Repo liquidity is often discussed but can be hard to measure: all firms require it but not every firm can access it at the right time and at the right price. Central counterparties (CCPs) in government debt repo help ease the access problem, which is why repo CCPs see burgeoning activity at times of market stress or whenever bank balance sheets are tightening.

Sell-side dealers and buy-side market participants continue to focus on resource and cost efficiencies, including the need to optimise financial resource management, whilst ensuring that they have access to reliable pools of cleared liquidity in all market conditions. Access to the right liquidity pools and partners is a primary part of this analysis; this creates opportunities for improved pricing and potential risk optimisation. Adding repo clearing to their liquidity toolbox allows members to optimise their financial resources, as qualified CCPs attract minimal RWA and facilitate balance sheet netting.

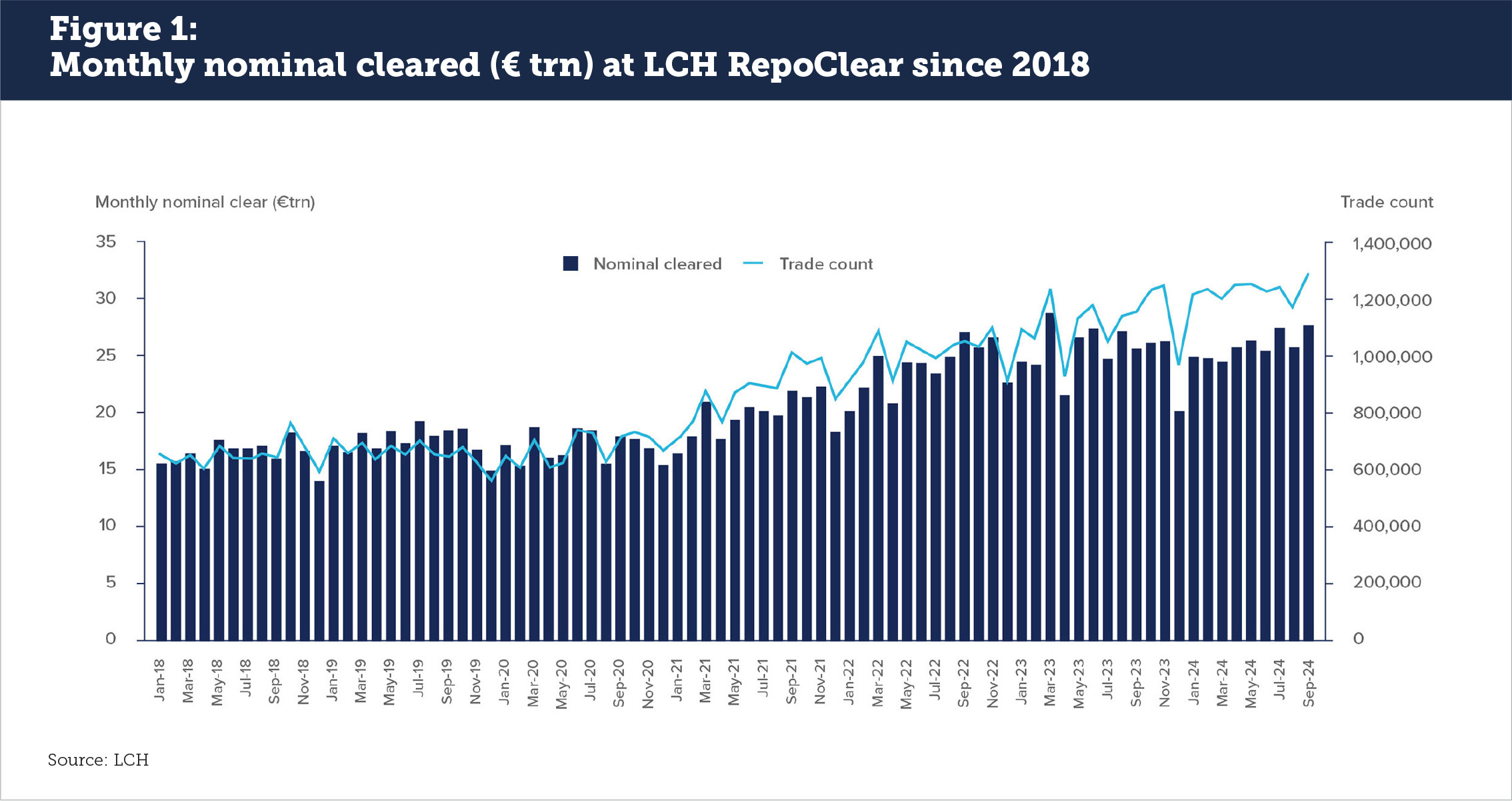

LCH RepoClear is seeing first-hand the results of market interest in reliable liquidity combined with balance sheet optimization. Volumes in Q3 2024 were up on Q2 2024 levels, with €80 trillion nominal cleared (up 3.1% vs Q1 2024) (see Figure 1).

Multiple regulatory factors suggest that repo clearing volumes will continue to increase, which produces opportunities for additional benefits for existing clearing members. Outside of regulatory mandates, the Basel III framework will increase bank risk-based capitalisation and further constrain bank leverage, resulting in increased capital consumption for non-cleared bilateral trades. Clearing with a Qualifying CCP typically carries a 2% risk weight compared to the 100% risk weight (RWA) of some bilateral counterparties. While margin and risk waterfall costs at the CCP are a known cost, when compared to many bilateral transactions, the trade off in RWA reduction is seen to be worth it based on increasing volumes. This becomes more apparent when increased CCP activity leads to greater netting opportunities, which in turn lowers member capital requirements.

Even without these benefits, there is an argument to be made that repo CCPs are the outlet valve for bottlenecks created by tighter regulation on bank balance sheets. This changes the consideration of CCPs as a stress relief mechanism into one that is used every day on an increasing basis as simply a better way to manage costs and service clients. At LCH RepoClear, we are hearing this conversation more frequently with our clients and expect this to be the direction of travel going forward.

Repo Clearing is at the forefront of firms’ considerations

The US Securities and Exchange Commission (SEC) is requiring that mandatory clearing of US Treasury repo will go live in June 2026, based on current expectations. This relatively short timeline means that every firm around the world that trades and finances US Treasuries must become educated and create an execution strategy around the new rules. At the same time, the new focus on the US clearing requirement means that firms are reviewing global clearing models. The rationale is that if they are going to do the work once, they might as well take a holistic approach to CCP adoption.

The US may have broken the ice but there have also been conversations about increased repo clearing for European Government Bonds. The Bank of England looked at the matter in June 2023 and found that “More widespread central clearing could enhance dealers’ ability to intermediate financial markets by increasing the netting of buy and sell trades, thereby reducing the impact of trading on balance sheets and capital ratios.” However, market participants are mixed on the value of a clearing mandate in the UK and Europe, and the focus seems to be more on how to facilitate access to repo clearing than mandating it.

The importance of buy-side clearing models

Both dealers and clients recognize that buy-side clearing access models are critical for market stability and liquidity. CCPs that offer reliable, cost-effective clearing models for the buy-side can best serve the needs of the diverse repo market audience. LCH RepoClear plans to offer two Sponsored Clearing models:

Existing model: Sponsored Clearing. LCH Ltd has now received regulatory approval to deliver significant enhancements to its existing Sponsored Clearing model for Gilts and LCH SA will be delivering the same enhancements for Euro debt (subject to regulatory approval). Our Sponsored Clearing service has seen significant growth in Euro debt volumes this year, as more dealers connect and quote prices. This creates even greater opportunities for netting benefits.

Future model: Guaranteed Sponsored Clearing. Our Guaranteed Sponsored clearing service will extend the benefits of direct CCP membership to a broader range of buy-side firms, including certain alternative investment funds, such as hedge funds (subject to regulatory approval).

The model will allow sponsoring banks to enhance their existing transactional and clearing relationships and unlock greater netting efficiencies. Equally, the model will enable hedge funds to benefit from access to the largest pool of cleared repo liquidity and meaningful settlement efficiencies.

In parallel, LCH RepoClear is enabling key funding providers, including selected supranationals and central banks, to join our pool and provide liquidity.

Aligning margin models with market needs and regulation

As a central counterparty, LCH is required to conservatively calibrate its margin models to prioritise financial stability in accordance with its high-risk management standards. The goal is to maintain a stable, anti-procyclical model that is transparent and avoids market disruption during times of stress, while securing appropriate protection for CCP members.

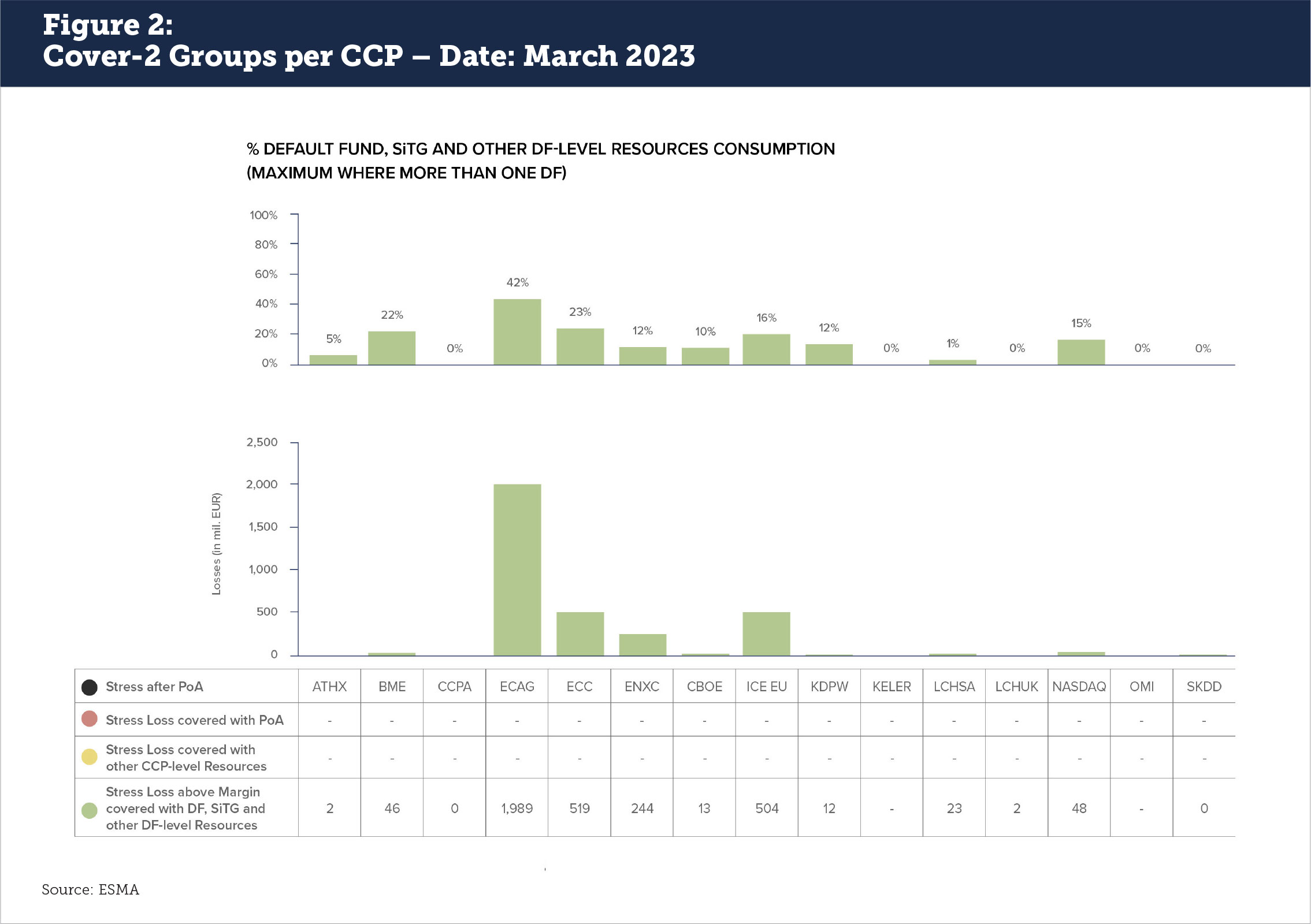

Our margin models safeguard resilience under conditions of market stress as highlighted in the ESMA 2024 stress testing report, for which two default scenarios were run, combined with a common market stress scenario based on CCPs’ positions on 16 December 2022 and 17 March 2023. LCH SA cover 2 results are robust compared to the market (see Figure 2).

LCH RepoClear will continue to be the market’s partner in ensuring the offering of the deepest cleared repo liquidity pools for Gilts and Euro debt. The structural composition of this pool enables participants to enjoy remarkable margin and netting opportunities, framed on stable and anti-procyclical risk management practices.

It is in LCH’s DNA to partner and accommodate the needs of market participants. Our flexible open access approach allows members and clients to choose from a range of trade venues for execution, and a range of CSDs and ICSDs for settlement. Recently, this has been illustrated by the connections of Tradeweb’s dealer-to-dealer platform (Dealerweb), in addition to €GCPlus being available to trade on BrokerTec Quote.

We will continue the open dialogue with the market to understand the needs of participants and address these with innovative solutions. We also look forward to further delivering on our commitment to supporting our members and clients, launching more new products over the coming months, and to further expanding the repo clearing ecosystem.

The information contained in this article is for information purposes only. All information is provided to you on an “AS IS” basis and may not be accurate or up to date. No warranties or representations, whether express or implied, are made in relation to the information. No responsibility is accepted by or on behalf of the LCH Limited (“LCH”) or any members of the London Stock Exchange Group (“LSEG”) for any errors, omissions or inaccuracies in the information and for the results of any actions or investment decisions taken by you, or anyone else or any organisation following the provision of this information to you. The information does not constitute professional, legal, regulatory, financial or investment advice and has not been verified, endorsed, or otherwise validated by LCH or LSEG. You are responsible for conducting your own research and due diligence before entering into any contract, or making any investment and any contract or investment made is entirely at the risk of the person or organisation entering into the contract or making the investment.