual to electronic processing activity. While the benefits of electronification will take time to emerge, any steps forward now by individual firms or the market as a whole could result in outsized positive consequences.

What will push the markets to automate further?

The manual nature of bilateral repo processing and the impact of costly errors encourages a continued push toward the adoption of electronification. . This will happen alongside an increased focus on internal technology projects that support efficient data management across the firm and on repo technology in particular. The larger sell-side and buy-side firms are already leading the charge and are benefitting from less time, money and effort spent in exception processing and the cost of fails management.

The creation of better and broader data pools will both drive the adoption of electronification and will be driven by it in a self-reinforcing loop. The creation of same day databases of relevant trade information can be leveraged to automate the passing of that data between systems, furthering a firm’s automation process. This project of ensuring that each system has the same data is an internal effort, but collecting that data relies on efficient interactions with trading platforms and matching utilities.

The opportunity to drive more electronification and STP in place of manual processing is an opportunity to reduce costs and increase efficiency. At an estimated 37% of trading today, the amount of electronic repo activity is not bad but could be much better. We encourage the industry to consider 75% as a realistic target for all repo electronic trading and STP by 2025. This will in turn lead to much greater rates of STP than are currently achieved.

Camille McKelvey is the Head of Business Development STP, for MarketAxess Post-Trade. Camille actively works with the industry to improve Post-Trade automation across the cash and repo markets, as well as looking for new, innovative ways to address client’s workflow challenges. Since joining MarketAxess is 2014, Camille has developed the Match Post-Trade platform and significantly grown the market share. Prior to joining MarketAxess she spent 10 years in investment banking. Camille actively participates in promoting diversity and inclusivity within financial services as a founding steering committee member of the International Capital Markets Association Women’s Network.

Camille McKelvey is the Head of Business Development STP, for MarketAxess Post-Trade. Camille actively works with the industry to improve Post-Trade automation across the cash and repo markets, as well as looking for new, innovative ways to address client’s workflow challenges. Since joining MarketAxess is 2014, Camille has developed the Match Post-Trade platform and significantly grown the market share. Prior to joining MarketAxess she spent 10 years in investment banking. Camille actively participates in promoting diversity and inclusivity within financial services as a founding steering committee member of the International Capital Markets Association Women’s Network.