Term repo fulfills an important function for trading firms in allowing them certainty in financing by volumes and rates, especially over periods of potential volatility like year-end. This year, Eurex is seeing a heightened demand for term repo as well as very positive rates. This compares to the US where market participants have noted a lack of term repo options going into 2025.

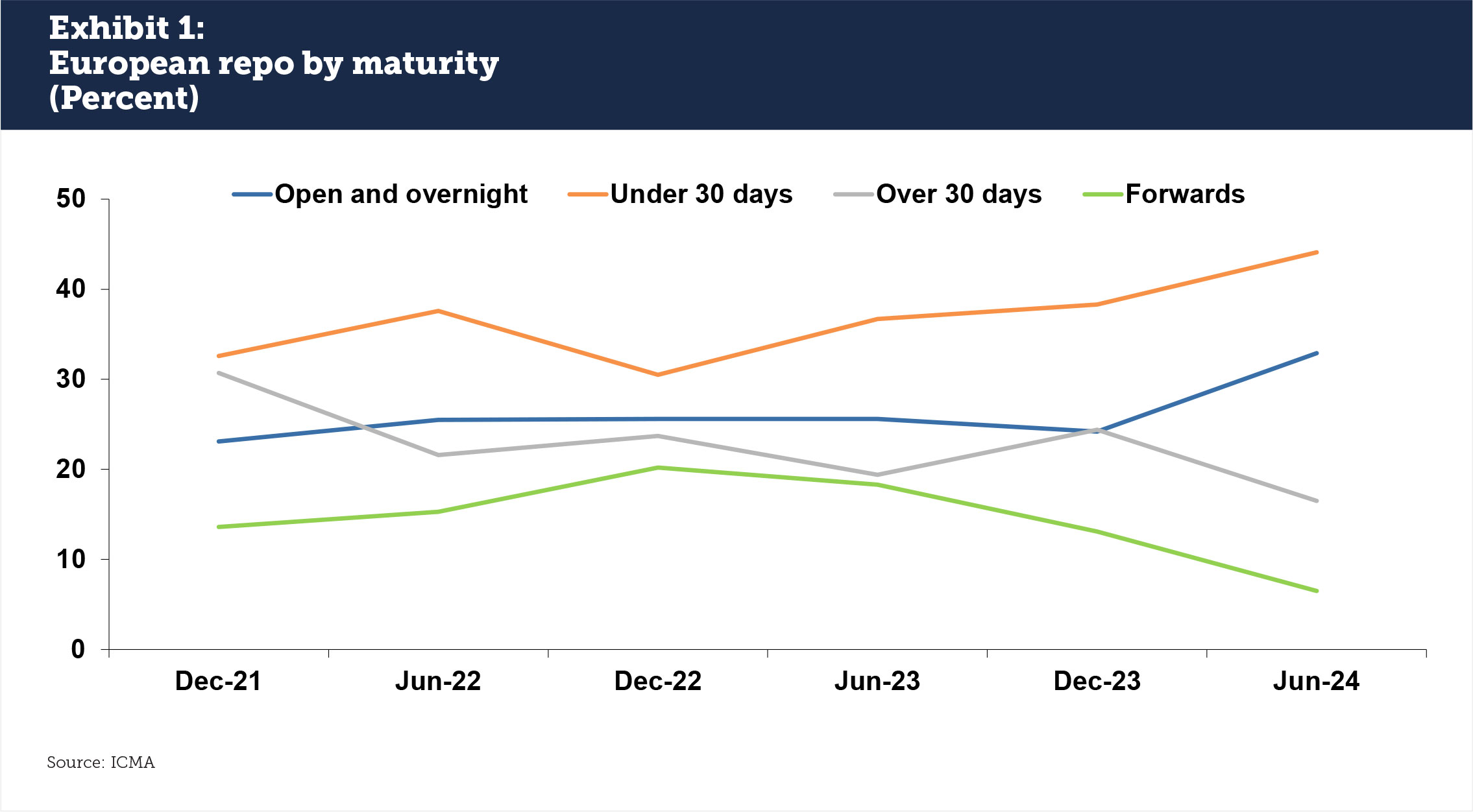

The end of 2024 is breaking from recent historical patterns. According to data from the International Capital Market Association (ICMA), term repo under 30 days has been gaining as a percentage of repo contract maturities. From December 2021, to June 2024, under 30 day contracts have grown from 33% of the market to 44% (see Exhibit 1). The open and overnight segment has also grown from 23% to 33%, with most of the increase happening in 2024 alone. Term repo over 30 days however has shrunk along with forward-dated contracts.

Going into the end of 2024 however, Eurex reports that term activity is highly elevated not just in German government bonds but across all four core European markets (Germany, France, Italy and Spain). Term trading activity started earlier in September 2024 compared to a later start in 2023, and average terms are increasing.

The end of collateral scarcity meets FX volatility

Increasing volumes are a notable impact of Quantitative Tightening in Europe and a return to collateral markets based on private market supply and demand. The ECB is transitioning from a policy of abundant reserves to “ample reserves,” which means a net shrinkage in its balance sheet holdings. In late 2022, central bank assets in the Eurozone stood at €8.7 trillion but has since declined to just over €6.4 trillion in October 2024.

The transmission mechanism of central bank balance sheets to dynamic repo market means that the fewer assets held by central banks, the more assets are held by private market participants that look to invest cash or finance collateral. Eurex repo balances have grown accordingly: GC Pooling balances have nearly tripled from June 2021 through October 2024.

The EUR-USD FX basis presents another opportunity for volatility and a need for some traders to lock in financing rates. Highly volatile USD/EUR exchange rates around and following the US election suggest that nothing is certain: while the euro could strengthen against the dollar through the end of the year, it could also fall just as much. With this much up in the air, locking in financing now is a prudent risk management move.

Compared to prior years, pricing in European government bond repo has right-sized away from the negative rates of the COVID and zero-interest rate periods to an €str+ market. Eurex sees that floating rate repos in German bonds are at €str+9 bps and Italian government bonds are at €str+15 bps. Rates over the turn are even higher, with German bonds at €str+25 bps and Italian government bonds at €str+225 bps. Compared to expectations this time in 2022, when German collateral was trading around €str–1,000 bps implied going over the turn, the change in pricing shows a sharp improvement in private market functioning.

This also means that European dealers for now still have the balance sheet capacity to extend term repo to their clients, albeit at a price. For firms looking to ensure certainty of their funding costs, the ability to lock in term repo is critical. This risk management also leads to a greater ability to engage in trades across the spectrum of asset classes.

Term supply vs. demand in the US

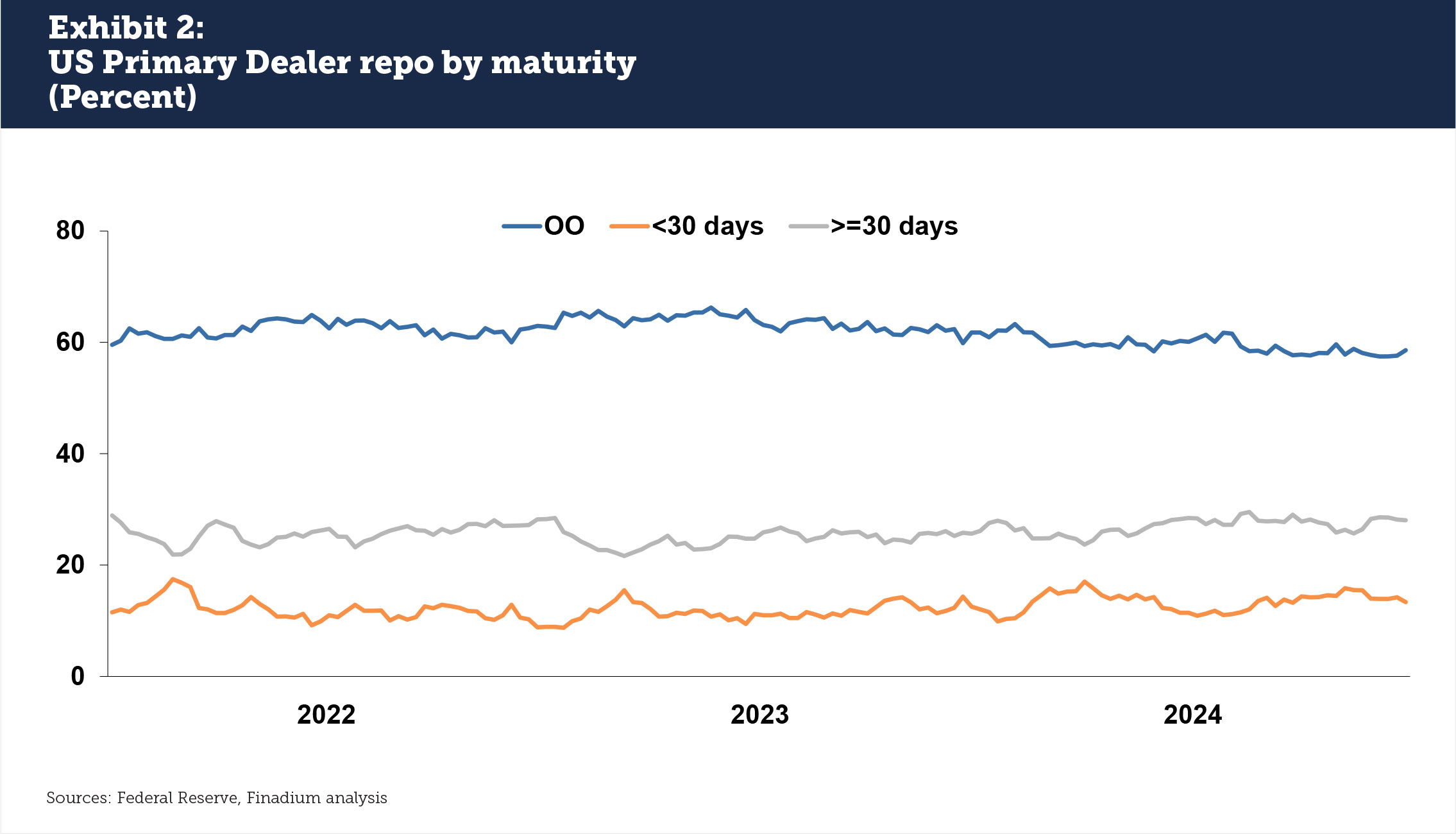

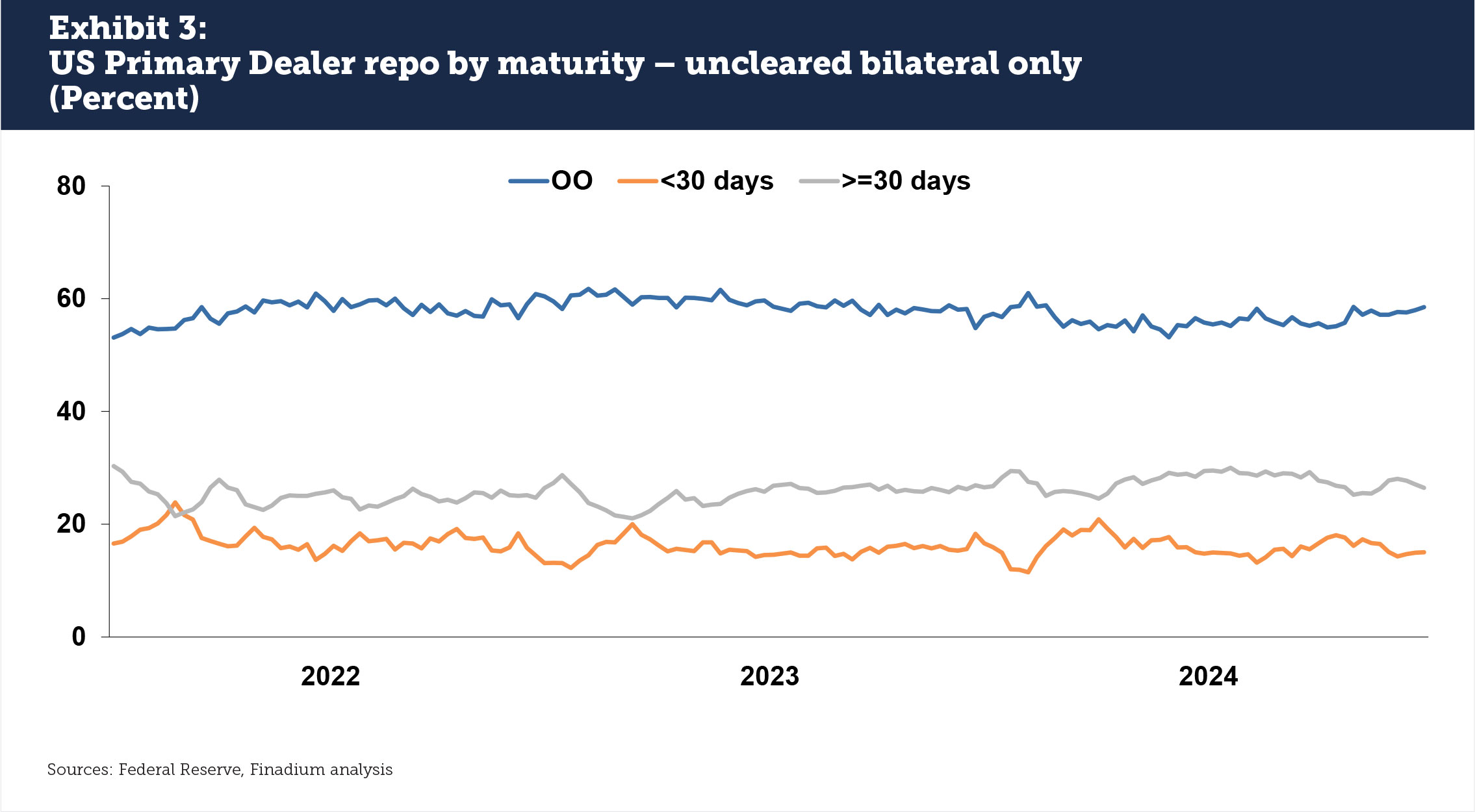

In the US, market participants note a lack of term repo especially in cleared markets. Data from US primary dealer reports to the Federal Reserve show that in total, the amounts of repo between 2-30 days of maturity and over 30 days of maturity have not changed much between 2022 and 2024; any differences are within 2% of their starting points (see Exhibit 2). However, increasing balances on the FICC Sponsored Repo program for overnight repo have left some firms looking for counterparties able to offer bilateral repo to cover the year end, and Federal Reserve data show a percentage decline in uncleared bilateral term repo activity in recent months (see Exhibit 3).

Regardless of the totals, a lack of term repo will always be defined by collateral funder demand. Going into the end of the year, demand seems to be outpacing supply on dealer balance sheets in the US.

The impact of clearing

Eurex is unique in the cleared repo landscape in that there are available contracts for up to three years on the repo market. This contract type is much longer in duration than most dealers look to offer in the bilateral market. Eurex cites netting benefits across market segments as part of why clearing firms are attracted to Eurex term markets.

“We think the availability of term repo in centrally cleared markets significantly increases resilience of European repo markets vs. that of other markets. The increase in activity also shows that private markets function and are able to replace the cheap term funding which had been offered via the ECB´s LTROs”, noted Frank Odendall, Head of Securities Financing Product & Business Development at Eurex.

Eurex now also offers an Evergreen repo contract to help regulated entities mitigate the impact of Basel III’s Net Stable Funding Ratio (NSFR). The NSFR is a measurement of risk exposure up to a year. Eurex’s contracts are offered at 185 or 370 day tenors, allowing firms to recognize long-term funding benefits. The trade tenor remains constant until one counterparty gives notice, at which point it counts down to a final settlement date like any non-term agreement. These types of innovations cannot always be managed bilaterally; having an exchange and clearinghouse in the middle solves a market funding problem.

No similar exchange contracts exist in the US. The FICC states that “The Sponsored DVP Service allows eligible GSD Members to sponsor their clients into GSD membership. Eligible transactions include two-directional (i.e., cash borrowing and cash lending) overnight and term DVP repo in U.S. Treasury and Agency securities and outright purchases and sales of such securities.” However, market reports are that not enough transactional volume occurs in term as to meet the breadth of demand.

This article was commissioned by Eurex.