In a recent report, the US finance ministry noted that Inter-Agency Working Group (IAWG) initiatives designed to increase transparency have been helpful in increasing the dissemination of information for private and public parties to evaluate market risks, with recent examples being Office of Financial Research (OFR) data collection on bilateral repo and FINRA’s release of transaction-level data.

The IAWG is composed of staff from the US Treasury, Federal Reserve Board, New York Fed, Securities and Exchange Commission and Commodity Futures Trading Commission.

The Treasury report also noted potential concerns such as the large deficits, limited growth in dealer intermediation capacity compared to increases in issuance, the change in demand for Treasuries from traditional parties such as asset managers, and the growing role of Principal Trading Firms (PTFs) in market intermediation are risk factors that should be monitored

“The IAWG should consider additional initiatives such as centrally clearing the [Standing Repo Facility], various ways of exempting Treasuries from the [Supplementary Leverage Ratio], and putting a greater focus on risks generated by month-end spikes in trading volume for existing stress tests,” the report stated.

SLR exemption

The SLR disincentivizes banks from holding low-risk, high-quality assets because they count toward banks’ total exposure, which increases the amount of costly regulatory capital they are required to hold. The policy consideration is a countercyclical design to temporarily exempt Treasuries and central bank reserves from the SLR, in either a systematic or discretionary fashion, to allow banks to support market liquidity during market stress.

“A permanent exemption could also be considered as part of holistic update of bank capital rules that balances the liquidity needs of the financial system while preserving resilience and stability of banks,” the report stated.

SRF clearing

Despite increases in hedge fund presence and the basis trade, movements of repo relative to the Fed’s administered rates have been relatively benign compared to before Covid. It is unclear how much of this should be attributed to IAWG efforts versus the continued abundance of funding liquidity.

Money market reform has reduced the risk of runs during periods of financial stress and keeps funding liquidity in private markets. Meanwhile, the Standing Repo Facility (SRF) and Foreign and International Monetary Authorities (FIMA) repo facility provide backstops that should reduce risks of precautionary sales of Treasuries.

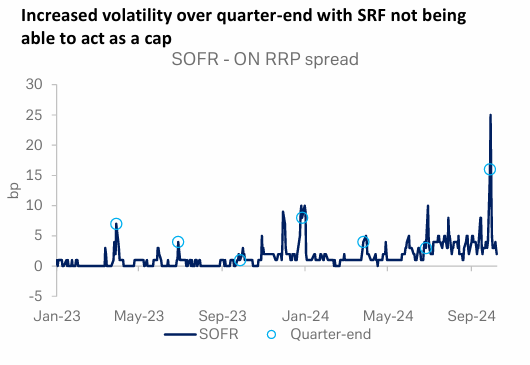

However, the facilities are untested in periods of acute stress and the SRF also faces limitations given its triparty structure (not centrally cleared). The late-day operation time also presents a challenge to dealers who need to borrow cash in the morning to prevent daylight overdrafts with their settlement bank. As a result, the SRF can dampen repo pressures but does not function as a ceiling on rates.

The SRF may have limited impact on funding pressures that arise from limits to dealer intermediation capacity because borrowing in the facility is not netted, and the policy consideration is to centrally clear SRF operations to enable netting of funds borrowed to support onward lending to other market participants.