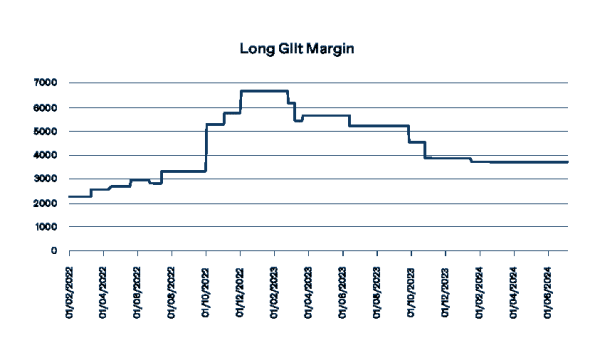

Financial markets witnessed a dramatic two-fold surge in the initial margin requirements for long gilt futures in the aftermath of then UK prime minister Liz Truss mini-budget fiasco of 2022, according to data from OpenGamma.

The initial margin for ICE long gilt futures spiked to an eye watering £6,650 following the controversial fiscal event which saw the government at the time pledge major unfunded tax cuts. This period also saw heightened variation margin demands, forcing investors to fire sell gilts and further destabilizing the market. Up until the budget meltdown, long gilt futures had seen modest increases from £2,240 to £3,280.

Since the mini-budget, initial margins have gradually decreased, yet they remain elevated compared to pre-crisis levels, stabilizing at around £3,680 since early January this year. This prolonged elevation reflects ongoing caution in the market, with margin requirements adjusted based on the worst-case historical scenarios.

The findings follow the Bank of England’s system-wide exploratory scenario (SWES) exercise in June 2023 – highlighting the necessity of stress testing to evaluate liquidity requirements. Currently, financial entities, including investment banks, insurers, and asset managers, are modelling the impact of hypothetical shocks and planning their responses. This phase will be followed by a second round of stress testing, which will consider the potential amplification effects of actions like closing positions or selling assets.

The current SWES exercise aims to provide a clearer picture of liquidity needs and the systemic impact of stress events. Final results are expected by the end of the year, offering crucial insights into the preparedness of financial systems to withstand significant shocks.

Jo Burnham, a margin expert at OpenGamma, said in emailed commentary: “The steep rise in initial margin post the mini budget illustrates the fragility of our financial system when under extreme stress. It’s a stark reminder of the importance of strong stress testing to anticipate and mitigate such liquidity crises. These measures are essential for ensuring the resilience of financial markets in the face of unforeseen economic shocks.”