- Report outlines risks from leverage, liquidity mismatch and interconnectedness

- Non-bank vulnerabilities could amplify cyclical risks to financial stability

The European Systemic Risk Board (ESRB) published the EU Non-bank Financial Intermediation Risk Monitor 2025 (NBFI Monitor) highlighting key cyclical and structural risks.

Leverage, liquidity mismatches and interconnectedness remain key vulnerabilities across the NBFI sector. This year’s report examines the role of captive financial institutions (i.e. subsidiaries of non-financial companies providing financial services exclusively to the parent and its affiliates) in facilitating liquidity and financing within transnational corporations. It explores their interconnectedness with private equity and real estate funds and the systemic risks this could pose. These topics, alongside carry trade activity by global hedge funds and the use of bank lending by real estate investment funds, are covered in five special features. Additionally, the report looks at the growing importance of private finance, with non-bank credit provision increasingly complementing traditional bank funding.

Given ongoing macroeconomic challenges and heightened market volatility, structural vulnerabilities in non-bank financial intermediaries could amplify cyclical risks to the stability of the EU financial system. Persistent geopolitical tensions, tighter financial conditions and subdued growth prospects could exacerbate credit and market risks. This may result in significant losses and strain non-bank financial intermediaries engaged in liquidity transformation, particularly those with concentrated exposures to US technology stocks or commercial real estate, or those reliant on high leverage. Moreover, vulnerabilities linked to liquidity mismatches and interconnectedness within the NBFI sector could magnify the impact of market stress and destabilize the broader financial system.

UCITS’ high leverage

Though typically associated with alternative investment funds, high leverage is also prevalent in certain undertakings for collective investment in transferable securities (UCITS) funds designed for retail investors. These funds pursue hedge fund-like strategies, exposing them to significant market and liquidity risks.

UCITS are subject to stringent constraints for on-balance-sheet leverage, but some funds using the VaR approach have increased synthetic leverage through derivative positions. Regarding financial leverage, all UCITS can borrow up to 10% of their NAV on a temporary basis. All UCITS also face constraints on their global exposures. Under the commitment approach, which is used by most funds, leverage after netting and hedging is limited to 100% of NAV.

However, funds can employ the VaR approach, which imposes indirect limits on their leverage by limiting market risks. Under the relative VaR approach, the one-month VaR of the fund at the 99th confidence level must be equal to or less than 200% of the VaR of a leverage-free benchmark. Under the absolute approach, the VaR is limited to 20% of NAV.

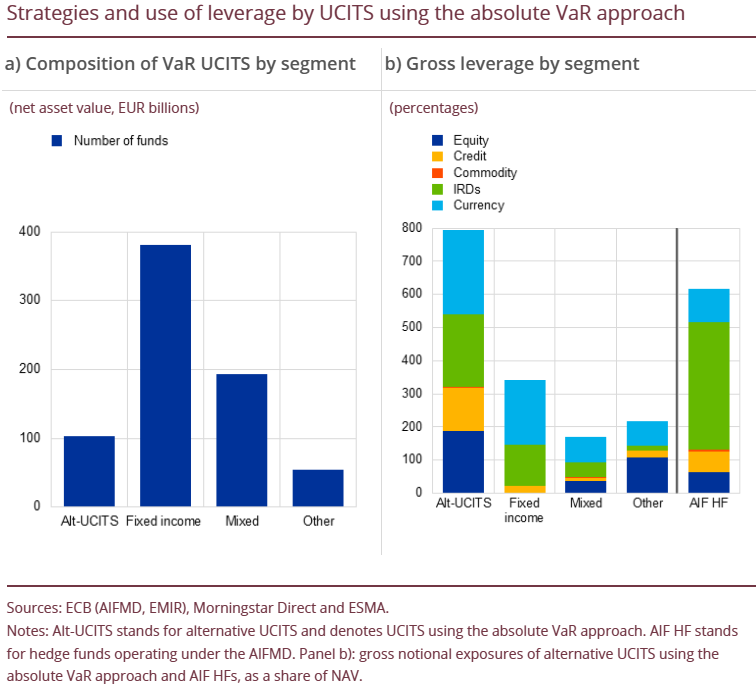

UCITS employing the absolute VaR approach constitute at least 8% of all UCITS funds in terms of net assets and pursue a variety of strategies. Some UCITS using the absolute VaR approach have high levels of gross leverage that exceed those of alternative investment fund (AIF) hedge funds. These funds constitute 2% of all UCITS in terms of net assets.

Some UCITS that employ the absolute VaR approach have leverage levels higher than AIF hedge funds: alternative UCITS had an aggregated leverage of 800% of NAV at the end of 2023, compared with 600% for AIF hedge funds. Focusing on funds with leverage exceeding 400% of NAV, this group comprises many different types of funds. Around 56% of alternative UCITS have a leverage above 400%, while the share is 15% across fixed income, mixed and other funds.