Standard metrics point to an improvement in Treasury market liquidity in 2024 to levels last seen before the start of the current monetary policy tightening cycle. Volatility has also trended down, consistent with the improved liquidity.

While at least one market functioning metric has worsened in recent months — yield curve “noise” — that measure is an indirect gauge of market liquidity and suggests a level of current functioning that is far better than at the peak seen during the global financial crisis.

In a blog, the Federal Reserve said that since mid-2023, bid-ask spreads have been narrow and stable, and order book depth has generally been rising since March 2023, hitting levels comparable to those of early 2022, albeit with a temporary decline early August 2024 around a weaker-than-expected employment report and global equity market declines.

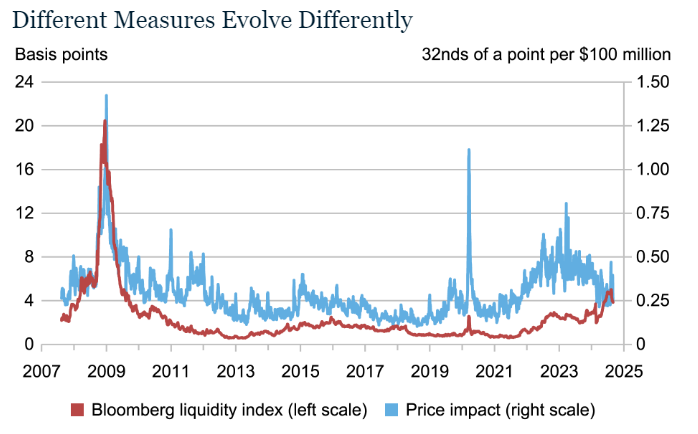

Measures of the price impact of trades also suggest an improvement in liquidity: price impact rose sharply again in March 2023, and then trended down to levels last seen in late 2021 or early 2022, before rising temporarily in early August 2024.

The improvement in liquidity over the past eighteen months has been accompanied by a decrease in price volatility. Moreover, the current level of liquidity is consistent with the current level of volatility, as implied by the historical relationship between the variables.

A Conflicting Measure?

While the measures discussed so far point to liquidity that is improving and far better than it was in March 2020, this is not true for all measures. So-called yield curve “noise” measures, which gauge the dispersion of individual Treasury security yields around a smoothed yield curve, have recently risen, suggesting decreased liquidity.

Dispersion does not measure liquidity directly, but it is thought to reflect the amount of arbitrage capital in the market and hence serve as a proxy for liquidity

The market’s capacity to smoothly handle large trading flows has been of ongoing concern since March 2020, debt outstanding continues to grow, and recent empirical work shows how constraints on intermediation capacity can worsen illiquidity. Close monitoring of Treasury market liquidity, and continued efforts to improve the market’s resilience, remain appropriate.