Basis traders, taking advantage of small mispricings between US Treasury (UST) cash and futures, and using repo to finance the trade, have become an increasingly important part of the UST cash buyer’s market. Mandatory clearing of US Treasury repo has the potential to increase their costs, and a reduction in basis trading could exacerbate already strained market conditions if international buyers of US Treasuries decide to go elsewhere at the same time, among other potential events that would hinder liquidity.

The CME/FICC cross-margining arrangement for US Treasuries could provide enough of a new cost structure for basis traders that they stay in the market after June 2027, and that could have far-ranging beneficial impacts. On the other hand, a breakdown in the basis trade could lead UST markets in the other direction and potentially force central bank intervention.

Here’s the thesis for why the CME/FICC cross-margining arrangement would help basis traders and, by extension, liquidity in UST markets:

– The Office of Financial Research has previously reported that at least 70% of uncleared bilateral repo transactions are conducted at 0% margin. A move to mandatory clearing at a higher margin point, hypothesized at 2% for general purposes, would force additional costs into the system and potentially make today’s basis trade’s uneconomical.

– Estimates are that basis traders have US$800 billion to US$1 trillion in UST cash holdings as part of their leveraged strategies. Basis traders have been cited for some years now as an important source of liquidity for UST, especially in a period of growing issuance. At the New York Fed’s 2023 UST conference, speakers noted that basis traders were acting as liquidity providers given a lack of other natural suppliers.

– International buyers hold much more but sales or a lack of further purchases could create volatility, especially at a time of increased issuance. China is the second largest foreign holder of US Treasury government debt after Japan, according to the US Treasury. China’s actual holdings are probably larger however as it’s been said that China is using omnibus accounts at Euroclear and other central securities depositories to hide the true total of its UST assets.

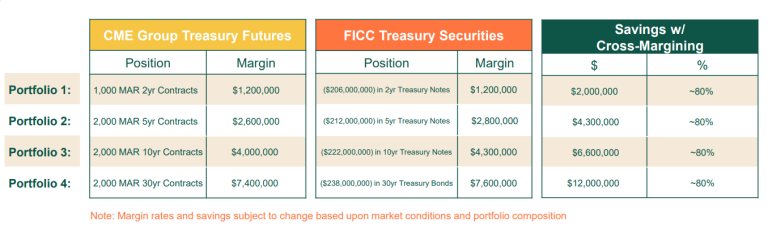

– According to DTCC, the CME/FICC arrangement should save traders 80% a year in margin cost (see chart). If basis traders are at 0% now and on the way to 2% (probably not that high but for illustrative purposes), then this would get their margin to 40 basis point. The program should be launching in Q4 2025 for buy-side clients.

– If the basis point savings from cross-margining is less than what basis traders currently earn then they should stay in the market. There may still be revenue loss as 0% margin is going to beat anything that a CCP will charge, even with cross-margining, but there will be some revenue compared to a negative return at 2% margin.

– Dealers note that the CME cash leg needs to apply to SA-CCR to make cross-margining work. We think it should but there appear to be some outstanding questions. Without SA-CCR, then cross-margining doesn’t work for clients.

It may not be good for market structure, but providing some stability to basis traders right now could be an important hedge against UST market disruption. Not as good as excepting Treasuries from bank Supplementary Leverage Ratios but not bad nonetheless.

Hedge funds in the UST basis trade got particular attention as marginal buyers given market behavior in March 2020. During this well-studied period, hedge funds looked to unwind their basis trades in a hurry due to illiquidity in cash UST markets and to avoid some or further financial losses due to higher futures margin and repo rate volatility. This happened at the same time that COVID-19 made a global impact, with policymakers, regulators and central banks all working to respond as fast as possible to the economic and social upheaval brought on by the pandemic.

Liquidity is at stake in the current market environment: if basis traders find that the cost of cleared repo outweighs the spread they are earning from basis trades, then they will not conduct those trades. This could impact UST liquidity at a critical time if global investor behavior is shifting as well.