The Bank for International Settlements published a briefing from staff at its Financial Stability Institute (FSI) on the writedown of Credit Suisse (CS) AT1 instruments.

- As demonstrated by the recent Credit Suisse episode, outside resolution, some Additional Tier 1 (AT1) bonds may be written down entirely before the wipe-out of Common Equity Tier 1 (CET1). This situation implies a transfer of value from holders of such AT1 bonds to shareholders.

- While the the isolated write-down is feasible in many jurisdictions, unintended consequences associated with the use of this mechanism may lead authorities to only write down these bonds in resolution. This would effectively deprive them of their ability to absorb losses on a going-concern basis.

- Since the AT1 instruments were conceived for the purpose of absorbing losses on a going-concern basis, there may be merit in considering whether the current design of AT1 instruments remains fit for purpose or whether adjustments to the regulatory framework might be necessary.

- In addition, given the potential for market misperceptions regarding the functioning of AT1 bonds, authorities may wish to consider whether there is merit in pursuing regulatory work aimed at increasing the transparency and disclosure of AT1 instruments’ characteristics.

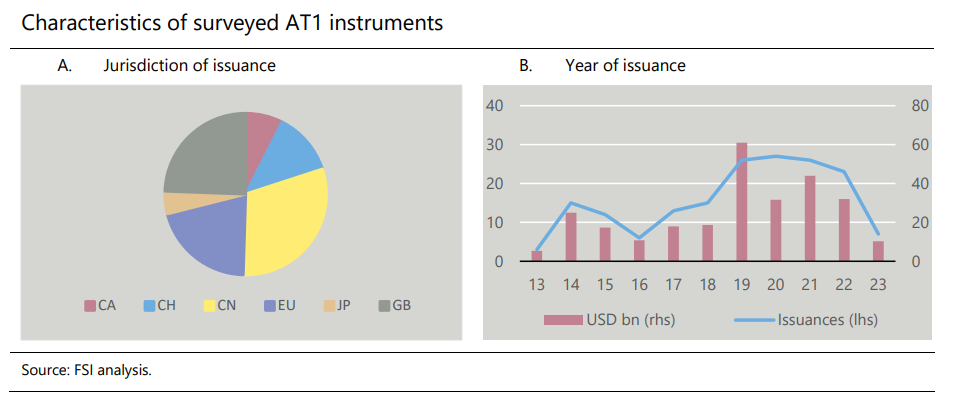

Researchers concluded that in principle, an isolated writedown of AT1 instruments, and hence a transfer of value, is possible under specific circumstances in most jurisdictions analyzed in the paper — EU, Japan, Switzerland and the United Kingdom — upon the occurrence of a quantitative trigger event, if such event was to take place outside resolution.

Experience shows, however, that this would be an improbable event as authorities are likely to take a resolution action before capital adequacy ratios breach trigger levels. Nevertheless, an isolated writedown would be feasible in China, Japan and Switzerland (but not in the EU or the United Kingdom), if authorities in those jurisdictions were to write down AT1 instruments on the basis of the qualitative trigger before putting the failing bank in resolution.

Experience shows, however, that this would be an improbable event as authorities are likely to take a resolution action before capital adequacy ratios breach trigger levels. Nevertheless, an isolated writedown would be feasible in China, Japan and Switzerland (but not in the EU or the United Kingdom), if authorities in those jurisdictions were to write down AT1 instruments on the basis of the qualitative trigger before putting the failing bank in resolution.

In practice, however, some authorities may wish to avoid the transfer of value from AT1 bondholders to shareholders. This stance may be justified, for example, on the basis of concerns about negative market reactions and the functioning of AT1 markets. This, in turn, would imply that authorities would only impose losses on AT1 instruments as part of a resolution action. This is because authorities lack powers to impose losses on shareholders outside resolution. This seems to imply that most AT1 bonds would in practice become an instrument with limited capacity to absorb losses on a going-concern basis.

Since the AT1 standard was designed precisely for the purpose of absorbing losses on a going-concern basis, there may be merit in considering whether the current design of AT1 instruments remains fit for purpose or whether adjustments to the regulatory framework might be necessary.

Moreover, the market reaction following the decision by Swiss authorities to write down CS AT1 instruments seems to suggest that some market participants may not fully appreciate that, while broadly similar, writedown conditions may differ across AT1 instruments. As a result, national authorities and standard-setting bodies may wish to consider whether there is merit in pursuing further work to increase the transparency and disclosure of AT1 instruments’ characteristics with a view to improving the functioning of the markets for these instruments.