The global collateral marketplace has grown to €25.57 trillion, up 6.5% since the December 2022 figure of €24 trillion, according to Finadium analysis. The increase shows that market participants will continue to drive efficient, cross-product and interconnected collateral technology to protect and expand their balance sheet capabilities. Distributed ledger technology (DLT) is an ideal mechanism to solve this problem set.

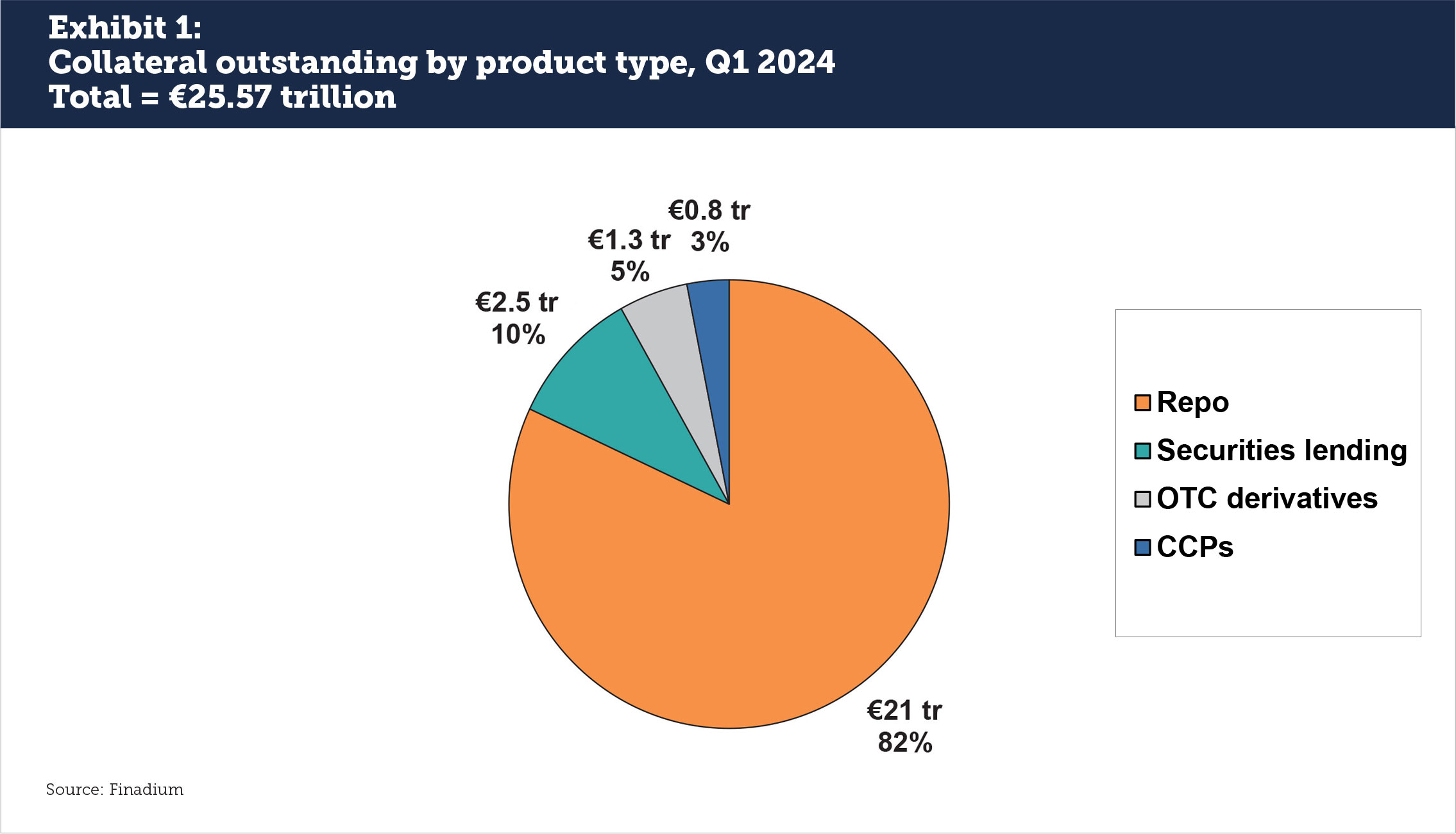

Data from Q1 2024 on collateralised trading markets show total asset values at €25.57 trillion across repo, securities lending, OTC derivatives, CCP-cleared derivatives and other products (see Exhibit 1); these are assets held and do not reflect intraday trading volumes. Several of these markets are growing: the European repo market increased from €10.4 trillion in 2022 to €10.9 trillion in 2024. The US primary dealer repo market expanded even more, from US$5 trillion a few years ago to over US$7 trillion today. While values for some products have stayed constant, including securities lending and OTC derivatives margin, the overall demand for collateralized trading products is on the rise.

Two sources of growth in the collateral markets have been higher interest rates and trading opportunities made possible by increased government bond issuance. These have led to pullbacks in central bank-led market activity in favour of the private sector. Eurex’s GC Pooling average outstanding volumes for example have mostly been between €700 billion and €800 billion for the last year, up from €100 billion to €200 billion just three years ago. Even a decline of US$1.5 trillion in the Federal Reserve’s Reverse Repo Facility (RRP) has not dented the growth of collateralised activity. While some volumes have gone to cash products, another portion simply moved from government to private sector books.

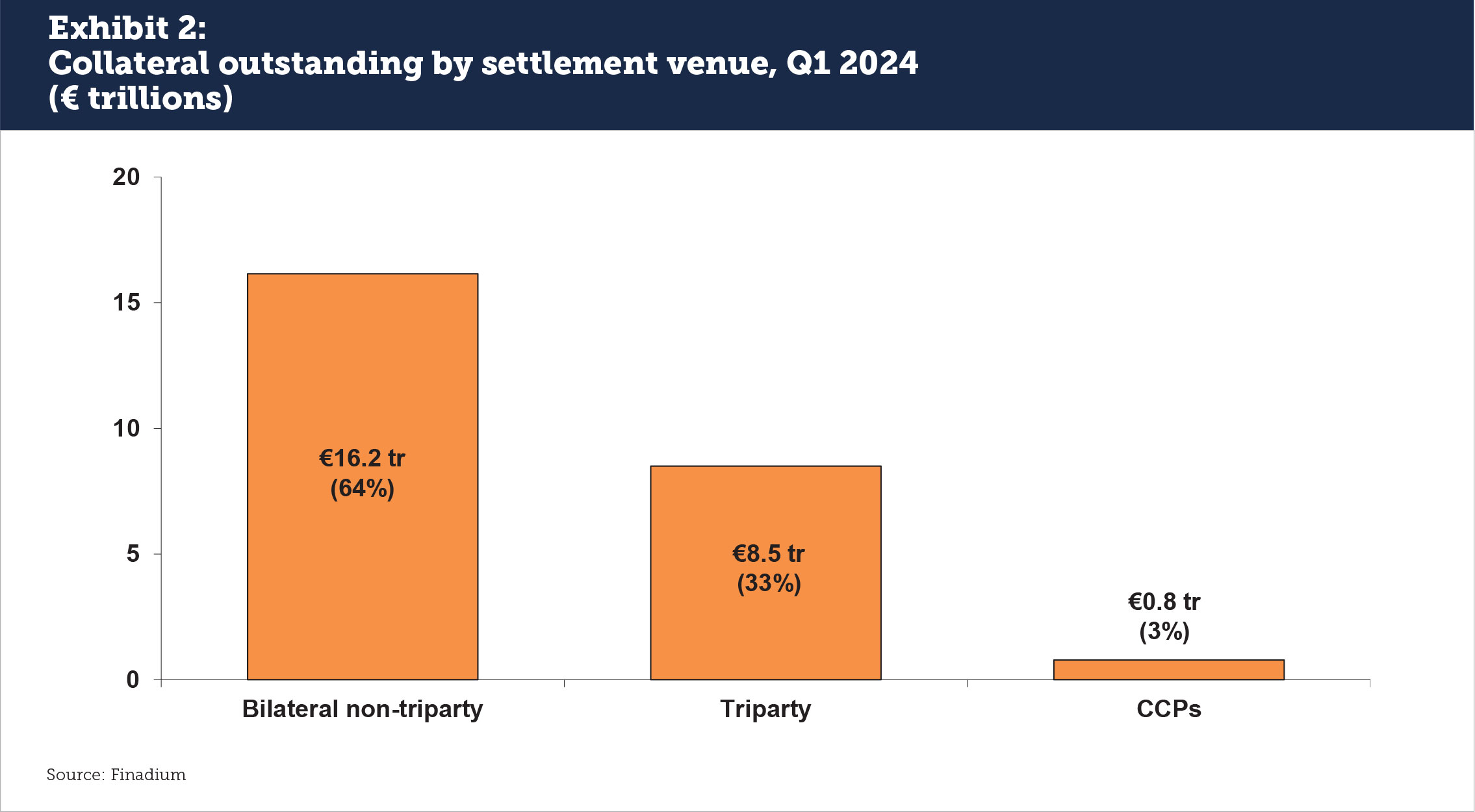

Across bilateral, triparty and CCP business, the greatest growth over the last two years occurred in the non-triparty bilateral market, at 12%, from €14.4 to trillion to €16.2 trillion, which is now 64% of the business (see Exhibit 2). Triparty grew more slowly at 4% as triparty agents have supported their clients in being more efficient with collateral. Triparty accounts for one-third of collateral held across nine triparty agents, with the majority managed by BNY, Euroclear, J.P. Morgan and Clearstream. The amount of CCP collateral holdings declined by 39% – a function of the amount of business being done, position netting and trade compression services. CCP-held collateral now accounts for just 3% of the market.

HQLAX‘s DCR solution

HQLAX‘s Digital Collateral Records (DCR) solution can be used by any market participant looking to access inventory between clients, counterparties and service providers. This includes custodians, central securities depositories (CSDs), triparty agents, banks, and both regulated and unregulated investment firms.

The solution optimizes collateral management by decoupling the relationship between ownership transfers from where collateral is held. There is no required development work for users to interface directly, said Erica De Rosa, Solutions Architect at HQLAX; the question is whether they would like their service providers, acting on behalf of hundreds or thousands of clients, to be part of the DLT ecosystem.

The same principles of the DCR can apply to all collateral products where dealers need to manage their inventory and operations, including repo, OTC derivatives and intercompany exposures. HQLAX lives downstream from trading venues and can capture collateral requirements across multiple bilateral channels, API or SWIFT messaging, letting clients see the settlement of their trade in a delivery-vs-delivery (DVD) format. DCRs can co-exist with central counterparties (CCPs) as well, and can solve additional pain points that arise from collateral calls and operational complexity for users on CCPs.

Integrating digital cash as a settlement option

While HQLAX started out providing non-cash settlement only, recent advances with Fnality’s universal settlement coin and J.P. Morgan’s JPMCoin introduce important new functionalities for users. In a June 18, 2024 press release, HQLAX said that “Fnality and HQLAX have completed the first successful end-to-end (E2E) testing of a cross-chain intraday repo settlement. The trade was submitted in Eurex Repo F7, collateral was earmarked on HQLAX, and cash was earmarked on the Sterling Fnality Payment System TestNet,” and that “Fnality and HQLAX are now preparing to officially launch wholesale cross-chain repo settlements in live environments later this year, subject to regulatory approvals.”

Introducing digital cash settlement on DLT has been a missing piece for some firms to successfully operationalise the technology. The idea of cash-on-chain, where cash can be on-ramped then off-ramped as needed, means that traders can get their money in and out of the system as necessary. This fungibility of cash and securities on- and off-chain makes DLT solutions much more efficient for dealers than other options. The build-out of this functionality requires an ecosystem that is in a rapid process of development.

Major custodians and CSDs are already live with digitized cash in some form; the more that each connects to DLT platforms like HQLAX, the more varied opportunities there are for clients to use the platform. Guido Stroemer, Co-founder and CEO of HQLAX, said that “Our platform vision is to enable frictionless and precise ownership transfers of collateral across the full product suite of collateral management activities, including securities lending, repo and derivatives.”

Ultimately, DLT platforms can support market resilience and reduction of market stress owing to the need to meet collateral requirements, said HQLAX’s De Rosa. Clients will need to have more precision and control over both intraday and end of day transactions. As total collateral values continue to increase in the market, there is a growing argument that solutions like HQLAX‘s DCR that make collateral more efficient market-wide will become more of a market standard by virtue of their speed and convenience.

This article was sponsored by HQLAX.